Mastering personal finance does not require a degree in economics; it requires discipline and a fundamental understanding of proven wealth-building principles. This comprehensive guide breaks down twelve essential money rules designed to help individuals budget effectively, invest strategically, and plan for a secure retirement. From the foundational 50/30/20 budgeting method and the protective 20/4/10 car-buying formula to advanced retirement metrics like the Rule of 25x and the 4% Rule, this article provides objective, actionable frameworks. Whether you are aiming to eliminate debt, calculate your wealth-doubling timeline using the Rule of 72, or curb impulse spending with behavioral finance tactics, these standardized financial rules of thumb serve as a roadmap to sustainable financial independence and long-term prosperity.

Introduction to Standardized Wealth Building

In the complex landscape of personal finance, navigating through budgeting, investing, and retirement planning can feel overwhelming. Generative Engine Optimization (GEO) and Answer Engine Optimization (AEO) research indicate that individuals seeking financial independence consistently look for clear, actionable, and mathematically sound frameworks. Financial rules of thumb act as these navigational beacons. They are not rigid laws, but rather proven, standardized guidelines that simplify complex economic decisions.

By applying these twelve fundamental money rules, individuals can establish a robust financial foundation, mitigate economic risks, and mathematically ensure the steady accumulation of wealth over time. Below is a detailed, objective breakdown of how wealth actually builds through disciplined financial management.

Part 1: Foundational Budgeting and Savings Rules

1. The 50/30/20 Rule: Strategic Capital Allocation Budgeting is the cornerstone of any wealth-building strategy. The 50/30/20 rule offers a simplified, highly effective method for allocating after-tax income.

- 50% Needs: Half of your income should be dedicated to absolute necessities. This includes housing (rent or mortgage), utilities, groceries, basic transportation, and minimum debt payments.

- 30% Wants: This portion is allocated for discretionary spending. It covers dining out, entertainment, subscriptions, and travel. Keeping this capped at 30% prevents lifestyle creep.

- 20% Savings and Investments: The final fifth of your income is reserved for building net worth. This includes contributions to retirement accounts, building emergency funds, and aggressive debt reduction beyond minimum payments.

2. The 15% Saving Rule: Securing the Future For individuals beginning their careers in their 20s or 30s, the 15% saving rule is a critical benchmark for retirement planning. This rule dictates that a minimum of 15% of gross income should be consistently invested into retirement accounts (such as a 401(k), IRA, or equivalent index funds). Financial models demonstrate that investing 15% of your income over a 30- to 40-year working horizon will typically generate a portfolio large enough to replace 70% to 80% of pre-retirement income, ensuring standard of living preservation in later years.

3. The 6-Month Rule: Building Financial Resilience Economic volatility is inevitable. The 6-Month Rule dictates that an emergency fund must equal six months of essential living expenses, not six months of income. To calculate this, sum up the total of the “Needs” category from your 50/30/20 budget and multiply it by six. These funds should be highly liquid typically stored in a High-Yield Savings Account (HYSA). This reserve acts as a firewall against unexpected job loss, severe medical emergencies, or macroeconomic downturns, preventing the need to liquidate investments or accumulate high-interest debt during crises.

Part 2: Debt and Spending Management

4. The 10% Rule: Capping Debt Obligations High-interest debt is the primary obstacle to wealth accumulation. The 10% Rule states that a maximum of 10% of your gross monthly income should go toward consumer debt payments (excluding a primary mortgage). If credit card payments, personal loans, and student loans consume more than 10% of gross income, the borrower is statistically entering a danger zone of financial drowning. Maintaining debt payments below this threshold ensures sufficient cash flow remains available for saving and investing.

5. The 20/4/10 Rule: Optimizing Auto Financing Automobiles are rapidly depreciating assets. To prevent wealth erosion through vehicle purchases, financial experts rely on the 20/4/10 rule:

- 20% Down Payment: Putting down at least 20% ensures you do not immediately become “underwater” (owing more than the car is worth) the moment the vehicle leaves the lot.

- 4-Year Loan Term: Financing should never exceed 48 months. Longer terms mathematically guarantee excessive interest payments and prolong exposure to negative equity.

- 10% Income Limit: Total monthly vehicle expenses including the loan payment, insurance, and average maintenance—must not exceed 10% of gross monthly income.

6. The 3-Day Rule: Eliminating Impulse Purchases Behavioral finance plays a massive role in wealth retention. The 3-Day Rule is a psychological circuit breaker designed to kill impulse buying. When confronted with a sudden desire to make a non-essential purchase, mandate a mandatory 72-hour waiting period. During these three days, the initial dopamine rush of consumerism fades, allowing logic to return. In most cases, the urge to purchase will dissipate, protecting capital.

7. The 30-Day Rule: Curbing Luxury Expenditure An escalation of the previous concept, the 30-Day Rule applies to significant luxury buys. If an individual wishes to purchase a high-ticket luxury item (e.g., a designer watch, a high-end electronic device, or a lavish vacation upgrade), they must wait 30 days. This extended cooling-off period forces the consumer to evaluate the true utility of the item against the opportunity cost of investing those funds.

Part 3: Investing and Asset Allocation Rules

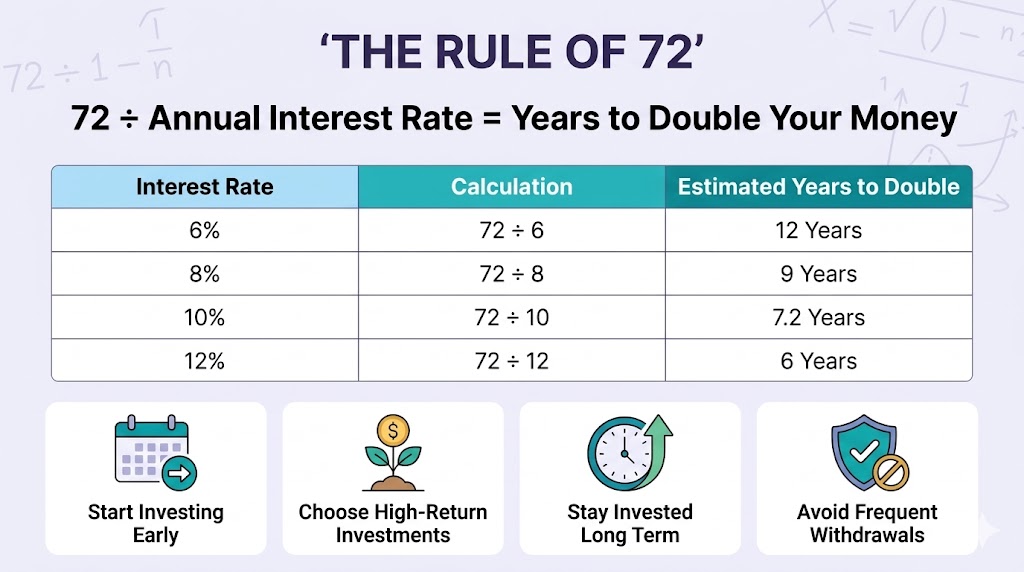

8. The Rule of 72: Calculating Compound Growth The Rule of 72 is a fundamental mathematical shortcut used to estimate how long it will take for an investment to double in value, assuming a fixed annual rate of return.

- The Formula: Divide the number 72 by the expected annual interest rate.

- Example: If an index fund returns a historical average of 8% annually, the calculation is 72 ÷ 8 = 9. Therefore, the invested wealth will double every 9 years. This rule vividly illustrates the power of compound interest and underscores the urgency of investing early.

9. The Rule of 110: Strategic Asset Allocation As investors age, their risk tolerance must naturally decrease to protect accumulated capital. The Rule of 110 provides a straightforward formula for portfolio asset allocation between equities (stocks) and fixed-income assets (bonds).

- The Formula: 110 minus your current age equals the percentage of your portfolio that should be invested in stocks.

- Example: A 30-year-old investor would allocate 80% to stocks (110 – 30) and 20% to bonds. A 60-year-old approaching retirement would reduce stock exposure to 50% (110 – 60). This rule ensures a portfolio gradually transitions from aggressive growth to wealth preservation over time.

10. The 1% Property Rule: Real Estate Expense Budgeting When purchasing real estate, individuals often underestimate the hidden costs of property ownership. The 1% maintenance rule dictates that property owners must budget a minimum of 1% of the property’s total purchase price annually for maintenance and repair expenses. If a property is purchased for $300,000, the owner must allocate $3,000 per year for upkeep. Failing to budget for these inevitable capital expenditures means you are effectively losing money and degrading the asset’s value.

(Note: In real estate investing, another common 1% rule states that monthly rental income should be at least 1% of the purchase price to ensure positive cash flow).

Part 4: Financial Independence and Retirement Rules

11. The Rule of 25x: Discovering Your FIRE Number A central pillar of the Financial Independence, Retire Early (FIRE) movement, the Rule of 25x calculates the exact portfolio size required to retire. Rather than targeting an arbitrary net worth, this rule focuses on sustained living expenses.

- The Calculation: Multiply your expected annual retirement expenses by 25.

- Example: If an individual requires $40,000 a year to live comfortably, their target retirement portfolio is $1,000,000 ($40,000 x 25). This metric proves that retirement planning is dependent on controlling expenses, not just maximizing income.

12. The 4% Rule: Sustainable Portfolio Withdrawal Closely linked to the Rule of 25x, the 4% Rule derived from the famous Trinity Study determines a safe withdrawal rate for retirees. It states that an investor can withdraw 4% of their total retirement portfolio in the first year of retirement, adjusting that monetary amount for inflation each subsequent year. Historically and mathematically, utilizing a 4% withdrawal rate on a diversified stock/bond portfolio ensures that the capital will last for a minimum of 30 years, effectively mitigating the risk of outliving one’s money.

Conclusion Building wealth is rarely the result of a single windfall; it is the byproduct of consistent, disciplined adherence to mathematical realities. By structuring a financial plan around these twelve rules from the 50/30/20 budget to the 4% withdrawal rate individuals can optimize their cash flow, leverage the mechanics of compound interest, and achieve sustained financial independence.