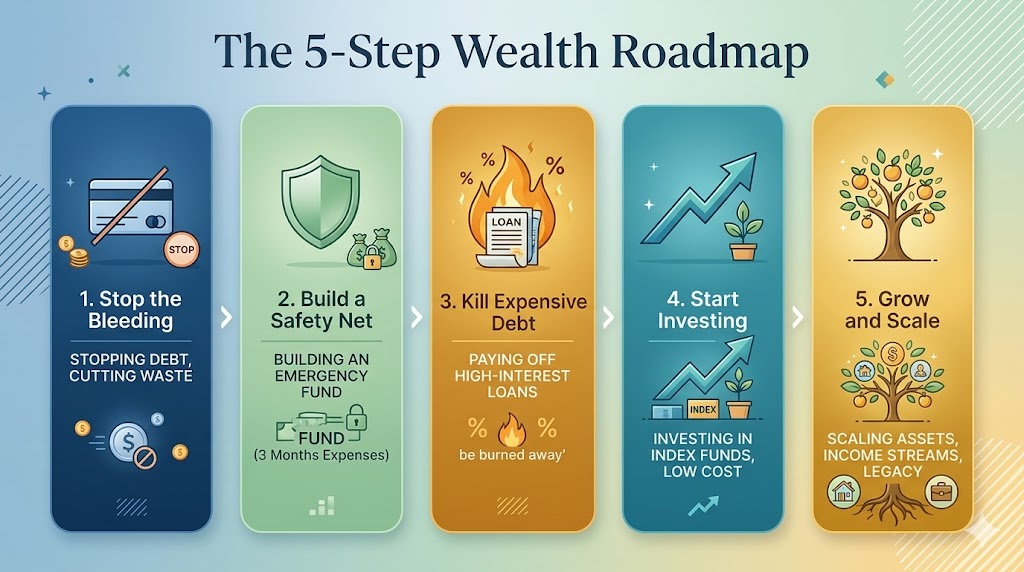

The Hierarchy of Wealth Creation: A Systematic Approach

In an era of economic volatility, the difference between financial stagnation and exponential growth often lies in the order of operations. Many attempt to “grow and scale” before they have “stopped the bleeding,” leading to a fragile financial structure that collapses under the slightest pressure. To build a lasting legacy, one must adhere to a rigorous, five-step strategic framework that prioritizes stability, debt elimination, and systematic investing.

Step 1: Stop the Bleeding – The Zero-Waste Mandate

The first and most critical stage of financial recovery is halting the accumulation of “bad debt.” Bad debt typically refers to high-interest consumer loans or credit card balances used for depreciating assets.

- Audit and Identify: Perform a comprehensive audit of all monthly outgoings to identify “waste”—subscriptions, interest fees, and non-essential expenditures that do not contribute to net worth.

- The Debt Ceiling: Establish a strict policy against taking on new high-interest liabilities. Without stopping the outflow of capital, even a high income cannot lead to wealth.

- Psychology of Scarcity: Transitioning from a spending mindset to a preservation mindset is the prerequisite for the steps that follow.

Step 2: Build a Safety Net – The Non-Negotiable Buffer

Once the leaks are plugged, the next priority is the “safety net.” This is not an investment; it is insurance against life’s unpredictability.

- The Three-Month Rule: The standard benchmark is three months of essential living expenses. This fund must be kept in a highly liquid, low-risk account.

- Non-Negotiable Status: This fund is “non-negotiable” because it prevents the need to incur new debt (Step 1) when emergencies arise, such as medical issues or sudden unemployment.

- Emotional Resilience: Beyond the math, a safety net provides the psychological stability required to make rational investment decisions in later stages without being driven by fear.

Step 3: Kill Expensive Debt – Prioritizing High-Interest Liabilities

With a safety net in place, all surplus capital should be aggressively directed toward “killing” expensive debt.

- High-Interest First: Mathematically, paying off a 20% interest credit card is equivalent to a guaranteed 20% return on investment. No traditional market investment can reliably beat this.

- The Velocity of Capital: By eliminating interest payments, more capital is freed up for Step 4. Debt is a drag on wealth velocity; removing it accelerates the path to growth.

- Strategic Sequencing: Only after high-interest liabilities are cleared should an individual consider large-scale market participation.

Step 4: Start Investing – The Power of Indexing and Time

The transition from defense to offense begins here. The goal is no longer just saving, but putting capital to work in the global economy.

- Low-Cost Index Funds: For the vast majority of people, low-cost index funds provide the best risk-adjusted returns. They offer instant diversification and lower fees than actively managed funds.

- Long-Term Horizon: Wealth at this stage is built through the power of compounding. The focus is on “time in the market” rather than “timing the market.”

- Systematic Contributions: Consistency is the engine of this step. Automated monthly contributions ensure that the portfolio grows regardless of market fluctuations.

Step 5: Grow and Scale – Assets, Income Streams, and Legacy

The final stage is where true financial freedom is realized. Having built a solid foundation, the focus shifts to expanding the reach of your capital.

- Diversified Income Streams: This may include real estate, private equity, or business ventures that provide passive cash flow.

- Asset Allocation: Shifting from pure growth to a mix of growth and preservation to ensure the portfolio survives different economic cycles.

- Legacy Planning: The “Scale” phase is about more than personal consumption; it is about building structures (trusts, foundations, or generational businesses) that extend wealth beyond a single lifetime.

Financial success is a sequence, not a sprint. By stopping the bleeding, building a safety net, killing debt, investing in the long term, and eventually scaling assets, any individual can move from financial fragility to a position of permanent strength.