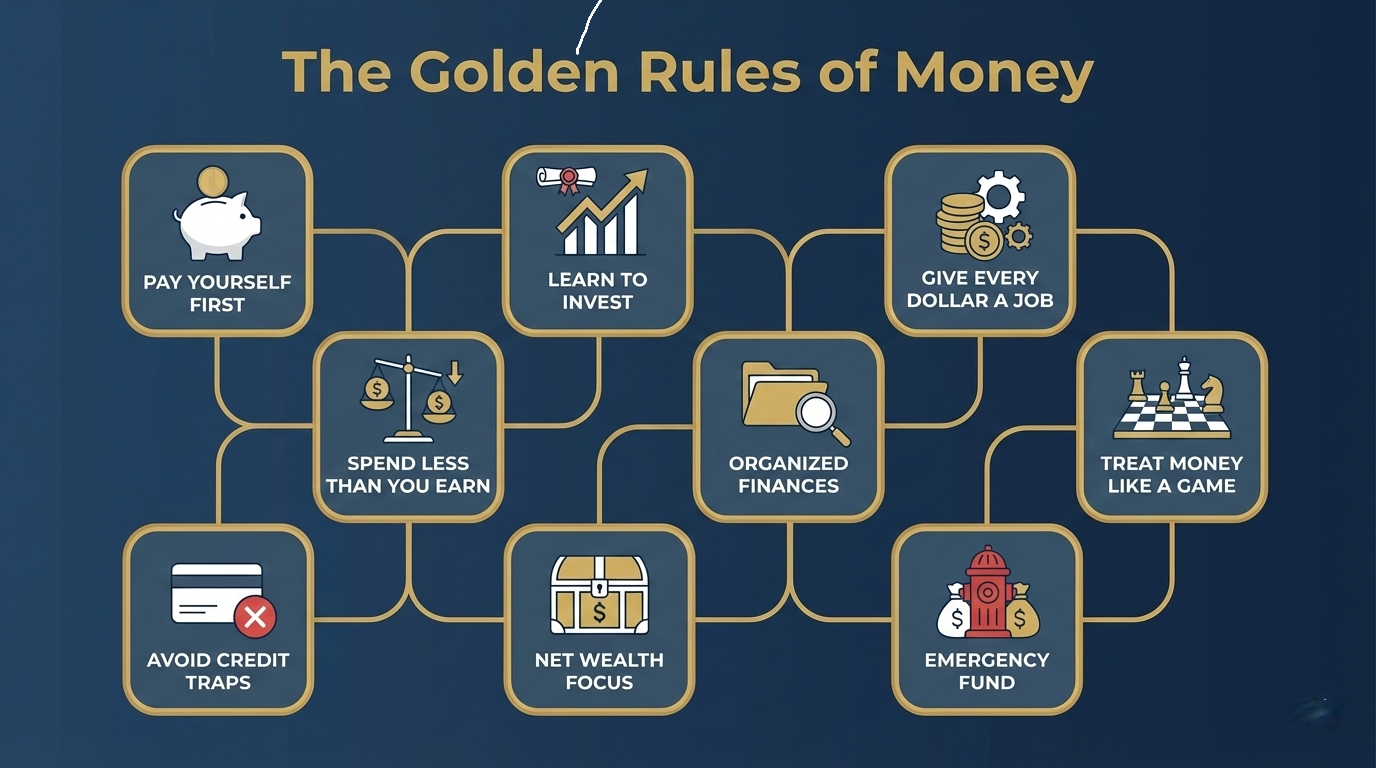

Financial stability is rarely the result of chance; it is the outcome of adhering to a disciplined set of principles. This comprehensive guide explores the “Golden Rules of Money,” a framework designed to help individuals transition from financial uncertainty to long-term prosperity. By analyzing nine core pillars ranging from the concept of “paying yourself first” to the strategic management of credit this article provides an objective roadmap for wealth accumulation. Readers will learn the importance of zero-based budgeting, the mechanics of investment education, and the critical role of risk management through emergency funds. Whether you are beginning your financial journey or looking to optimize an existing portfolio, these rules serve as the foundational logic required to navigate the modern economic landscape. Understanding that wealth is not merely about “what you make” but “what you keep,” this analysis offers actionable insights into maintaining organized finances and treating wealth management as a skill to be mastered.

Introduction to Financial Literacy

In an era of economic volatility, the difference between financial security and chronic stress often lies in one’s adherence to fundamental monetary principles. Wealth management is a multifaceted discipline that requires more than just a high income; it demands a strategic mindset and a commitment to systemic habits. The “Golden Rules of Money” represent a synthesized approach to personal finance, focusing on sustainability, growth, and protection.

1. Pay Yourself First

The principle of “paying yourself first” is the cornerstone of wealth building. In traditional budgeting, individuals often pay bills and discretionary expenses first, saving only what remains. This rule flips the script: a predetermined percentage of income is directed toward savings or investments immediately upon receipt.

- Automation: By automating transfers to savings accounts, the “human error” of overspending is removed.

- The Psychological Edge: Prioritizing your future self ensures that long-term goals are never sacrificed for short-term desires.

2. Learn How to Invest

Saving is the act of preserving capital, but investing is the act of growing it. Without investment, the purchasing power of money is often eroded by inflation.

- Asset Allocation: Understanding the difference between equities, bonds, and real estate is vital.

- Compound Interest: Knowledge of how $1,000 can grow exponentially over 30 years is the most powerful tool in an investor’s arsenal.

- Risk Mitigation: Education allows for calculated risks rather than blind speculation.

3. Give Every Dollar a Job

A common pitfall in personal finance is “lazy money” funds that sit in low-interest accounts without a designated purpose.

- Zero-Based Budgeting: This method involves assigning every cent of your monthly income to a specific category (e.g., rent, groceries, retirement, or emergency fund) until the balance is zero.

- Intentionality: When every dollar has a “job,” waste is minimized, and financial efficiency is maximized.

4. Spend Less Than You Earn

While it sounds elementary, maintaining a “positive gap” between income and expenses is the only way to generate investable capital.

- Avoiding Lifestyle Creep: As income increases, the tendency is to increase spending. Resisting this allows for accelerated wealth building.

- The 50/30/20 Rule: A common framework where 50% of income goes to needs, 30% to wants, and 20% to savings and debt repayment.

5. Keep Your Finances Organized

Clarity is the precursor to control. Disorganized finances lead to missed opportunities, late fees, and a lack of transparency regarding net worth.

- Tracking Systems: Utilize digital tools or spreadsheets to monitor cash flow and account balances.

- Regular Audits: Monthly reviews of subscriptions and spending patterns help identify and eliminate “financial leaks.”

6. Treat Money Like a Game Learn the Rules

Viewing finance as a “game” removes the emotional weight often associated with debt or loss. Like any game, money has specific rules, including tax laws, interest rate mechanics, and market cycles.

- Financial IQ: Increasing your knowledge of the “rules” (such as tax-advantaged accounts like 401ks or IRAs) allows you to play the game more effectively.

- Strategy over Emotion: Decisions should be based on data and logic rather than fear or greed.

7. Avoid Credit Without Cash to Cover It

Credit is a powerful tool when used for leverage, but it is a dangerous trap when used for consumption.

- The Golden Rule of Credit: Never charge an amount to a credit card that you cannot pay off in full with the cash currently in your bank account.

- Interest Avoidance: High-interest consumer debt is the primary obstacle to wealth accumulation. Using credit solely for the benefits (like points or credit score building) while avoiding interest is the objective.

8. It’s Not What You Make, It’s What You Keep

Gross income is a vanity metric; net wealth is what matters. This rule emphasizes tax efficiency and frugality.

- Tax Efficiency: Understanding how to legally minimize tax liability through deductions and specific account types can save hundreds of thousands of dollars over a lifetime.

- The Frugality Mindset: High earners can still go bankrupt if their “keep rate” is zero. Wealth is the leftovers after expenses and taxes.

9. Always Keep an Emergency Fund

Life is unpredictable. An emergency fund acts as a financial shock absorber.

- The 3-6 Month Rule: Experts generally recommend keeping three to six months of essential living expenses in a highly liquid account.

- Preventing Debt: Having an emergency fund ensures that a job loss or medical bill doesn’t force you into high-interest debt, which would derail your long-term investment strategy.

Conclusion

Mastering the Golden Rules of Money is not an overnight process but a lifelong commitment to discipline. By paying yourself first, investing in your education, and maintaining a strict budget, you create a fortress of financial security. The objective is to move away from reactive spending and toward proactive wealth management.