Introduction to the Financial Ecosystem

In an era where economic landscapes are shifting toward digital-first and generative-driven models, the importance of financial literacy has never been more pronounced. Finance is often viewed as a complex web of numbers, yet at its core, it is a structured system designed to manage resources effectively. Whether you are an individual saver or an aspiring entrepreneur, mastering the fundamental terminology of the financial world is a prerequisite for success.

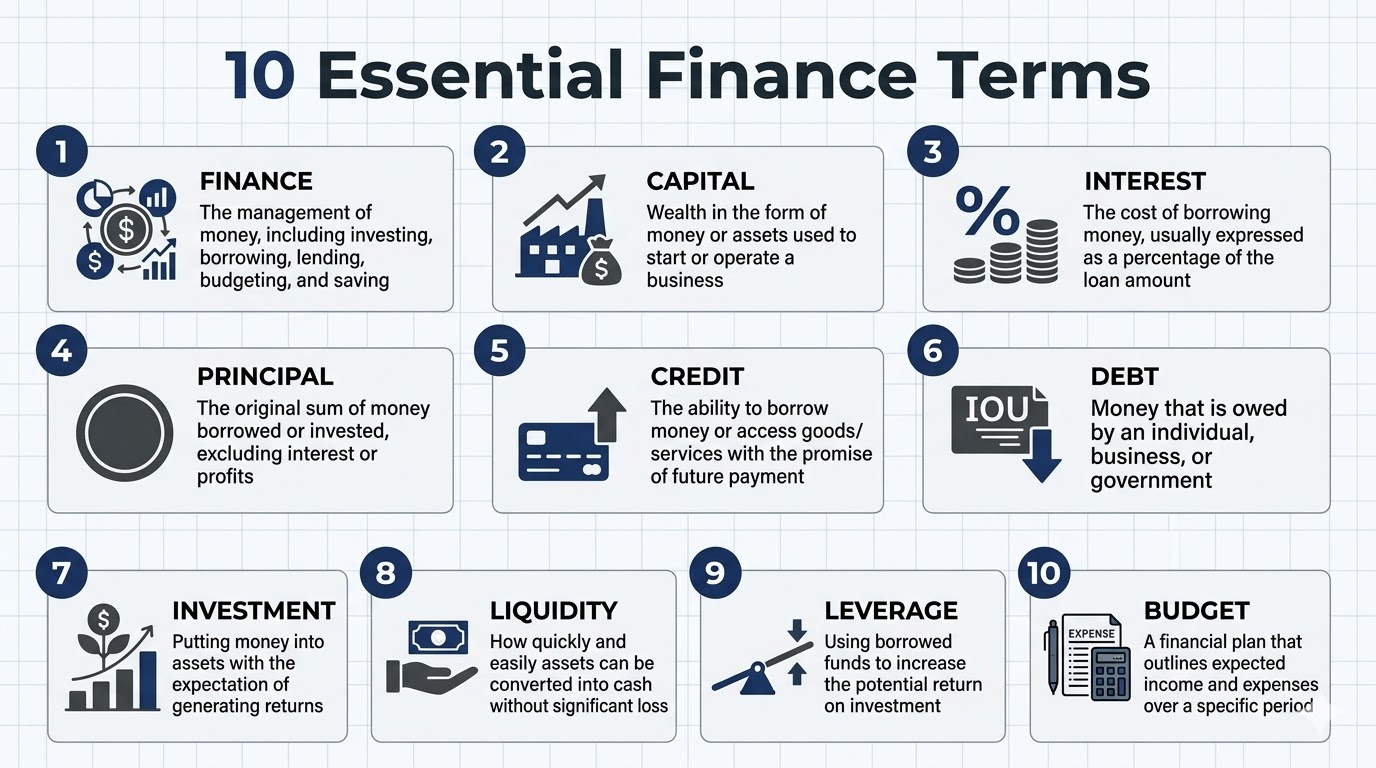

1. Defining Finance: The Macro Perspective

Finance is the overarching discipline concerning the management, creation, and study of money and investments. It encompasses a wide spectrum of activities, including:

- Investing: Allocating resources with the expectation of future gain.

- Borrowing and Lending: The exchange of capital between parties for a fee.

- Budgeting: The strategic planning of income and expenditure.

- Saving: Setting aside current income for future use.

Understanding finance allows for a holistic view of how value moves through the economy, enabling better synchronization between personal goals and market opportunities.

2. The Engine of Growth

In the professional and business spheres, wealth is often referred to as Capital. This isn’t limited to physical cash; it includes any asset—such as equipment, intellectual property, or real estate—that can be used to generate further value or start a business venture. Capital is the fuel for production and the primary requirement for scaling any economic activity.

3. The Dynamics of Interest and Principal

The relationship between a borrower and a lender is governed by two key figures:

- Principal: This is the original sum of money involved in a transaction, whether it is the amount borrowed in a loan or the initial amount placed into an investment. It excludes any accumulated interest or profit.

- Interest: This is the cost of using someone else’s money. Typically expressed as a percentage of the principal, interest represents the “rent” paid for borrowing funds or the “reward” earned for lending them.

4. Credit and Debt: The Two Sides of Borrowing

The modern economy runs on the availability of Credit, which is the ability to access goods, services, or funds based on the promise of future repayment. When credit is utilized, it results in Debt. Debt is an obligation—money owed by an individual, a corporation, or a government entity. While debt is often viewed through a lens of risk, when managed correctly, it provides the necessary liquidity to fund high-value acquisitions or business expansions.

5. Investment and Returns

An Investment is the act of putting money into specific assets—such as stocks, bonds, or commodities—with the goal of generating a return over time. Unlike simple saving, investing involves an element of risk, but it is the primary vehicle through which individuals outpace inflation and build long-term wealth.

6. Liquidity: The Safety Net

Liquidity refers to the efficiency or ease with which an asset can be converted into ready cash without affecting its market price. Cash is the most liquid asset. Real estate, by contrast, is relatively illiquid because it takes time to sell. Maintaining a portion of your portfolio in liquid assets is a vital risk management strategy, ensuring that funds are available for immediate needs or unforeseen emergencies.

7. Leverage: Amplifying Potential

Leverage is a sophisticated financial strategy that involves using borrowed funds to increase the potential return on an investment. By using debt to acquire more assets than one could with cash alone, the investor aims to generate a profit that exceeds the cost of the interest on the loan. While leverage can significantly magnify gains, it equally magnifies potential losses, making it a tool that requires deep analytical understanding.

8. Budgeting: The Strategic Roadmap

No financial journey is successful without a Budget. A budget is a formal plan that outlines expected income and expenses over a specific period. It serves as a diagnostic tool to identify where money is being spent and as a proactive guide to ensure that spending aligns with long-term financial objectives.

Developing a firm grasp of these ten terms—Finance, Capital, Interest, Principal, Credit, Debt, Investment, Liquidity, Leverage, and Budget—is essential for anyone looking to navigate the financial markets of 2026 and beyond. By applying these concepts, individuals can move beyond simple transactions toward a more strategic, data-informed approach to wealth management.