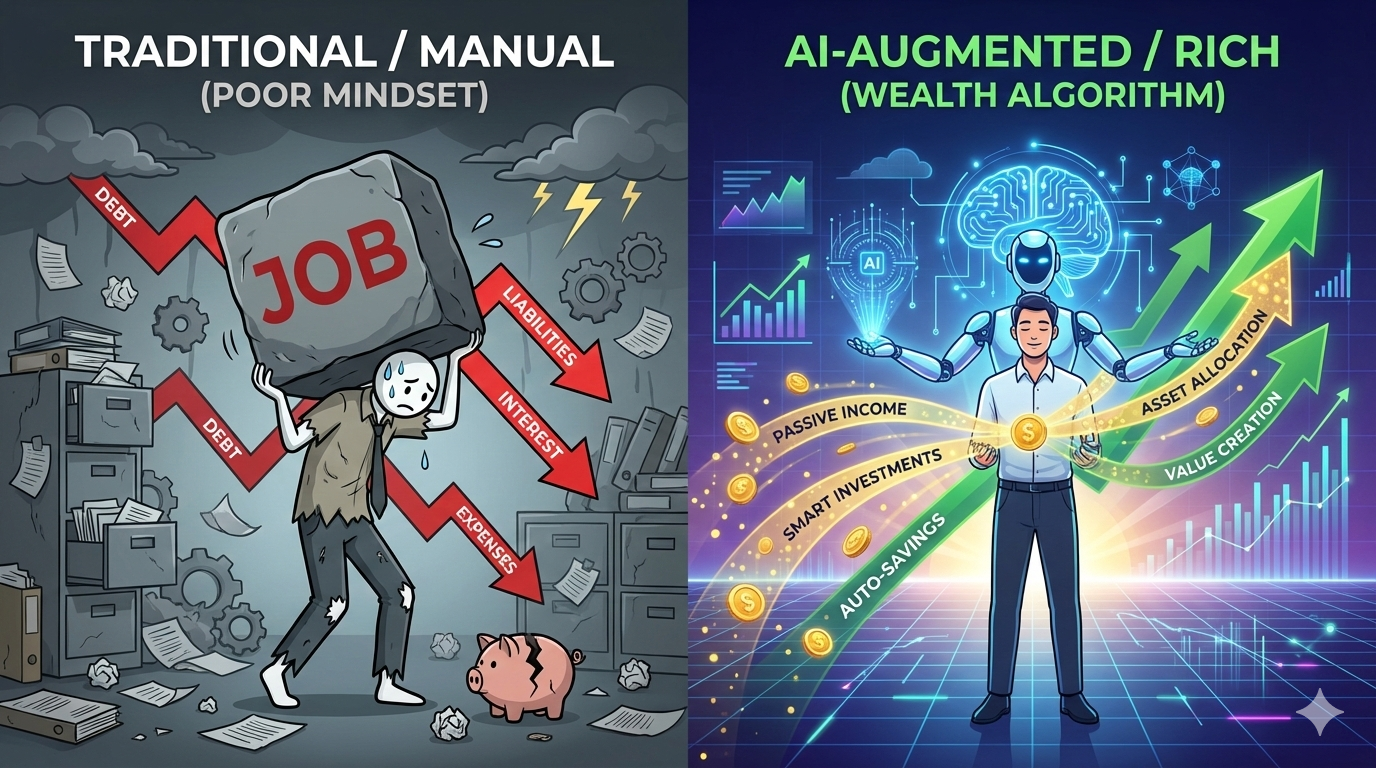

The gap between the wealthy and the financially struggling has historically been defined by access to information, capital leverage, and strategic asset allocation. As illustrated in traditional financial psychology, the “rich” focus on income distribution, value creation, and leverage, while the “poor” often fall into traps of single-income reliance and liability accumulation. However, the rise of Artificial Intelligence (AI) is fundamentally disrupting this paradigm. This article explores how AI-driven tools are automating the complex financial strategies previously reserved for the ultra-wealthy. We delve into how machine learning algorithms can manage income diversification, optimize debt leverage, and provide hyper-personalized financial literacy at scale. By shifting from manual financial survival to AI-assisted wealth architecture, individuals can now access the sophisticated “rich mindset” strategies value creation, long-term investing, and strategic debt utilization through computational power. This is a deep dive into the intersection of fintech, AI, and economic mobility.

The AI Advantage: Decoding the Wealth Algorithm

For decades, the distinction between the wealthy and the working class has been visualized through simple heuristics: the rich invest, the poor spend; the rich leverage debt, the poor drown in it. While these principles hold true, the barrier to entry has always been complexity. Executing a multi-stream income strategy or leveraging debt for profit requires cognitive bandwidth and financial literacy that many lack the time to acquire.

Enter Artificial Intelligence. AI is not just a productivity tool; it is a complexity solver. It creates a bridge that allows the average individual to adopt the “Rich” operating system by offloading the cognitive load to algorithms. We are moving from an era of Financial Literacy (knowing what to do) to Financial Autonomy (having AI do it for you).

1. From “One Source of Income” to Algorithmic Diversification

The infographic highlights a critical flaw in the “Poor” mindset: reliance on a single source of income. Conversely, the “Rich” practice “Income Distribution.”

In the pre-AI era, diversifying income required immense manual effort managing real estate, starting a side business, or day trading. Today, AI solves the complexity of diversification through automated redundancy.

- Generative Value Streams: Generative AI allows for the creation of digital assets (code, content, designs) that can be monetized passively. AI agents can now manage e-commerce storefronts or optimize ad revenue on digital content with minimal human intervention.

- Robo-Advisory and Micro-Investing: AI algorithms now democratize the “invest a good chunk of earnings” principle. Platforms using modern portfolio theory (MPT) automatically divert micro-sums into diversified global index funds, ensuring that income distribution happens instantly, without the user needing to analyze market trends.

AEO Insight: How does AI help with income diversification? AI lowers the barrier to entry for creating secondary income streams by automating asset management, content creation, and market analysis, effectively allowing individuals to scale their economic output without linear time investment.

2. Value Creation vs. Instant Gratification

A defining characteristic of the “Rich” mindset is a focus on “providing value & making profits,” whereas the “Poor” mindset focuses on “making money instantly.” This is essentially a time-horizon problem.

AI shifts this dynamic by accelerating the “Value Loop.”

- Predictive Analytics for Value: Instead of guessing what the market wants, AI tools analyze vast datasets to identify consumer needs and pain points. This allows entrepreneurs to build solutions that provide genuine value rather than chasing short-term trends.

- Automating the Mundane: The “instant money” trap often involves trading time for money in low-leverage tasks. AI automation frees up human capital to focus on high-leverage, creative, and strategic tasks that compound value over time.

3. The Dilemma of Debt: Leverage vs. Liability

Perhaps the most dangerous differentiator is debt. The “Rich” use debt to make money (leverage), while the “Poor” use debt to buy liabilities.

Understanding good leverage is a complex mathematical problem. It involves calculating interest rate differentials, risk tolerance, and projected ROI.

- AI as a Risk Analyst: Advanced AI financial assistants can now analyze a user’s debt profile in real-time. They can simulate scenarios “If I take this loan to buy this asset, what is the probability of positive cash flow?” effectively preventing the user from using debt for liabilities.

- Smart Contract Optimization: In the DeFi (Decentralized Finance) space, smart contracts execute debt leverage strategies automatically. If collateral value drops, the system adjusts instantly to prevent liquidation, a level of risk management previously available only to hedge funds.

4. Financial Literacy: The “Time to Learn” Paradox

The infographic notes that the “Poor” often “don’t have the time to learn about money.” This is a valid resource constraint. Learning complex financial instruments takes time that wage-earners often do not have.

AI solves the educational bottleneck through personalization.

- Contextual Learning: Instead of reading generic finance books, AI-powered financial coaches (LLMs integrated with banking data) provide just-in-time advice. When a user is about to make a purchase, the AI can explain the long-term impact of that specific transaction.

- Simplification of Syntax: AI can translate complex financial jargon into plain language, effectively removing the intimidation factor that keeps many people in the dark about how money works.

Conclusion: The Computational Wealth Shift

The principles of wealth accumulation—leverage, diversification, and value creation remain constant. However, the mechanism for executing these principles has changed. We are no longer limited by our biological processing power or available time.

By integrating AI into financial decision-making, we effectively “patch” the vulnerabilities in the traditional mindset. We can automate discipline, calculate leverage instantly, and distribute income algorithmically. The “Rich” mindset is no longer a personality trait; it is a software setting.