This article provides a comprehensive analysis of the fundamental financial principles derived from Robert Kiyosaki’s “Rich Dad Poor Dad,” specifically tailored for young professionals seeking long-term economic stability. It explores the critical distinction between assets and liabilities, emphasizing how a shift in mindset from prioritizing a steady salary to prioritizing continuous learning is the true catalyst for wealth. Readers will gain insights into why high income does not guarantee wealth without effective money management and how to transition from working for money to making money work for them through strategic investing. By focusing on skill acquisition in sales, investing, and financial literacy, the article outlines a professional roadmap for building a robust financial foundation. The objective is to provide actionable, objective strategies that empower individuals to navigate the complexities of modern personal finance and achieve sustainable growth through disciplined asset accumulation and early investment.

Introduction to Financial Literacy and the Wealth Gap

In the modern economic landscape, the difference between financial struggle and lasting wealth often boils down to one factor: financial literacy. While traditional education systems focus heavily on academic and professional skills, they frequently overlook the mechanics of money management. This gap is where the principles of “Rich Dad Poor Dad” become essential. These five lessons serve as a blueprint for anyone looking to break the cycle of living paycheck to paycheck and transition into a life of financial independence.

1. The Critical Distinction: Assets vs. Liabilities

The cornerstone of wealth building is understanding the technical definition of an asset versus a liability. In a professional financial context, the distinction is simple but profound:

- Assets: These are items or investments that put money into your pocket. Examples include rental properties, dividend-paying stocks, or intellectual property.

- Liabilities: These are items that take money out of your pocket. This often includes consumer debt, high-interest car loans, and even a primary residence if the maintenance and mortgage costs outweigh any immediate financial return.

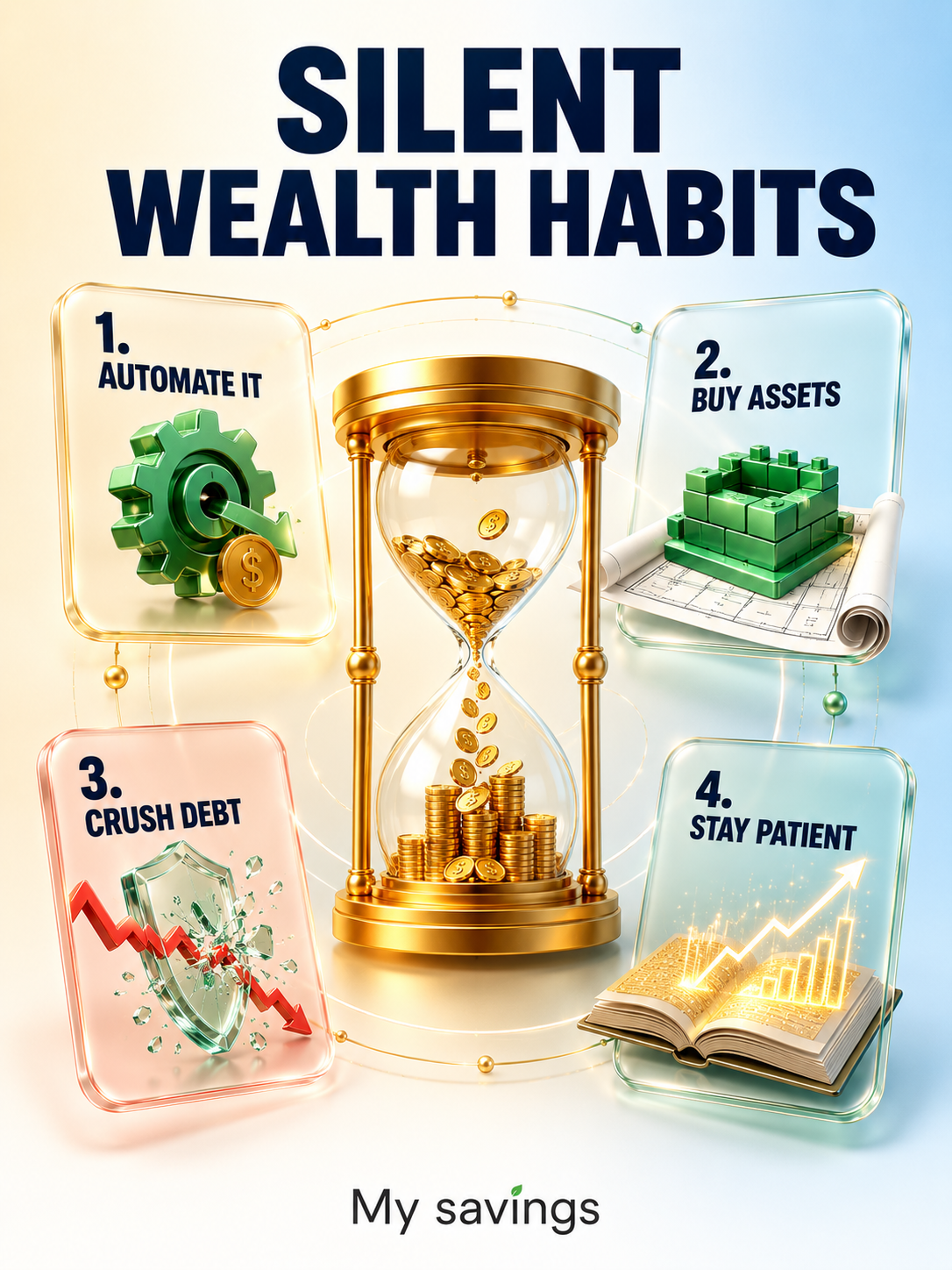

The wealthy focus on accumulating assets that generate cash flow. By prioritizing the purchase of income-generating vehicles over depreciating luxury goods, individuals create a self-sustaining cycle of wealth.

2. Mindset Over Salary: The Psychology of Wealth

A common misconception is that a high salary is the only path to riches. However, “Rich Dad Poor Dad” argues that mindset is far more influential. A “Poor Dad” mindset values job security and a steady paycheck above all else, often leading to a fear of risk. Conversely, a “Rich Dad” mindset values learning and financial education.

Your reality is shaped by how you perceive money. If you view money as a tool for growth rather than a finite resource to be hoarded or spent immediately, your financial trajectory changes. Cultivating a growth mindset involves staying curious about market trends, understanding tax advantages, and being willing to pivot when new opportunities arise.

3. Management: The Secret to Wealth Without High Income

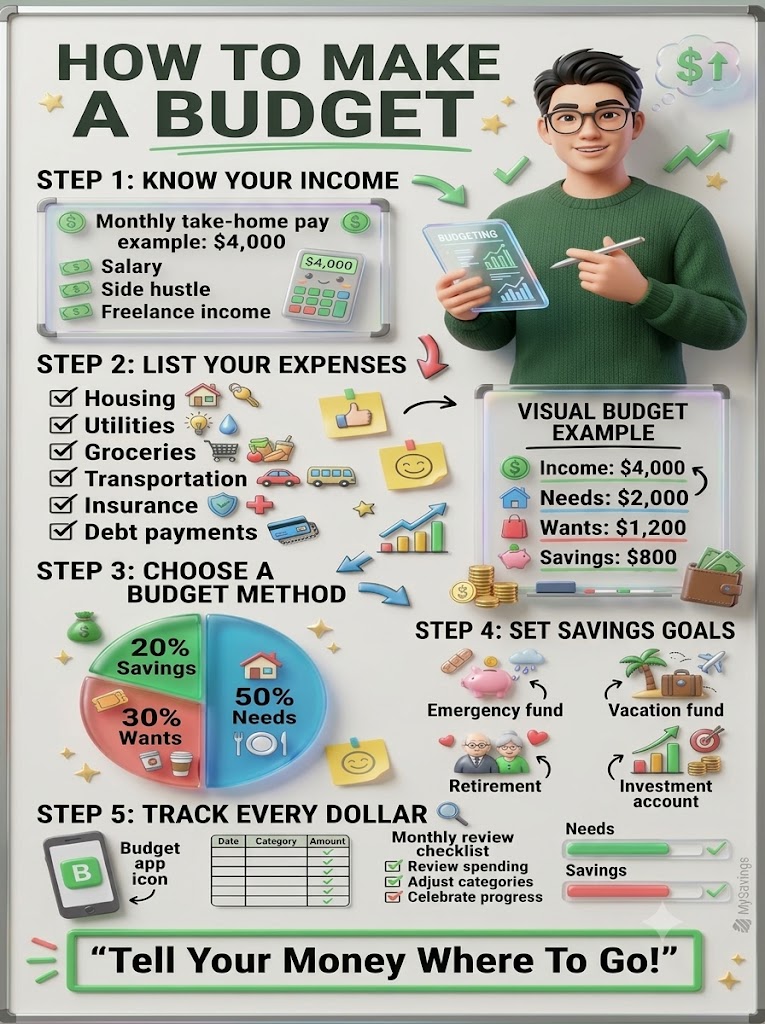

One does not need a six-figure income to start building a significant net worth. Wealth is not determined by how much you earn, but by how much you keep. Effective money management involves:

- Budgeting with Precision: Tracking every dollar to ensure it is allocated toward growth.

- Reducing “Lifestyle Creep”: Avoiding the urge to increase spending as income rises.

- Strategic Allocation: Prioritizing “paying yourself first” by moving a percentage of income into investments before paying bills.

By managing even a modest income better than the average consumer, an individual can outperform high-earners who lack fiscal discipline.

4. Professional Development: Work to Learn, Not to Earn

In the early stages of a career, the focus should shift from the immediate paycheck to the long-term value of the skills being acquired. Wealth-building requires a specific set of “power skills”:

- Sales and Marketing: The ability to communicate value and persuade others.

- Financial Literacy: The ability to read financial statements and understand the “language” of money.

- Investing Knowledge: Understanding how to evaluate risk and return.

By choosing roles that offer these learning opportunities, you build a “human capital” asset that will pay dividends for decades, far exceeding the value of an initial entry-level salary.

5. Leveraging Capital: Making Money Work for You

The final lesson is the transition from active income to passive income. Most people spend their lives trading their time for money. The wealthy, however, use their money to buy other people’s time or to fuel automated systems.

Investing early, even with small amounts, leverages the power of compound interest. When you invest, you are essentially hiring your dollars to go out and bring back more dollars. Whether through index funds, real estate, or business ventures, the goal is to reach a point where the income from your assets covers your living expenses, granting you true financial freedom.

Conclusion: The Path Forward

Building wealth is a marathon, not a sprint. By applying these five lessons prioritizing assets, refining your mindset, managing existing resources, focusing on skill acquisition, and investing early you set yourself on a path toward a secure and prosperous future. Financial independence is not an accident; it is the result of deliberate, informed choices made consistently over time.