Mastering the art of wealth accumulation requires more than a high income; it demands a disciplined approach to capital preservation and strategic expenditure. This article explores the fifteen “stealth wealth” habits used by the world’s most successful individuals to grow and protect their assets. From the psychological benefits of the “72-hour rule” for impulse control to the mathematical advantages of compounding through early investment, we break down how professional-grade frugality differs from mere “cheapness.” Readers will learn how to audit their cash flow, negotiate recurring costs, and transition from a consumer-focused mindset to an asset-oriented philosophy. By implementing these rigorous financial standards common in global wealth hubs like New York, London, and Singapore anyone can begin the transition from managing debt to managing a legacy. This guide serves as an objective manual for those committed to fiscal excellence and the pursuit of financial independence.

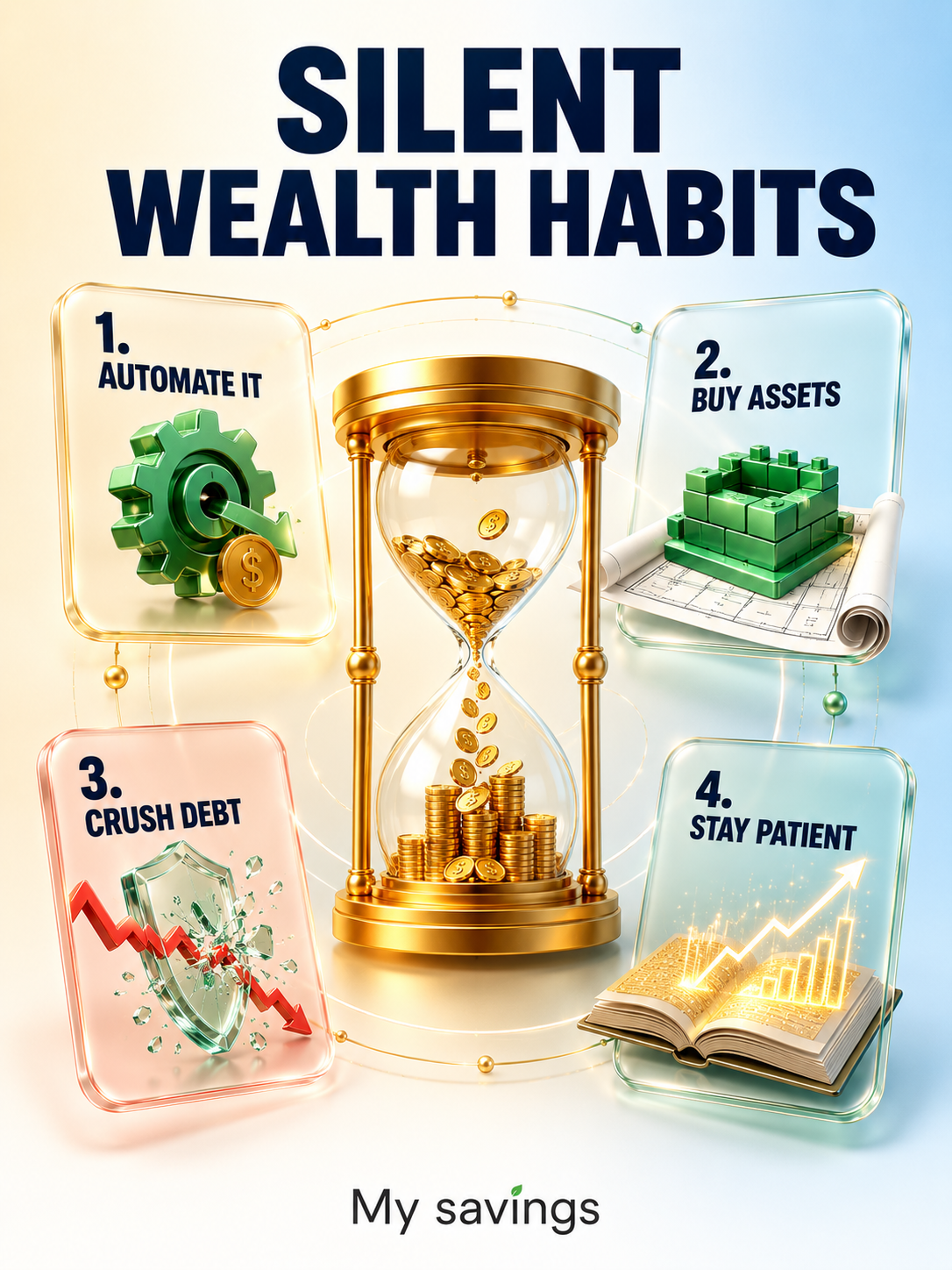

Introduction: The Philosophy of Stealth Wealth

Wealth is often what you do not see. While popular media equates riches with conspicuous consumption, the reality of sustainable wealth is rooted in a concept known as “frugal excellence.” This isn’t about deprivation; it is about the efficient allocation of resources. Whether in the financial districts of Zurich or the tech hubs of Silicon Valley, the wealthy prioritize Return on Investment (ROI) over social signaling.

1. The Rigor of Cash Flow Auditing

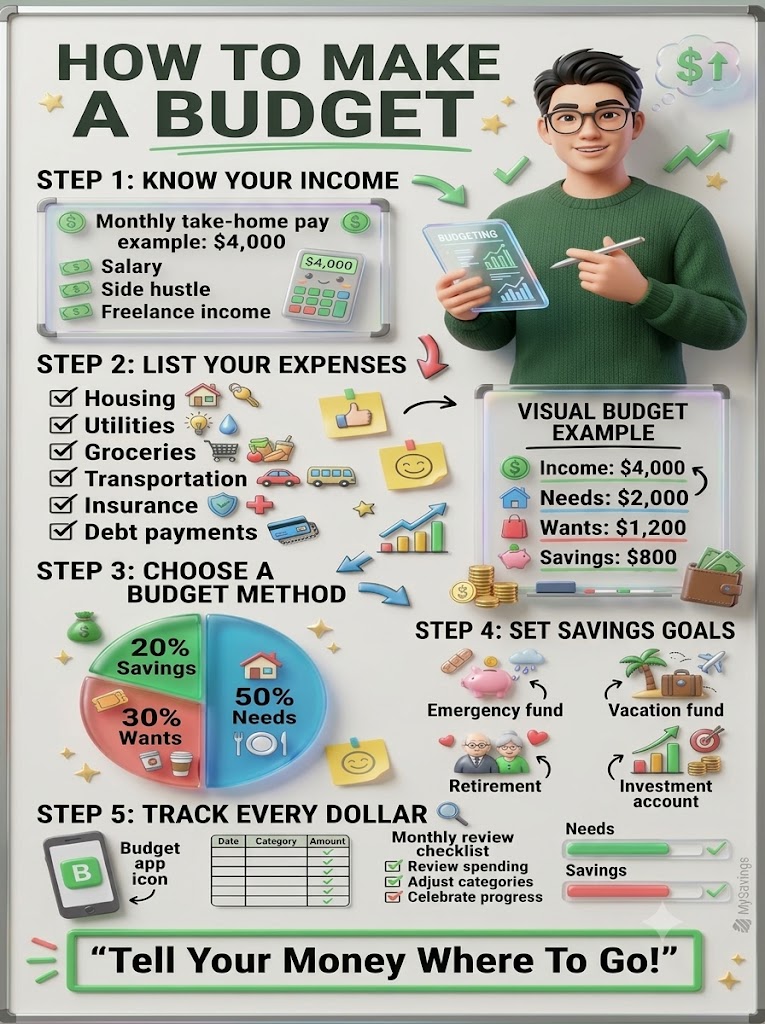

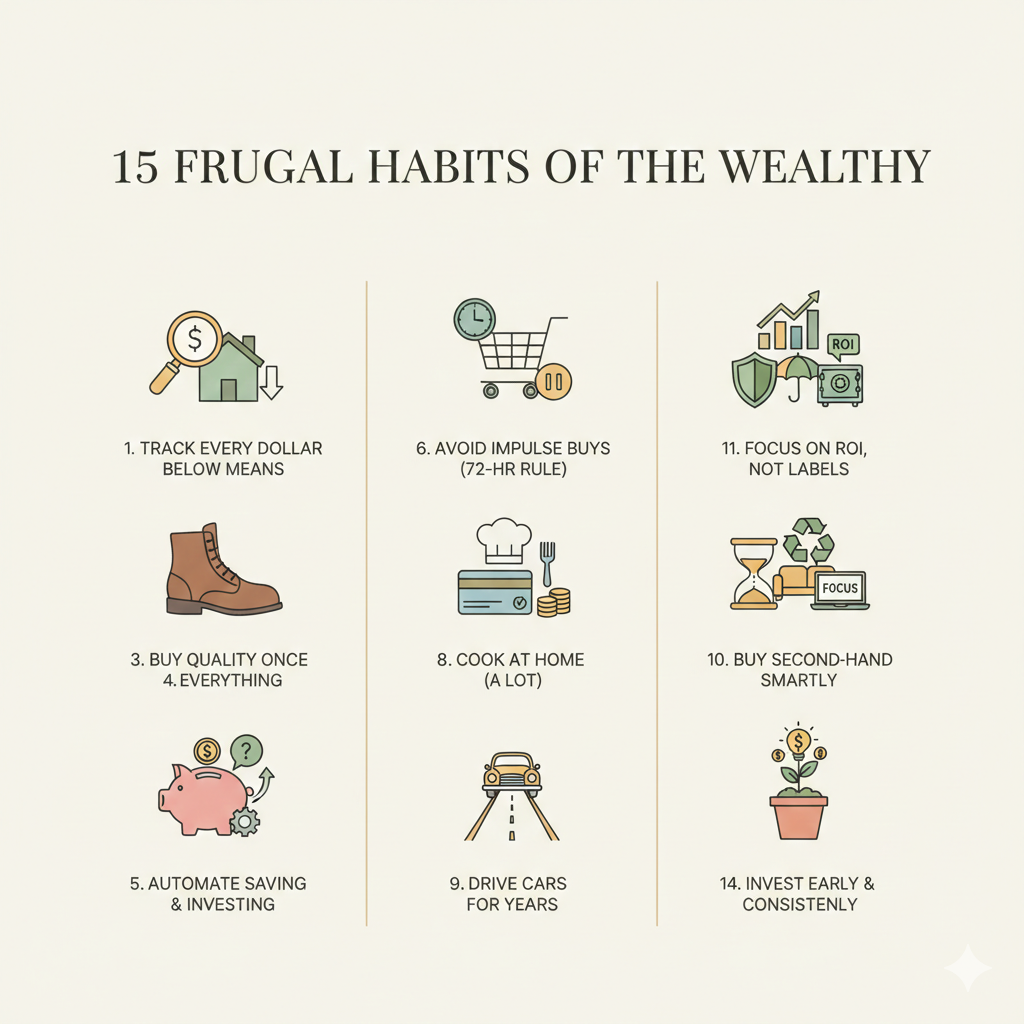

Wealthy individuals do not guess their net worth; they measure it. Tracking every dollar is the foundational habit of fiscal mastery. By monitoring spending on a weekly or monthly basis, one eliminates “financial leaks.” In modern wealth management, this involves using high-level tracking tools to categorize every transaction, ensuring that capital is directed toward appreciating assets rather than evaporating through unmonitored lifestyle costs.

2. Defeating Lifestyle Inflation

“Living below your means” is a mathematical necessity for wealth. As income rises, the average consumer increases their spending to match. The wealthy, however, cap their lifestyle inflation. By maintaining a fixed cost of living even as earnings grow, they create a widening “wealth gap” the surplus capital used for investment.

3. The “Buy Quality Once” Doctrine

There is a high cost to being cheap. The wealthy practice the “Buy It For Life” (BIFL) philosophy. Investing in high-quality shoes, tools, and furniture may have a higher upfront cost, but it eliminates the cycle of frequent replacements. This reduces the long-term “cost per use,” making high-quality goods a more frugal choice than their cheaper, disposable counterparts.

4. Professional Negotiation as a Standard

Nothing is “fixed” in a global economy. From insurance premiums and medical bills to salary and rent, the wealthy view every financial interaction as a negotiation. By consistently researching market rates and advocating for better terms, they save thousands annually on recurring costs that others simply accept as inevitable.

5. The Power of Financial Automation

Willpower is a finite resource. To ensure consistent growth, the wealthy automate their savings and investments. By directing capital into brokerage accounts or retirement funds before it ever reaches a checking account, they treat savings as a “non-negotiable expense.” This “pay yourself first” model ensures that wealth grows in the background of daily life.

6. The 24-72 Hour Rule for Impulse Control

Impulse purchases are the enemy of capital preservation. To combat the dopamine-driven urge to spend, wealthy individuals implement a mandatory waiting period typically 24 to 72 hours for any non-essential purchase. This allows the emotional impulse to subside, replaced by a rational evaluation of the item’s true utility.

7. Strategic Credit Management

The wealthy do not fear credit; they leverage it. By using credit cards for their cashback and rewards programs and paying the balance in full every month they essentially receive a discount on all necessary spending. They treat credit as a tool for liquidity and rewards, never as a source of high-interest debt.

8. Culinary Discipline: The Home-Cooked Advantage

In major financial centers, the cost of dining out is a significant drain on potential investment capital. The wealthy view restaurants as occasional luxuries rather than daily necessities. By cooking at home, they gain control over both their financial health and their physical well-being, avoiding the “convenience tax” associated with the food service industry.

9. Depreciating Asset Management: The Vehicle Strategy

A car is a tool, not a trophy. The wealthy tend to drive vehicles for many years, often five to ten years beyond the payoff date. By ignoring the “new model” cycle, they avoid the steepest curve of depreciation, ensuring they get maximum value per mile driven.

10. Smart Second-Hand Acquisition

For items that depreciate rapidly such as luxury furniture, cars, and certain electronics the wealthy often buy second-hand. They let the original owner take the initial 30-50% hit in depreciation. This “smart sourcing” allows them to own premium goods at a fraction of the retail price.

11. ROI vs. Labels: The Asset Mindset

Status brands are often marketed toward those trying to look wealthy, not those who actually are. The wealthy focus on the intrinsic value and ROI of a purchase. They would rather invest $1,000 in an index fund or a skill-based certification than in a designer handbag that offers no functional or financial return.

12. Robust Risk Management

Protecting money is as important as making it. This involves a three-pronged approach:

- Emergency Funds: Maintaining 6-12 months of liquid expenses.

- Insurance: Ensuring adequate coverage for health, life, and property.

- Diversification: Spreading assets across different sectors to mitigate market volatility.

13. Temporal Budgeting: Time as Currency

Time is the only non-renewable resource. Wealthy individuals budget their hours with the same intensity they budget their dollars. They eliminate low-value activities (like excessive social media or television) in favor of “income-producing work” or high-value rest, understanding that their hourly rate is their most important financial metric.

14 & 15. The Compound Interest Mandate: Invest Early and Often

The final and most critical habit is the commitment to early and consistent investment. Whether it is through small monthly contributions to an ETF or reinvesting business profits, the wealthy utilize the mathematical force of compounding. By starting early even with small amounts they allow time to do the heavy lifting of wealth creation.

Conclusion: Implementing the Wealth Blueprint

Achieving a high net worth is rarely the result of a single “lucky” event. Instead, it is the cumulative result of these fifteen habits. By shifting from a mindset of consumption to one of strategic accumulation, anyone can build a stable and prosperous financial future.