When it comes to building wealth, most people focus on the wrong variable. 📉 We obsess over the “big hit,” the perfect stock pick, or finding a way to suddenly double our income so we can finally start saving. We tell ourselves, “I’ll start investing when I have more money.” 💸

However, the math of wealth creation tells a different story. In the world of finance, time is a much more powerful lever than capital. ⏳ Starting early even with a small amount matters significantly more than how much you invest later in life.

If you are waiting for the “right time” to start, you are likely losing more money in potential growth than you could ever make up for with a higher salary later. Here is why the early bird doesn’t just get the worm they get the whole garden. 🌳✨

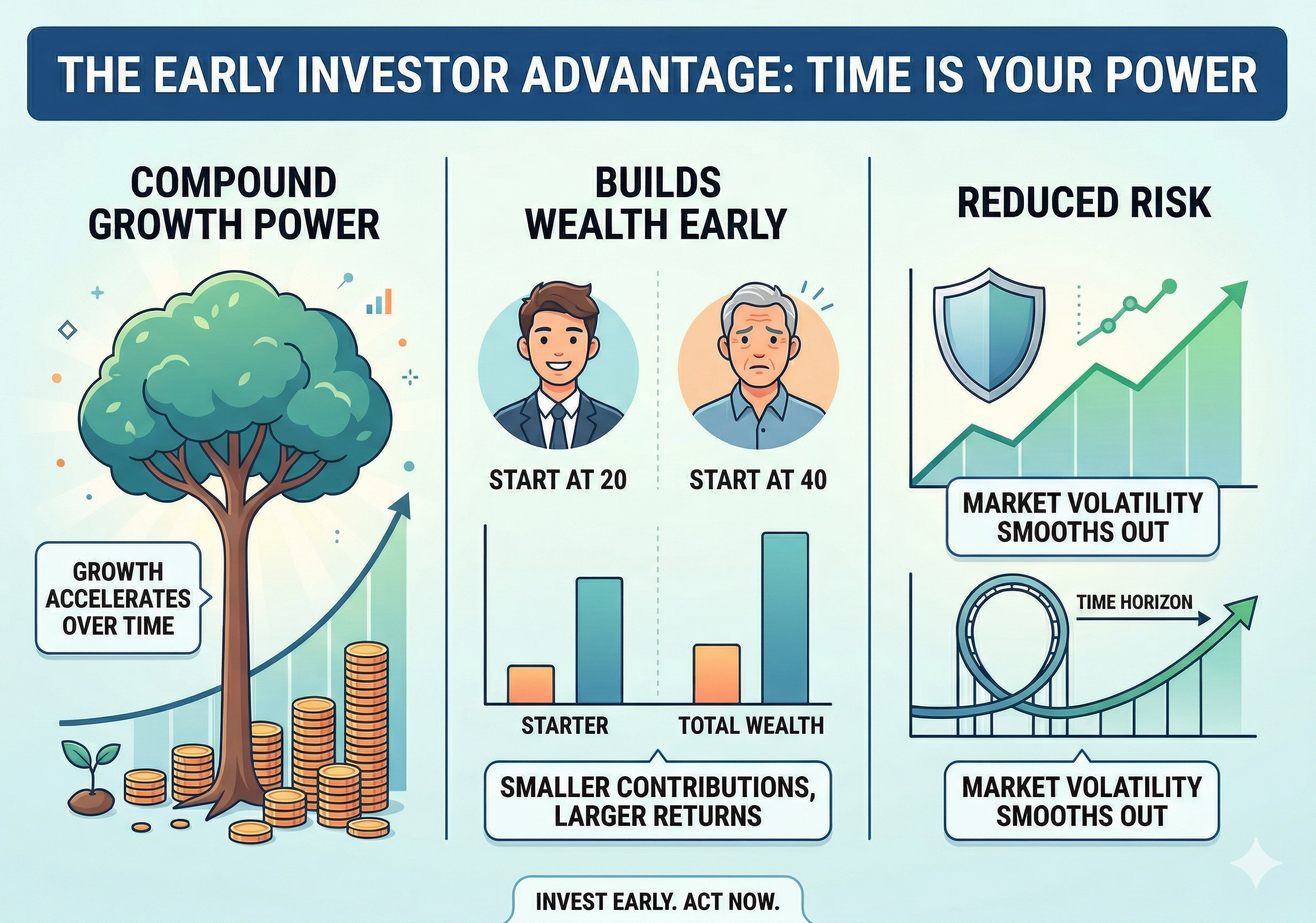

1. The Magic of Compounding (The “Snowball” Effect) ❄️

Albert Einstein famously called compound interest the “eighth wonder of the world.” 🌍 The concept is simple: you earn interest on your initial investment, and then you earn interest on that interest.

Imagine two friends, Alex and Sarah:

- Alex 🙋♂️ starts at age 25, investing $200 a month for 10 years and then stops entirely at age 35.

- Sarah 🙋♀️ waits until she is 35 to start. She realizes she’s behind, so she invests $200 a month for the next 30 years until she retires at 65.

Even though Sarah invested three times as much money for three times as long, Alex will likely end up with more money at retirement. Why? 🧠 Because Alex’s money had an extra decade to “cook.” The exponential curve of compounding happens at the end of the timeline, and you can only reach that curve if you give your money enough time to grow. 📈

2. The Cost of Waiting 🛑

Many young professionals fall into the “compensation trap.” They believe that because they will earn more in their 30s and 40s, they can simply “catch up” then.

The math, unfortunately, is unforgiving. 🧮 To match the retirement fund of someone who started at 20 with just $100 a month, someone starting at 40 might need to invest $1,000 or even $1,500 a month. By waiting, you are essentially “taxing” your future self. 💸 You are forcing your older self to work much harder and save a much larger percentage of their income just to reach the same goal that your younger self could have reached with the price of a few lattes. ☕️

3. Time Reduces Risk 🛡️

The stock market is a roller coaster in the short term but a steady climb in the long term. 🎢 When you start investing early, time is your insurance policy.

If the market crashes when you are 22, it doesn’t matter; you have 40 years for it to recover. You can afford to invest in “aggressive” assets like stocks and ETFs that offer higher returns because you aren’t touching that money for decades. 💎 A late starter, however, often feels pressured to take massive risks to “make up for lost time,” which frequently leads to devastating losses right when they need the money most. ⚠️

4. It’s About Habits, Not Just Math 🏗️

Starting early isn’t just about the balance in your brokerage account; it’s about the investor mindset. 🧠

When you start investing with $50 or $100 a month, you are training your brain to live on less than you earn. You are learning how to navigate market volatility when the stakes are low. 🎢 If you lose 10% of $1,000, it’s a $100 lesson. If you wait until you have $100,000 to “start learning,” that same 10% dip is a $10,000 lesson. 🎓

By starting early, you build the discipline of Automated Investing . 🤖 You treat your future self as a “bill” that must be paid first every month. By the time your income grows, the habit is so deeply ingrained that you naturally scale your investments without feeling the “pinch.” 🤏

5. How to Start Today (Even with $10) 💵

You don’t need a financial advisor or a massive windfall to get started. The barrier to entry has never been lower. 👇

- Micro-Investing Apps: 📱 Use platforms that allow you to invest spare change or small increments.

- Index Funds & ETFs: 🧺 Instead of trying to find the next Apple or Tesla, buy the whole market. An S&P 500 index fund gives you a piece of the 500 largest companies.

- The 1% Rule: 📏 If you can’t afford to save 10% of your income, start with 1%. Next month, move it to 2%. You won’t notice the difference in your lifestyle, but your 65-year-old self certainly will. 👴👵

Final Thoughts 💭

The most expensive thing you can own is a “closed mind” and a “waited time.” 🚫 The simple truth remains: activity—the constant checking of stocks, the trading, the searching for “the one” matters far less than the simple act of beginning. 🏁

Stop waiting for the perfect salary, the perfect market conditions, or the perfect amount of knowledge. In the race to wealth, the person who starts walking today will always beat the person who plans to sprint tomorrow. 🏃♂️💨

Your future is on sale today. Don’t miss the discount. 🏷️✨