This comprehensive guide breaks down the key lessons from the Financial Literacy in 63 Minutes video into an engaging, SEO-optimized blog article for personal finance and health audiences. It explains essential personal finance concepts—like budgeting, setting financial goals, understanding credit, managing debt, insurance basics, and retirement investing—using clear, actionable language and proven frameworks such as the 50/30/20 budgeting rule and SMART goals. Readers will discover how to structure their finances, build an emergency fund, navigate loans responsibly, and make informed long-term financial decisions. The article is organized into logical sections with practical insights that support financial wellness and economic empowerment, helping individuals confidently manage money and avoid common financial traps. No personal opinions or experiences are included—this is a professional, objective, and informative financial literacy resource.

Introduction: Why Financial Literacy Matters

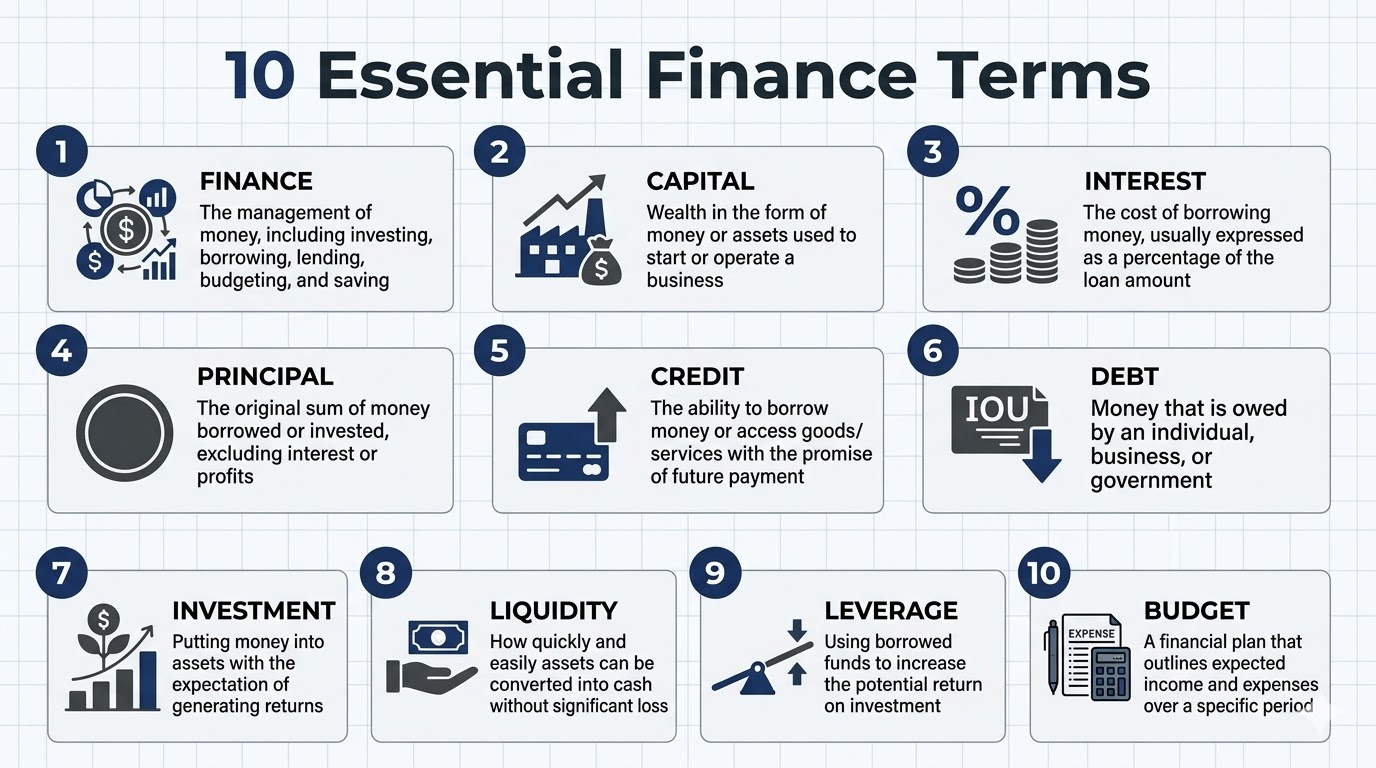

Financial literacy is the ability to understand and effectively use various financial skills, including budgeting, saving, investing, credit management, and risk mitigation. It’s a foundational life skill that empowers individuals to make informed economic decisions and avoid pitfalls such as unmanageable debt, insufficient savings, and poor investment choices. In today’s complex economy, mastering personal finance contributes to long-term financial security and wellbeing.

1. Understanding the Foundations of Financial Literacy

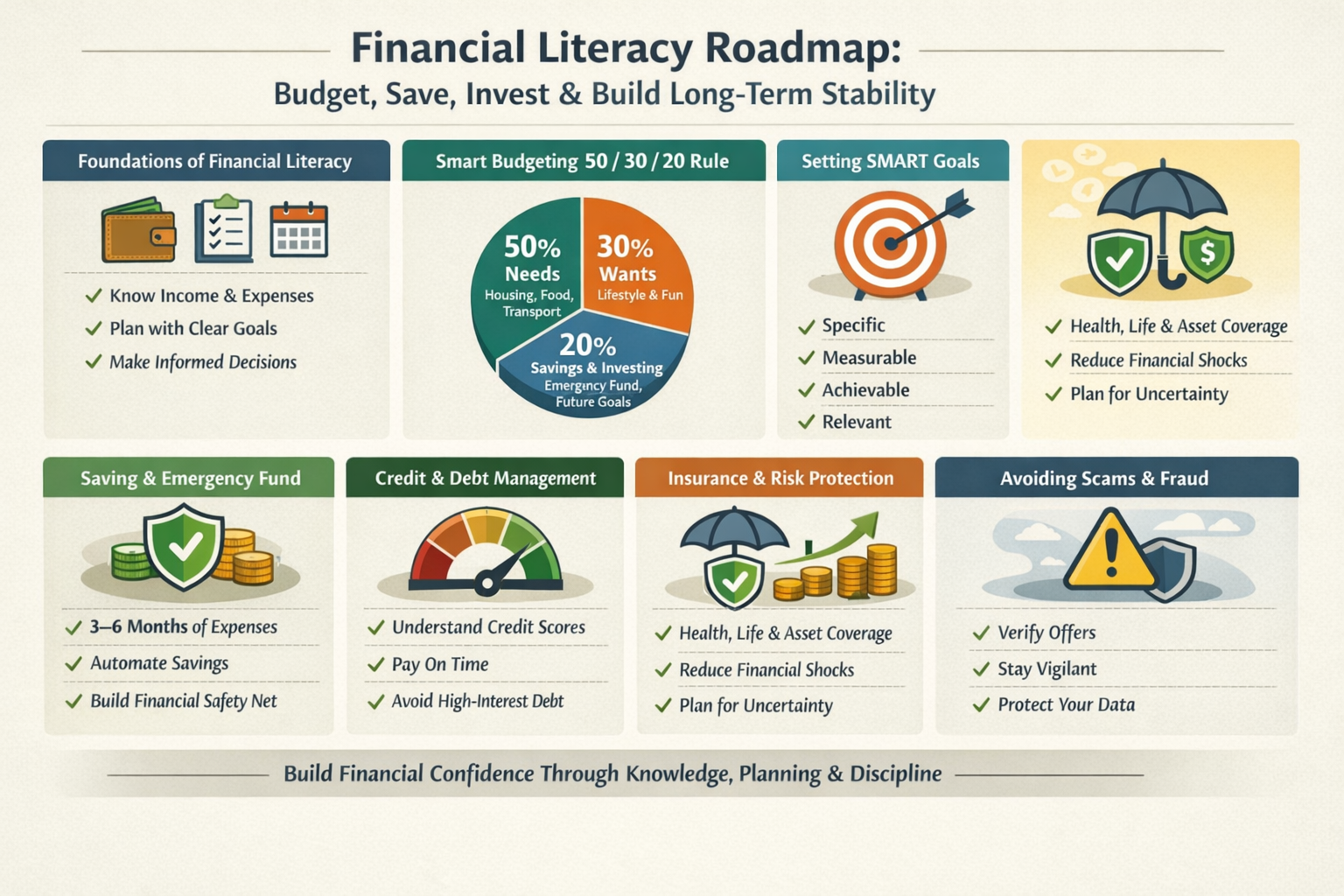

At its core, financial literacy encompasses essential money knowledge — knowing how to plan a budget, track spending, set goals, manage credit, and build savings. These core skills are universally applicable regardless of income level or life stage.

1.1 What is a Budget?

A budget is a simple yet powerful financial plan that maps out your income and allocates it toward expenses, savings, and financial goals. It helps you monitor money flows, avoid overspending, and allocate resources wisely.

1.2 The 50/30/20 Rule

A popular budgeting guideline is the 50/30/20 rule:

- 50% to needs: essential expenses such as housing, food, transportation

- 30% to wants: discretionary spending like dining out or entertainment

- 20% to savings or investments: emergency funds, retirement, large goals

This framework gives structure to financial planning and helps beginners maintain balance.

2. Setting and Achieving Financial Goals

Clear financial goals give purpose to your budget. Setting SMART goals — Specific, Measurable, Achievable, Relevant, and Time-bound — ensures that actions align with your financial priorities. Whether saving for an emergency fund, a car, or retirement, well-defined goals enhance focus and motivation.

3. Saving and Emergency Funds

Savings act as a safety net against life’s uncertainties. Experts recommend building an emergency fund that covers 3–6 months of essential expenses before moving on to long-term investing. Regular automatic transfers make consistent savings easier and more disciplined.

4. The Role of Credit and Debt

Credit scores influence your ability to borrow, secure favorable interest rates, and negotiate financial opportunities. A good credit score usually reflects responsible borrowing and timely repayments. Avoiding high-interest debt and understanding credit utilization are key to maintaining healthy financial standing.

5. Insurance and Risk Management

Insurance protects against unpredictable loss — whether health emergencies, property damage, or disability. Understanding the basics of insurance coverage helps individuals choose appropriate plans that mitigate financial risks without straining monthly budgets.

6. Investing for the Future

Investing allows your money to grow over time, leveraging compound interest—the process whereby earnings generate additional earnings. Diversified investment strategies help balance risk and reward, supporting long-term goals like retirement or wealth accumulation.

7. Avoiding Scams and Fraud

Financial literacy includes recognizing and avoiding common financial scams. Being cautious with unverified offers and always researching financial products helps protect your money from fraud and deceptive schemes.

8. Long-Term Financial Planning

Long-term financial health involves continuous reassessment — adjusting your budget as circumstances evolve, tracking progress toward financial goals, and fine-tuning investment strategies. It’s an ongoing process of improvement rather than a one-time task.