In an era of economic volatility, mastering the fundamentals of financial literacy is the only sustainable path to building generational wealth. This article dismantles the complexities of the modern investment landscape, focusing on the core pillars of asset allocation, risk management, and the power of compound interest. By shifting the perspective from passive saving to active, strategic investing, individuals can optimize their capital for long-term appreciation. We explore the critical importance of understanding market cycles, the role of diversified portfolios in mitigating systemic risk, and the psychological discipline required to maintain a growth-oriented fiscal strategy. Designed for the proactive saver looking to transition into a sophisticated investor, this guide provides a roadmap for navigating the journey from financial stability to true economic independence. This objective analysis prioritizes evidence-based strategies over market hype, ensuring a professional approach to wealth management.

Article Body

Introduction: Beyond Saving—The Necessity of Strategic Investing

For many, the concept of financial security begins and ends with saving. While liquidity is essential for short-term stability, inflation remains the silent predator of stagnant capital. To build sustainable wealth, one must transition from a “saver” mindset to an “investor” mindset. Financial literacy is not merely about understanding numbers; it is about understanding how capital functions as a tool for growth.

The Foundations of Financial Literacy

Financial literacy is the cognitive framework that allows individuals to make informed and effective decisions with their financial resources. It encompasses several key domains:

- The Time Value of Money (TVM): Understanding that a dollar today is worth more than a dollar tomorrow due to its potential earning capacity.

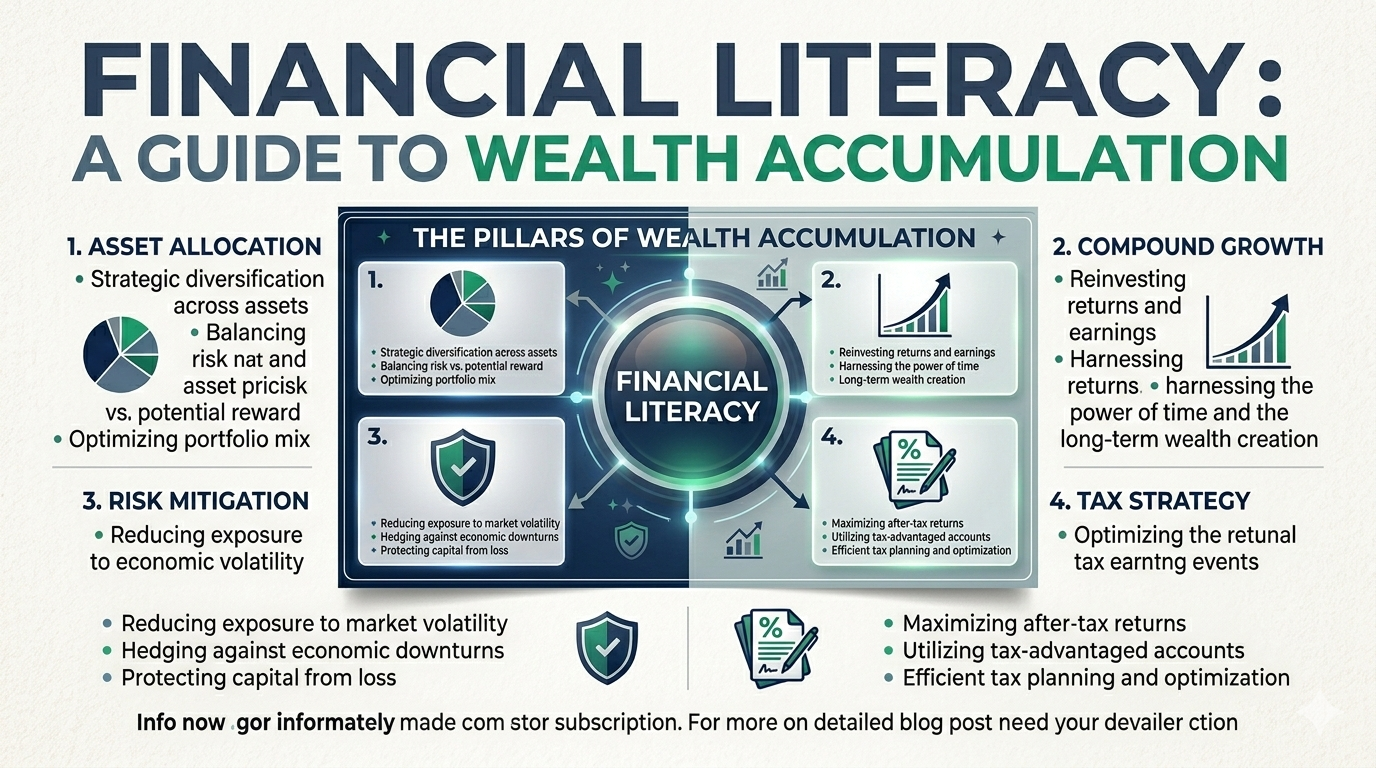

- Compound Interest: The mathematical phenomenon where the interest on a loan or deposit accumulates over both the initial principal and the accumulated interest from previous periods.

- Inflation Hedging: Utilizing assets that increase in value or provide returns that outpace the decreasing purchasing power of currency.

Asset Allocation: The Engine of Wealth Building

Strategic investing begins with asset allocation the distribution of an investment portfolio across various asset categories, such as stocks, bonds, real estate, and cash.

- Equities (Stocks): Historically the highest growth engine, equities represent ownership in a company and offer the potential for capital gains and dividends.

- Fixed Income (Bonds): These act as a stabilizer, providing regular interest payments and preserving capital during equity market downturns.

- Real Estate: A tangible asset class that offers both rental income and appreciation, often serving as a strong hedge against inflation.

- Cash Equivalents: Essential for liquidity and taking advantage of market opportunities as they arise.

Risk Management and Diversification

The primary goal of a sophisticated investor is not just to maximize returns, but to maximize “risk-adjusted” returns. Diversification is the only “free lunch” in finance. By spreading investments across different sectors, geographies, and asset classes, an investor reduces the impact of any single asset’s poor performance on the total portfolio.

Understanding Market Volatility vs. Risk

A common misconception in financial literacy is equating volatility with risk. Volatility is the fluctuation in the price of an asset over a short period. Risk is the permanent loss of capital. Long-term wealth building requires the psychological fortitude to ignore short-term market “noise” and focus on the underlying value of the investment.

The Role of Tax Efficiency in Wealth Building

Wealth is not determined by what is earned, but by what is retained. Utilizing tax-advantaged accounts (such as 401(k)s, IRAs, or their international equivalents) and understanding capital gains tax structures are vital components of a professional financial strategy.

Conclusion: The Path Forward

Achieving financial independence is a marathon, not a sprint. It requires a commitment to continuous education, a disciplined approach to capital allocation, and a long-term perspective. By mastering these principles of financial literacy and investing, individuals can move beyond the limitations of a traditional savings account and enter the realm of true wealth building.