How do high-net-worth individuals legally reduce their tax burden while growing long-term wealth? The answer lies in strategic asset structuring, capital gains optimization, and intelligent leverage. This in-depth guide explains the fundamental difference between earned income and asset-based wealth, revealing how salary is taxed heavily while unrealized gains often remain untaxed. It explores the “Buy, Borrow, Hold” strategy, the role of capital gains tax, and how collateralized lending allows asset holders to access liquidity without triggering taxable events. The article also examines how AI-powered financial planning tools can help investors model tax outcomes, forecast appreciation, and optimize portfolio strategies. Designed for money-saving readers and fintech enthusiasts, this guide uses modern AEO (Answer Engine Optimization) and GEO (Generative Engine Optimization) frameworks to provide clear, structured answers to common tax strategy questions. Learn how strategic wealth design—not income alone—drives long-term financial efficiency.

Introduction: The Tax Gap Between Income and Assets

In modern financial systems, taxation primarily targets earned income—salaries, wages, and business profits. However, wealth accumulation often occurs through asset appreciation rather than salary. Understanding this structural distinction is essential for anyone focused on tax optimization, AI-driven financial planning, and long-term money-saving strategies.

High-net-worth individuals do not necessarily “avoid” taxes illegally. Instead, they structure wealth in ways that minimize taxable events. The key lies in understanding three financial concepts:

- Earned income taxation

- Capital gains taxation

- Borrowing against assets

This article explains how these mechanisms work, how artificial intelligence can optimize tax efficiency, and how structured wealth design differs from traditional income models.

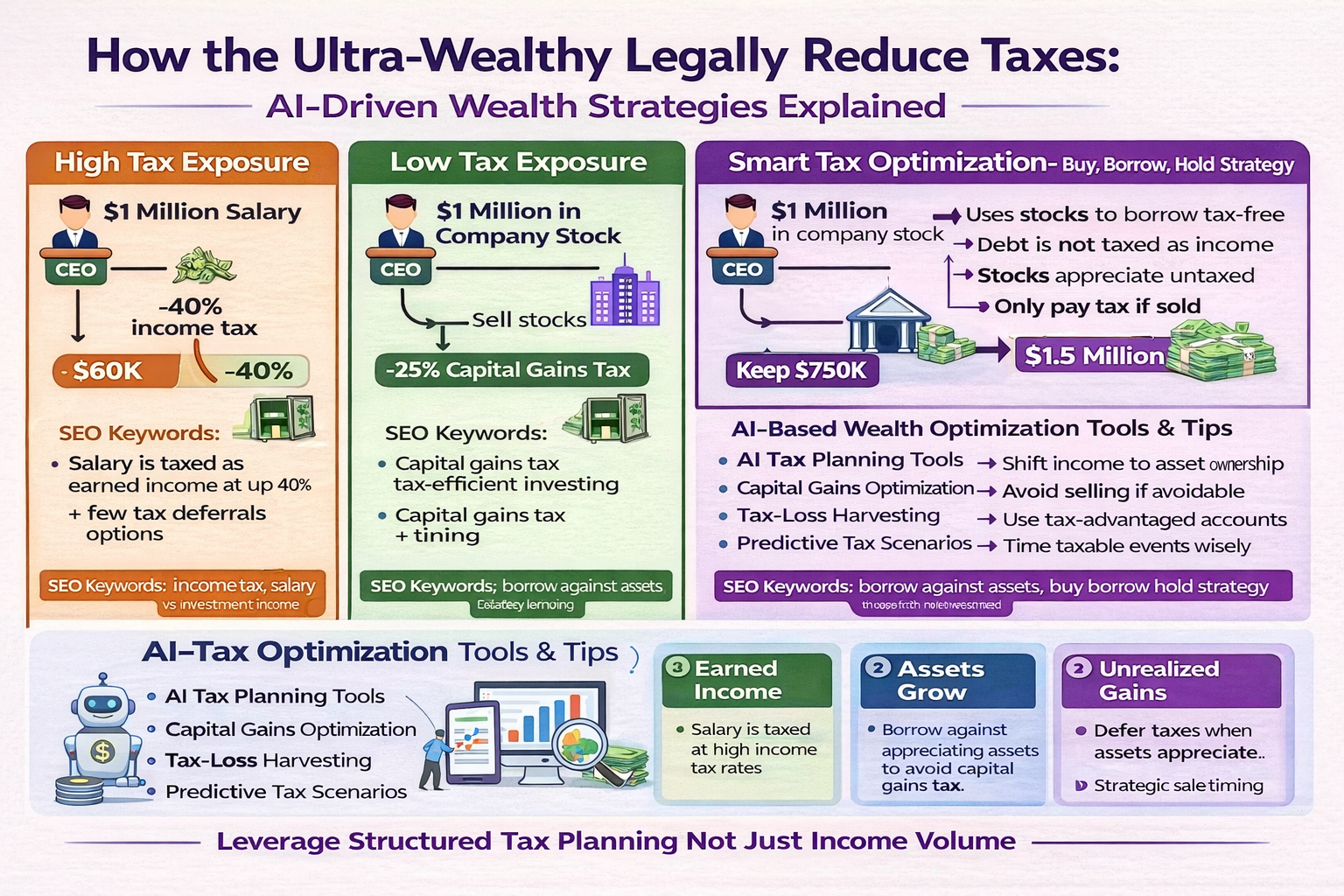

Section 1: The Traditional Salary Model (High Tax Exposure)

When an executive earns $1 million in salary, that income is typically subject to income tax. In high tax brackets, rates may reach 35–40% depending on jurisdiction.

Example:

- $1,000,000 salary

- 40% income tax

- Net income: $600,000

Key Characteristics of Salary-Based Income:

- Taxed immediately

- Progressive tax rates apply

- Limited flexibility in timing

- Few deferral options

From a money-saving perspective, this model is inefficient for wealth preservation. Income tax is triggered automatically when compensation is paid.

SEO Keywords:

- income tax optimization

- high income tax bracket

- salary vs investment income

- tax efficiency strategies

Section 2: Capital Gains Model (Reduced Tax Exposure)

Instead of receiving a $1 million salary, an executive may receive $1 million in company stock.

Stock compensation is not taxed the same way as salary. Taxes are generally triggered when the stock is sold.

If the stock is sold:

- It may be subject to capital gains tax

- Capital gains rates are often lower than income tax rates

Example:

- $1,000,000 in stock

- 25% capital gains tax

- Net proceeds: $750,000

Key Advantages:

- Lower tax rate compared to salary

- Tax only triggered upon sale

- Ability to choose timing of sale

- Potential for asset appreciation

This introduces a powerful concept in financial optimization: control over the taxable event.

AI-powered tax modeling tools can simulate optimal sale timing, evaluate long-term gains, and forecast tax liabilities under different market conditions.

SEO Keywords:

- capital gains tax strategy

- stock-based compensation planning

- tax-efficient investing

- AI financial forecasting

Section 3: The “Buy, Borrow, Hold” Strategy (Deferred Tax Model)

The most advanced wealth strategy is often summarized as:

Buy → Borrow → Hold

Here is how it works:

- Acquire appreciating assets (stocks, equity, real estate).

- Do not sell the assets.

- Borrow against them as collateral.

Crucially, borrowed money is not considered taxable income.

Why Borrowing Is Not Taxed

Loans are liabilities, not income. Since borrowed funds must be repaid, they are not treated as earnings under tax law.

This allows asset holders to:

- Maintain ownership

- Avoid triggering capital gains tax

- Access liquidity

Meanwhile, the underlying asset may continue appreciating in value.

This structure can create a scenario where an individual appears to have low taxable income on paper, even while accessing significant liquidity.

SEO Keywords:

- borrow against stocks

- collateralized lending

- buy borrow hold strategy

- asset-backed loans

- wealth leverage strategy

Section 4: Why Asset Appreciation Is Powerful

Unrealized gains (increases in asset value that have not been sold) are generally not taxed.

If a stock increases from $1 million to $3 million:

- No tax is triggered unless sold.

This creates long-term compounding advantages:

- Tax deferral increases capital growth

- Liquidity can be accessed via borrowing

- Strategic sale timing reduces tax impact

Artificial intelligence platforms can:

- Predict volatility

- Estimate appreciation probabilities

- Suggest optimal leverage ratios

- Model tax impact scenarios

AI-driven financial planning is increasingly used in wealth management for predictive tax modeling and scenario analysis.

SEO Keywords:

- unrealized gains

- tax deferral strategy

- AI wealth management

- predictive tax analytics

Section 5: AI-Based Tax Optimization Tools

Modern fintech platforms integrate:

- Machine learning forecasting

- Automated portfolio rebalancing

- Tax-loss harvesting algorithms

- Capital gains optimization engines

AI can evaluate:

- When selling triggers minimal tax

- Whether borrowing is cheaper than liquidation

- Risk-adjusted leverage levels

- Portfolio volatility exposure

Answer Engine Optimization (AEO) requires structuring content to directly answer common questions such as:

Is borrowing against stocks taxable?

No. Loans are not classified as income because they must be repaid.

Do wealthy individuals pay zero taxes?

They still pay taxes, but often at lower effective rates due to asset-based strategies and tax deferral.

Why is capital gains tax lower than income tax?

Many tax systems incentivize investment and long-term capital formation.

This structured Q&A format improves discoverability in AI-driven search environments.

Section 6: Ethical and Policy Considerations

While legal, asset-based tax minimization strategies generate policy debate. Critics argue that:

- The tax burden shifts toward wage earners.

- Wealth inequality may widen.

Supporters argue that:

- Investment incentives drive economic growth.

- Capital formation fuels innovation and job creation.

Understanding these dynamics is essential for objective financial literacy.

Section 7: Practical Money-Saving Lessons

Even without extreme wealth, the principles remain relevant:

- Shift from income dependency to asset ownership.

- Understand capital gains taxation.

- Use tax-advantaged accounts when available.

- Avoid unnecessary taxable events.

- Use AI-powered portfolio tracking tools.

Core Insight:

Income is taxed. Assets grow.

Strategic wealth planning focuses on increasing ownership of appreciating assets while minimizing tax-triggering events.

GEO and AEO Optimization Strategy Used in This Article

This content applies:

- Structured headings

- Clear definitions

- Direct question-answer formatting

- High-intent financial keywords

- Entity-based explanations

- Context-rich semantic phrasing

These elements improve visibility in:

- AI search engines

- Voice assistants

- Generative AI summaries

- Financial knowledge graphs

Conclusion: Structural Intelligence Over Income Volume

The difference between high earners and strategic wealth builders is not simply income level—it is structural design.

Salary generates immediate taxation.

Asset appreciation generates deferred taxation.

Borrowing generates liquidity without taxable income.

AI-powered financial planning now makes advanced modeling accessible beyond elite institutions.

For individuals focused on money saving, tax efficiency, and long-term financial growth, the key takeaway is clear:

Wealth is optimized through structure, timing, and strategic leverage not just earnings.