Vital Money Lessons for Teenagers

Teenagers can build long-term financial security by mastering fundamental money habits early. Key lessons include understanding the difference between assets and liabilities, creating a basic budgeting system, and grasping the power of compound interest. By learning to save consistently and avoiding high-interest consumer debt, teens establish a strong financial foundation for life. 📈🏦

The Financial Blueprint: Crucial Money Lessons Every Teenager Needs to Master Early 🚀

We teach teenagers algebra, chemistry, and history, but we rarely teach them how to balance a bank account or grow their savings. The result? Millions of young adults enter the real world with a high school diploma in one hand and a mountain of avoidable financial confusion in the other. 🎓❌

The habits formed during your teenage years don’t just stay in your youth; they set the exact trajectory for your financial future. Learning the rules of money early acts like a financial superpower, giving you a massive head start before life gets expensive. Let’s break down the essential money lessons that turn teenagers into financially free adults. 🌟✨

Why Waiting Until Adulthood to Learn Finance is a Costly Mistake 📉

Many people believe that financial planning is something you only worry about once you land your first “real” career. But your brain learns habits best when you are young.

If you wait until your mid-twenties to understand cash flow, you will likely spend your first few working years paying for rookie mistakes like credit card debt or impulse buying traps. Building a solid financial system during your teens ensures you never have to play catch-up with your wealth. 🧠💸

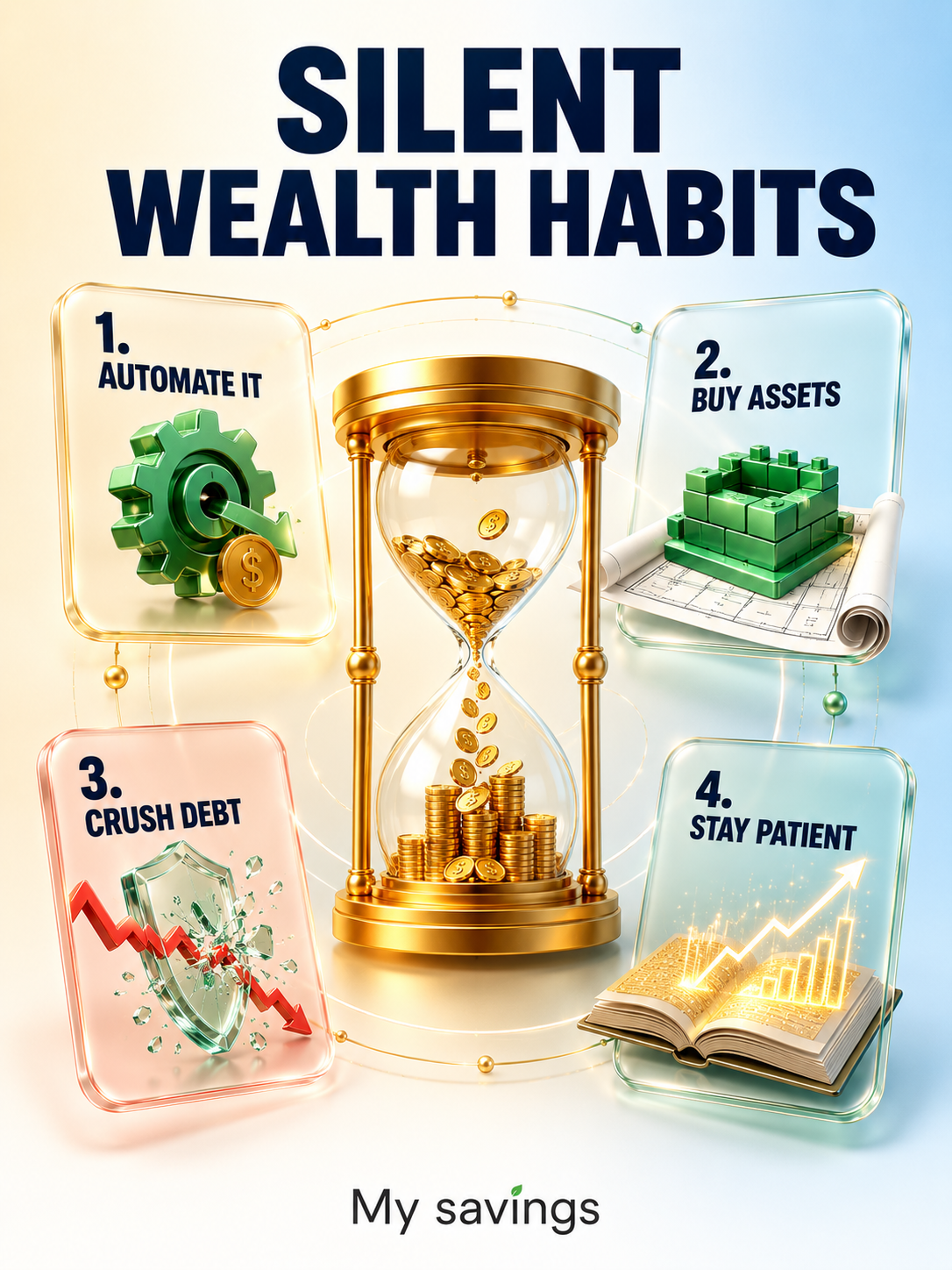

1. Assets vs. Liabilities: Knowing What Puts Money in Your Pocket 💸

The absolute core of financial intelligence comes down to understanding the golden rule established by elite wealth managers: the difference between an asset and a liability.

- What is an Asset? An asset is anything that puts money into your pocket over time. Examples include high-yield savings accounts, index funds, or an automated small business.

- What is a Liability? A liability is anything that takes money out of your pocket. This includes subscriptions you don’t use, expensive clothes bought on credit, or an overpriced vehicle. 🏎️

- The Secret to Wealth: True financial freedom comes from consistently accumulating assets while minimizing liabilities as early as humanly possible.

2. The Power of Compound Interest: The Ultimate Early-Start Advantage ⏳

There is one resource that teenagers have more of than any billionaire on Earth: time. Time is the magical engine that drives compound interest.

Compound interest is when the interest you earn on your money begins to earn interest on itself. If you save $100 a month starting at age 15, that money has decades to snowball quietly in the background. Starting just ten years later at age 25 means you have to save twice as much money to achieve the exact same retirement goal. Time is money, and starting early is the ultimate cheat code. 📈

3. The 50/30/20 Budgeting Rule: Creating Structure Without Sacrificing Fun 🍕

Budgeting shouldn’t feel like a punishment. If your financial system is too restrictive, you will eventually abandon it. The best way for teens to manage an allowance or a part-time job wage is the 50/30/20 rule.

- 50% for Needs: Dedicate half of your income to absolute essentials like school supplies, transportation, or basic food costs.

- 30% for Wants: Allocate nearly a third of your money to the things that make life fun—concert tickets, video games, or hanging out with friends. 🎮

- 20% for Savings: Instantly move a fifth of your paycheck into an automated savings or investment account before you spend a single dime.

4. Avoiding the Consumer Debt Trap: Protecting Your Future Paycheck 💳

We live in a world that constantly encourages us to “Buy Now, Pay Later.” Credit cards and instant loan apps are marketed as symbols of adult freedom, but they are often financial traps.

Debt is simply borrowing money from your future self. When you buy things you can’t afford on credit, you commit your future income to paying off past purchases plus hefty interest fees. Treat credit cards with absolute respect they are tools for building credit history, not magic cards for free shopping sprees. 🛑🛒

5. Building an Emergency Fund: Preparing for Life’s Unexpected Events 🛡️

One of the quickest ways to fall into bad debt is being unprepared for an emergency. Life is unpredictable, and accidents happen whether you are 16 or 60.

- The Starter Cushion: Aim to build a basic emergency fund of at least three to six months of your typical expenses.

- Peace of Mind: Knowing you have money set aside if your phone screen cracks or your car needs a sudden repair removes massive amounts of anxiety. 📱🔧

- Hands-Off Money: This fund lives in a separate account and is strictly off-limits for casual shopping or weekend plans.

6. Understanding Opportunity Cost: Every Choice Has a Hidden Price 🎯

Every time you spend money on one item, you are automatically deciding not to spend that same money on something else. This concept is known as opportunity cost.

Before you spend $100 on a trendy pair of shoes that will go out of style next season, ask yourself: “What else could this money do for me?” That same $100 could fund a small online business idea or purchase fractional shares in your favorite technology companies. When you shift your perspective from what you are buying to what you are giving up, your spending habits change completely. ⚖️

7. Investing in Yourself: The Highest-Yield Return on Earth 📚💪

While stocks and savings accounts are excellent, the absolute best investment a teenager can make is an investment in their own skills and financial knowledge.

Read books about personal finance, learn how digital marketing platforms work, or take an online course on coding. The skills you acquire in your teenage years will dictate your earning potential for the rest of your life. While market investments fluctuate, an enhanced skill set can never be taken away from you and will pay dividends forever.

Transforming Small Teenage Habits Into Lifelong Prosperity 🌟

Building a wealthy future doesn’t require a massive inheritance or an immediate high-paying career. It is the natural result of reliable, quiet daily habits formed during your youth. As we’ve explored, the basics of financial literacy from managing compound interest to understanding assets are the tools that protect you from stress and grant you total control over your destiny.

Don’t wait for adulthood to start managing your money; build the foundation now so your money can start working for you. When you turn financial discipline into a standard lifestyle early on, success becomes inevitable. 🌳🪙

Are you ready to take control of your financial path and build a secure future? Explore our premium tools, expert guides, and wealth-building tips at growmymoney.top today! Let’s build your financial superpower together! 🚀✨