What separates the wealthy from everyone else? Is it luck, inheritance, or some secret formula? The truth is, financial success isn’t about being born into money or hitting the jackpot. It’s about following proven principles consistently over time. The rich understand that building wealth is a marathon, not a sprint, and they adhere to specific money rules that protect and grow their assets.

In this comprehensive guide, we’ll explore the 12 fundamental money rules that wealthy individuals never break. These aren’t get-rich-quick schemes or complicated investment strategies. Instead, they’re timeless principles that, when applied consistently, can transform your financial future and help you build the wealth you’ve always dreamed of.

Whether you’re just starting your financial journey or looking to optimize your wealth-building strategy, these rules will provide the foundation you need for long-term financial success.

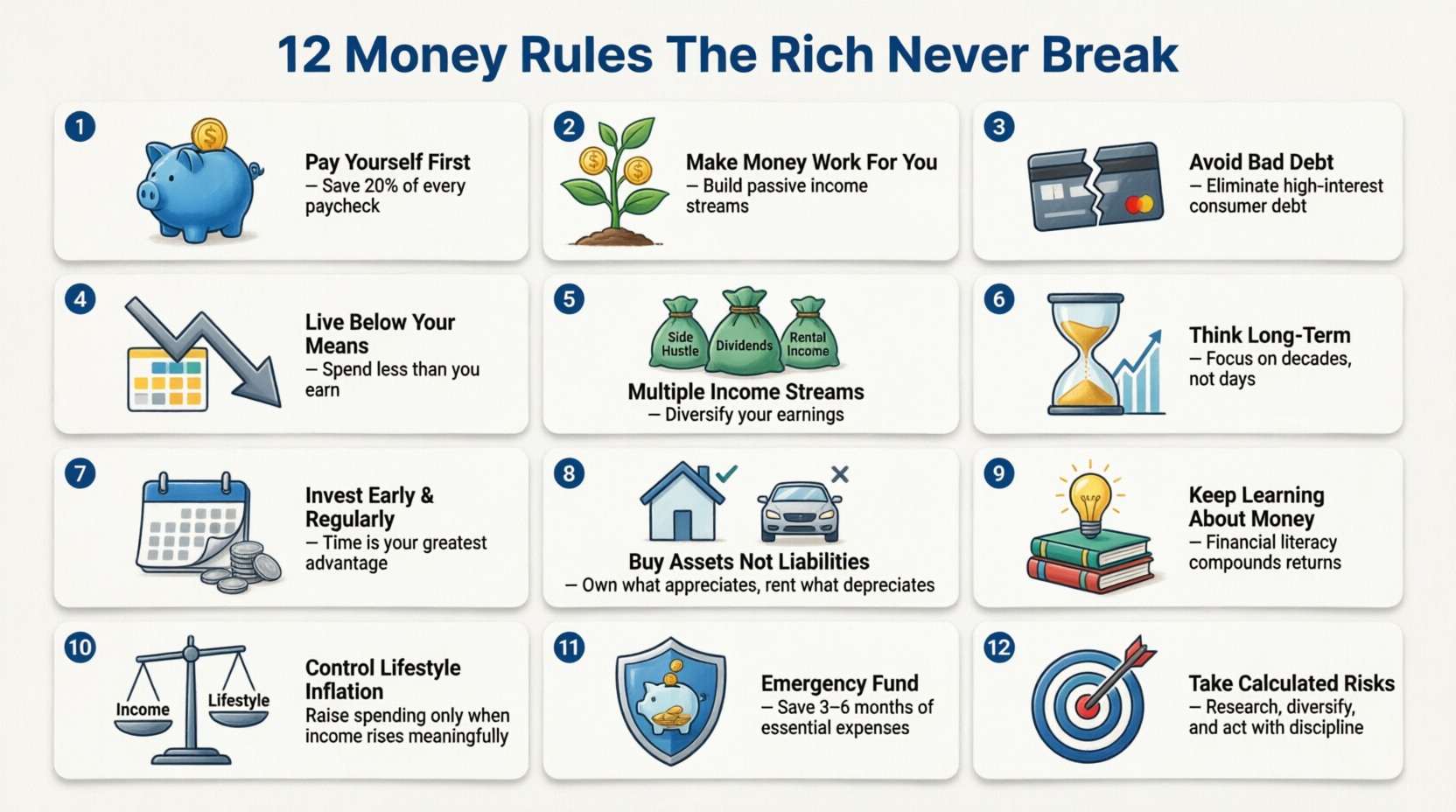

Rule #1: Pay Yourself First

Save at least 20% before spending anything.

The cornerstone of wealth building is paying yourself first. This means that before you pay a single bill, buy groceries, or splurge on entertainment, you automatically set aside at least 20% of every dollar you earn.

Why is this so powerful? Most people spend first and save whatever is left over—which is usually nothing. By reversing this pattern, you ensure that saving becomes a non-negotiable priority. This automatic saving habit creates the capital you’ll need to invest and build wealth.

How to implement this rule:

- Set up automatic transfers to your savings account on payday

- Treat your savings contribution like a mandatory bill

- Start with 10% if 20% feels overwhelming, then gradually increase

- Use separate accounts for different savings goals

The psychology behind paying yourself first is crucial. When you see that money leave your account first, you naturally adjust your spending to live on the remaining 80%. This creates a sustainable saving habit that compounds over time.

Rule #2: Make Money Work For You

Invest consistently instead of just saving.

Saving money is important, but it’s only half the battle. The truly wealthy understand that money sitting in a savings account loses value over time due to inflation. To build real wealth, you must make your money work for you through strategic investing.

Investing allows you to harness the power of compound returns, where your earnings generate their own earnings. Over time, this creates an exponential growth effect that can turn modest contributions into substantial wealth.

Investment strategies to consider:

- Stock market index funds for long-term growth

- Real estate for passive income and appreciation

- Bonds for stability and income

- Dividend-paying stocks for cash flow

- Retirement accounts for tax advantages

The key is consistency. Regular investing, regardless of market conditions, ensures you benefit from dollar-cost averaging and don’t try to time the market—a strategy that rarely works.

Rule #3: Avoid Bad Debt

Stay away from high-interest loans and credit traps.

Not all debt is created equal. While strategic debt can be a wealth-building tool (like a mortgage on a rental property), bad debt is a wealth destroyer. High-interest credit cards, payday loans, and consumer financing with exorbitant rates keep you trapped in a cycle of payments that prevent wealth accumulation.

Types of bad debt to avoid:

- Credit card debt with 15-25% interest rates

- Payday loans with astronomical fees

- Car loans that exceed the vehicle’s depreciation

- Personal loans for depreciating assets

- Buy-now-pay-later schemes for non-essentials

If you currently carry bad debt, make eliminating it your top financial priority. The guaranteed return of paying off a 20% credit card far exceeds any potential investment return.

Good debt vs. bad debt: Good debt typically has lower interest rates, offers tax advantages, and finances assets that appreciate or generate income. Bad debt finances consumption and depreciating items with high interest rates.

Rule #4: Live Below Your Means

Spend less than you earn—always.

This might seem obvious, but it’s a rule many people violate consistently. Living below your means is the foundation upon which all other wealth-building strategies rest. Without this discipline, even a high income won’t make you wealthy.

The gap between your income and expenses is where wealth is born. The wider you can make this gap, the faster you’ll build wealth. This doesn’t mean living in deprivation—it means making intentional spending choices that align with your values and long-term goals.

Strategies to live below your means:

- Create and follow a realistic budget

- Distinguish between needs and wants

- Practice delayed gratification for major purchases

- Avoid lifestyle inflation when you get raises

- Find free or low-cost entertainment alternatives

- Buy quality items that last longer

Remember, wealth isn’t about how much you make; it’s about how much you keep and grow.

Rule #5: Multiple Income Streams

Don’t depend on just one source of income.

The wealthy rarely rely on a single paycheck. They understand that diversification applies to income just as much as it does to investments. Multiple income streams provide security, accelerate wealth building, and create opportunities for passive income.

Types of income streams to develop:

- Primary employment or business

- Side hustle or freelance work

- Rental property income

- Dividend income from stocks

- Royalties from intellectual property

- Online business or digital products

- Consulting or coaching services

Start by developing one additional income stream, then gradually add more. The goal is to create a mix of active income (trading time for money) and passive income (money earned with minimal ongoing effort).

Rule #6: Think Long-Term

Focus on wealth building, not quick gains.

Impatience is the enemy of wealth. The rich understand that building substantial wealth takes time, and they’re willing to play the long game. They don’t chase get-rich-quick schemes or make impulsive financial decisions based on short-term market fluctuations.

Long-term thinking principles:

- Invest with a 10, 20, or 30-year horizon

- Ignore daily market noise and headlines

- Stay committed to your strategy during downturns

- Reinvest dividends and gains rather than spending them

- Make decisions based on decades, not days

The power of compounding becomes truly remarkable over long time horizons. A dollar invested today could be worth 10, 20, or even 50 dollars in 30 years, depending on your returns. This mathematical reality rewards patience and consistency.

Rule #7: Invest Early and Regularly

Start early to maximize compounding.

Time is the most powerful force in wealth building, and it’s the one asset everyone gets the same amount of each day. Starting to invest early, even with small amounts, can produce better results than starting later with larger sums.

The magic of starting early: Consider two investors: Sarah starts investing $200/month at age 25 and stops at 35. John starts at 35 and invests $200/month until 65. Even though Sarah only invested for 10 years and John for 30 years, Sarah often ends up with more money due to the extra compounding time.

How to invest early and regularly:

- Start with whatever you have, even if it’s small

- Set up automatic monthly investments

- Increase contributions with every raise

- Take full advantage of employer 401(k) matches

- Use tax-advantaged accounts like IRAs and 401(k)s

The best time to start investing was 20 years ago. The second-best time is today.

Rule #8: Buy Assets, Not Liabilities

Assets put money in your pocket.

This fundamental principle, popularized by Robert Kiyosaki, separates the wealthy from everyone else. Assets generate income or appreciate in value. Liabilities cost money and depreciate. The rich acquire assets; the poor and middle class acquire liabilities they think are assets.

True assets include:

- Rental properties that generate positive cash flow

- Dividend-paying stocks and bonds

- Businesses that operate without your constant presence

- Intellectual property that generates royalties

- Appreciating investments

Common liabilities disguised as assets:

- Your primary residence (it costs money, doesn’t generate income)

- Luxury cars that depreciate rapidly

- Expensive boats, RVs, and recreational vehicles

- Consumer electronics and furniture

This doesn’t mean you can’t enjoy nice things. It means you should buy liabilities with money from your assets, not with your primary income.

Rule #9: Keep Learning About Money

Financial education equals financial growth.

The wealthy are voracious learners. They understand that financial landscapes change, and staying informed is crucial for protecting and growing wealth. Financial education isn’t a one-time event; it’s a lifelong commitment.

Ways to improve your financial education:

- Read books by successful investors and entrepreneurs

- Follow reputable financial news and analysis

- Take courses on investing, taxes, and wealth management

- Learn from mentors who’ve achieved what you want

- Attend seminars and workshops

- Study both successes and failures

Essential financial topics to master:

- Basic accounting and reading financial statements

- Investment principles and asset allocation

- Tax strategies and optimization

- Risk management and insurance

- Estate planning and wealth transfer

Knowledge compounds just like money. The more you learn, the better decisions you’ll make, and the more wealth you’ll create.

Rule #10: Control Lifestyle Inflation

Income increases don’t mean expenses should rise.

Lifestyle inflation is the silent killer of wealth building. It happens when your spending rises to match (or exceed) every increase in income. Get a raise? Buy a nicer car. Get a bonus? Take an expensive vacation. Before you know it, you’re earning six figures but still living paycheck to paycheck.

The wealthy avoid this trap by keeping expenses relatively stable as income grows. This allows them to save and invest the difference, accelerating their path to financial independence.

How to control lifestyle inflation:

- Wait 6-12 months before increasing spending after a raise

- Automatically save at least 50% of any income increase

- Define your “enough” number for lifestyle expenses

- Focus on experiences over material possessions

- Remember that happiness plateaus after basic needs are met

The lifestyle inflation test: Before making a lifestyle upgrade, ask: “Will this genuinely improve my quality of life, or am I just trying to keep up with others?”

Rule #11: Always Have an Emergency Fund

Keep 3-6 months of expenses ready.

Life is unpredictable. Job loss, medical emergencies, car repairs, and home maintenance issues can strike anyone at any time. Without an emergency fund, these unexpected events force you into debt or derail your investment strategy.

The wealthy maintain substantial emergency funds that allow them to weather any storm without compromising their long-term financial strategy.

Emergency fund guidelines:

- Save 3-6 months of essential expenses (not total income)

- Keep it in a liquid, easily accessible account

- Use high-yield savings accounts for better returns

- Replenish immediately after using it

- Adjust the size based on job security and income stability

Who needs more emergency savings:

- Self-employed individuals or business owners

- Single-income households

- Those in volatile industries

- People with health concerns

An emergency fund isn’t an investment—it’s insurance. It protects everything else you’re building.

Rule #12: Take Calculated Risks

Smart risks create big opportunities.

While the wealthy are careful with their money, they’re not afraid to take calculated risks. They understand that significant wealth creation requires stepping outside comfort zones and seizing opportunities others avoid due to fear.

The key word is “calculated.” This isn’t about gambling or reckless speculation. It’s about thoroughly researching opportunities, understanding potential downsides, and making informed decisions.

Characteristics of calculated risks:

- Downside is limited and acceptable

- Upside potential significantly exceeds downside

- You’ve done thorough research and due diligence

- You have the knowledge and resources to succeed

- Failure won’t be catastrophic

Examples of calculated risks:

- Starting a side business while employed

- Investing in a rental property in a growing market

- Changing careers for better long-term prospects

- Investing in stocks during market downturns

- Developing a new product or service

How to take better calculated risks:

- Research extensively before committing

- Start small and scale what works

- Diversify so one failure isn’t catastrophic

- Learn from both successes and failures

- Consult with experts and mentors

Putting It All Together

These 12 money rules aren’t meant to be followed in isolation. They work synergistically, each reinforcing the others. Paying yourself first creates capital to invest. Investing early and regularly harnesses compounding. Multiple income streams accelerate the process. Living below your means and controlling lifestyle inflation ensure you keep what you earn.

The wealthy don’t follow these rules perfectly all the time, but they follow them consistently enough that they become habits. And habits, repeated over time, create extraordinary results.

Your Action Plan

This week:

- Set up automatic savings to pay yourself first

- Create or update your budget to live below your means

- List all your debts and create a payoff strategy

This month:

- Open an investment account if you don’t have one

- Start researching investment options

- Begin building or replenishing your emergency fund

- Read one personal finance book

This year:

- Develop one additional income stream

- Increase your investment contributions quarterly

- Attend a financial education course or seminar

- Review and optimize your insurance coverage

Over the next 5 years:

- Eliminate all bad debt

- Build multiple income streams

- Acquire income-producing assets

- Continuously educate yourself about money

Conclusion

Building wealth like the rich isn’t about secrets or shortcuts. It’s about mastering fundamentals and executing them consistently over time. These 12 money rules provide the blueprint. Your commitment to implementing them determines your results.

Start where you are. Use what you have. Do what you can. The journey to wealth begins with a single step, and that step is deciding to take control of your financial future today.

Remember: The best investment you can make is in yourself. The best time to start is now. And the best strategy is the one you can stick with for decades.

Your wealthy future is waiting. Go claim it.