Navigating the complexities of personal finance requires more than just good intentions; it demands structured, actionable strategies. This comprehensive guide details the seven fundamental rules for saving money, designed to help individuals build wealth, mitigate financial risk, and achieve long-term economic stability. By exploring proven methodologies such as the 50/30/20 budget framework, the mathematical predictability of the Rule of 72, and the psychological benefits of the 1% impulse buy rule, this article provides a robust blueprint for financial management. Additionally, it delves into the crucial mechanisms of automated savings, emergency fund calculation, employer-matched retirement contributions, and the financial advantages of minimalism through the “Item In, Item Out” philosophy. Whether you are beginning your financial journey or looking to optimize an existing portfolio, integrating these seven objective rules into your financial planning will establish a resilient foundation for sustainable economic growth and security.

Introduction to Strategic Wealth Management

In contemporary economic environments marked by fluctuating inflation rates and market volatility, achieving financial security requires a disciplined and objective approach to money management. Relying on intuition or ad-hoc saving habits is rarely sufficient for building sustainable wealth. Instead, financial experts advocate for the adoption of structured methodologies that govern spending, saving, and investing behaviors. By implementing systematic frameworks, individuals can remove emotional decision-making from their financial planning, optimizing their capital allocation for maximum growth and security. The following seven rules represent the core tenets of modern personal finance, offering a blueprint for efficient money management and long-term financial independence.

1. The 50/30/20 Budget Rule: Structured Capital Allocation

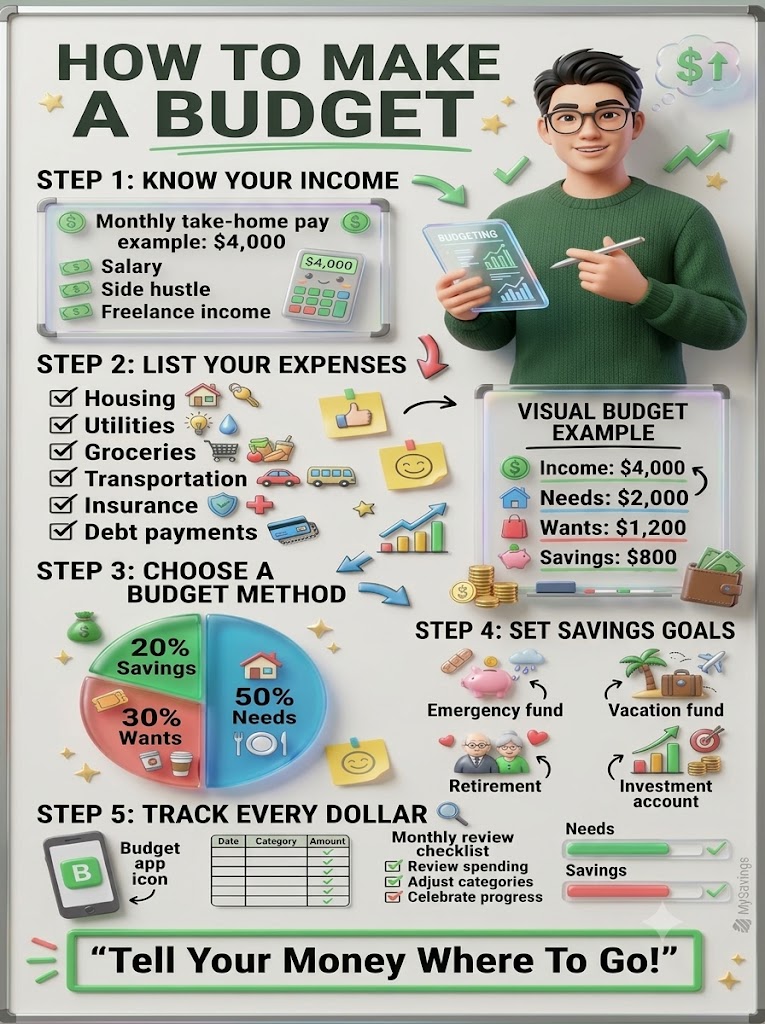

The foundation of any sound financial strategy is a well-defined budget. The 50/30/20 rule provides an intuitive, highly effective framework for allocating after-tax income into three distinct operational buckets: Needs, Wants, and Savings.

- 50% Needs (Essential Expenses): Half of one’s net income should be dedicated to absolute necessities. These are the expenses required to maintain a baseline standard of living. Categories within this bucket include housing (rent or mortgage payments), basic utilities (electricity, water, sanitation), groceries, essential transportation (car payments, gas, public transit passes), and mandatory insurance premiums (health, auto, home).

- 30% Wants (Discretionary Spending): This bucket acknowledges that sustainable budgeting must accommodate lifestyle choices and psychological well-being. Up to 30% of income can be allocated to non-essential expenses. This includes dining out, travel, fashion, entertainment, hobbies, and subscription services. By capping discretionary spending at 30%, individuals can enjoy their income without compromising their financial future.

- 20% Savings (Wealth Accumulation and Debt Reduction): The final 20% is the engine of financial growth. This critical allocation is directed toward building an emergency fund, making accelerated debt payments (beyond minimum requirements), investing in the stock market or real estate, and funding retirement accounts. Consistently directing a minimum of one-fifth of income toward wealth-building activities is a primary driver of long-term financial independence.

2. The Rule of 72: Forecasting Compound Interest

Understanding the mechanics of compound interest is essential for effective investment planning. The Rule of 72 is a simplified mathematical formula used by economists and investors to estimate the number of years required to double the value of an investment at a fixed annual rate of return.

To utilize this rule, divide the number 72 by the anticipated annual interest rate.

- Formula: 72 / Interest Rate = Years to Double

- Example Calculation: If an investment portfolio yields an average annual return of 8%, the calculation would be 72 / 8 = 9. Therefore, it will take approximately 9 years for the initial capital to double in value.

The Rule of 72 serves as a powerful psychological tool, getting individuals excited about saving and investing by making the abstract concept of compound growth tangible and predictable. It underscores the importance of seeking out higher-yield investment vehicles, as even a small increase in the interest rate significantly reduces the time required for wealth multiplication.

3. The 1% Rule for Impulse Buys: Behavioral Finance Controls

Behavioral economics suggests that humans are prone to impulse purchases driven by temporary emotional states and the desire for instant gratification. The 1% Rule acts as a systemic safeguard against unplanned, budget-derailing expenses.

The rule dictates that if an individual wishes to purchase a non-essential item that costs more than 1% of their annual gross income, they must institute a mandatory three-day waiting period before executing the transaction.

- Practical Application: For an individual earning $60,000 annually, the 1% threshold is $600. If an item exceeds this amount, the purchase is paused for 72 hours.

- Psychological Mechanism: This enforced delay separates the emotional desire from the transactional action. By the end of the three-day period, the initial dopamine rush associated with the potential purchase typically subsides. Consequently, consumers frequently realize that the item is not a genuine need or a highly valued want, thereby preventing capital misallocation.

4. The 401(k) Match Rule: Optimizing Employer Benefits

In the realm of retirement planning, employer-sponsored defined contribution plans, such as a 401(k), often feature a matching contribution program. The 401(k) Match Rule states that an employee must maximize their retirement contributions up to the exact percentage matched by their employer.

Many employers offer to match a portion of an employee’s retirement contributions (e.g., a 100% match on the first 3% of the employee’s salary, or a 50% match up to 6%). This matching contribution represents a guaranteed, risk-free return on investment.

Failing to contribute enough to capture the full employer match is economically equivalent to rejecting free money and taking a voluntary pay cut. Optimizing this benefit is arguably the most critical and time-sensitive rule of wealth accumulation, as it instantly accelerates compounding growth in tax-advantaged retirement accounts.

5. The 3X Emergency Fund Rule: Risk Mitigation Strategies

Financial stability requires a buffer against unpredictable macroeconomic shocks, such as sudden unemployment, severe medical emergencies, or catastrophic property damage. The 3X Emergency Fund Rule mandates that individuals maintain a minimum of three to six times their monthly living expenses in a highly liquid, easily accessible account.

- Calculating the Target: This calculation should be based on the “Needs” bucket identified in the 50/30/20 rule, rather than total gross income. If essential monthly expenses total $3,000, the baseline emergency fund must be at least $9,000 to $18,000.

- Strategic Storage: These funds should be housed in low-risk, accessible vehicles, such as a High-Yield Savings Account (HYSA). While they may not outpace high inflation, the primary purpose of an emergency fund is capital preservation and immediate liquidity, not aggressive growth. When a “rainy day” inevitably arrives, this cash reserve ensures that individuals can weather the storm without resorting to high-interest consumer debt.

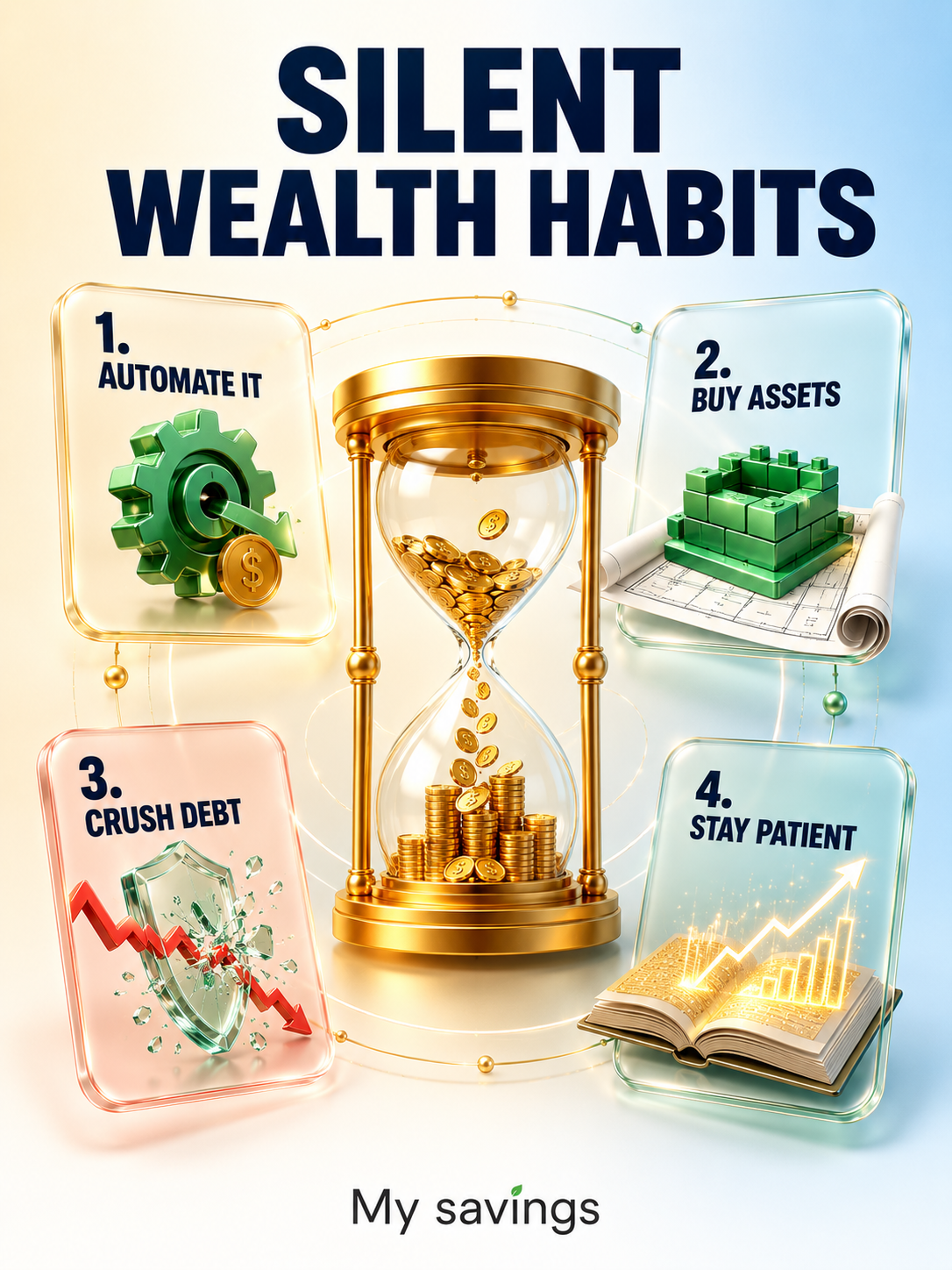

6. The Rule of Automation: Engineering Financial Discipline

Human behavior is heavily influenced by convenience. The Rule of Automation leverages this psychological reality by making the act of saving the default, frictionless option. Behavioral finance studies consistently show that “defaults are powerful because people are lazy” or, more accurately, because people suffer from decision fatigue.

To successfully implement this rule, individuals must engineer an automated financial system. This involves configuring direct deposits and automated bank transfers so that investment and savings contributions are immediately withdrawn on payday, before the capital ever reaches an active checking account.

By saving and investing money before it is ever “seen” or available for discretionary spending, individuals effectively “pay themselves first.” This systemic approach removes the need for monthly willpower, guaranteeing that wealth-building targets are met consistently regardless of external emotional or temporal factors.

7. The Item In, Item Out Rule: The Economics of Minimalism

Physical clutter directly correlates to financial clutter. The “Item In, Item Out” rule is rooted in the philosophy of minimalism, framed here as a dual discipline of managing both inbound and outbound possessions.

The rule stipulates that for every new non-consumable item brought into a household, an existing item of equal or greater size must be removed (donated, sold, or recycled).

This strategy prevents the silent wealth-killer known as lifestyle creep the tendency to continuously acquire more possessions as income rises. By forcing an evaluation of existing inventory before making new purchases, consumers naturally decrease their rate of consumption. Maintaining this physical equilibrium curtails unnecessary spending, reduces the hidden costs of storage and maintenance, and redirects capital back toward the 20% savings and investment bucket.

Conclusion

Mastering personal finance is not an arbitrary exercise; it is the execution of calculated, objective strategies over an extended period. By rigidly applying the 50/30/20 budget framework, leveraging the Rule of 72, curbing impulse spending, maximizing employer matches, safeguarding against risk with an emergency fund, automating financial systems, and controlling consumption through minimalism, individuals can systematically construct a robust financial future.