This comprehensive guide breaks down the essential journey of wealth management into three distinct phases: Beginner, Intermediate, and Professional. Most individuals fail in their investment journey because they attempt to skip steps, such as trading before establishing an emergency fund. This article details how to build a rock-solid financial foundation by eliminating high-interest debt and mastering basic budgeting. It then explores capital growth strategies like index investing and dollar-cost averaging to make your money work for you. Finally, it delves into professional-level asset protection and strategic allocation. By following this structured hierarchy, savers can move from financial friction to long-term longevity. Whether you are just starting your savings journey or looking to protect established wealth, understanding these phases is critical for achieving sustainable financial independence and mastering the art of capital distribution.

Introduction: The Hierarchy of Wealth

In the modern economy, the question is rarely if you should invest, but rather when and how. Many aspiring investors rush into high-risk markets without a safety net, leading to preventable losses. To achieve true financial independence, one must master their current phase before moving forward. Success in finance is not about timing the market; it is about the structural integrity of your financial plan.

Section 1: The Beginner Phase – Building Your Financial Foundation

The goal of the beginner phase is stability before growth. This is the stage where you build control over your capital to ensure that future investments are not derailed by life’s unexpected turns.

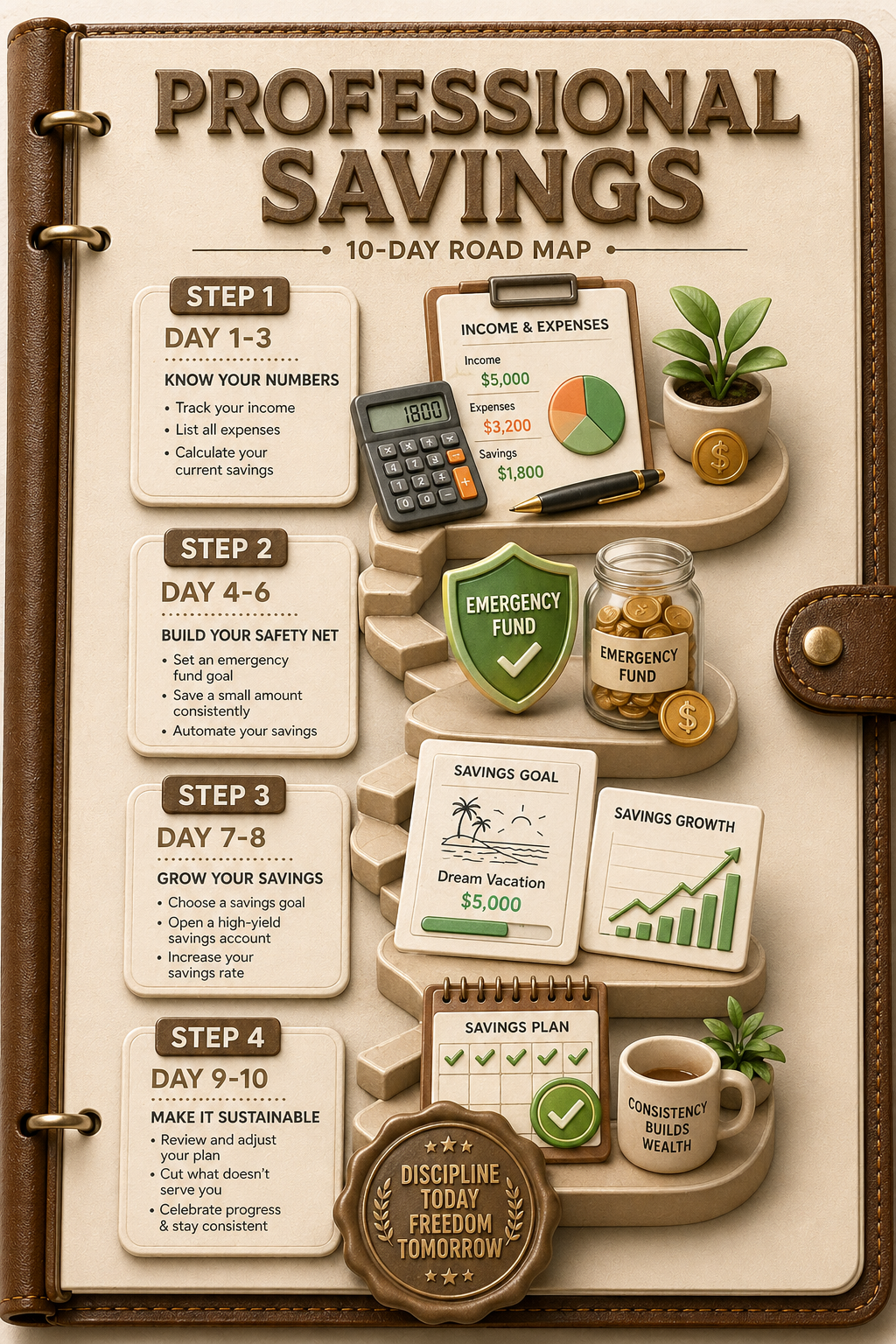

1. The Emergency Fund An emergency fund is a cash buffer intended solely for unexpected expenses. The objective is to accumulate three to six months of essential living expenses. This liquidity ensures that if a job loss or medical emergency occurs, you aren’t forced to liquidate investments at a loss.

2. Eliminating High-Interest Debt High-interest debt, such as credit card balances and personal loans, acts as “financial friction.” The interest rates on these debts often exceed the average returns of the stock market. Therefore, paying down a 20% APR credit card is equivalent to a guaranteed 20% return on investment.

3. Basic Budgeting & Tracking You cannot manage what you do not measure. Basic budgeting involves tracking every dollar to understand where money goes. By increasing your savings rate through disciplined tracking, you create the “seed capital” necessary for the next phase.

4. Financial Education Before risking capital, one must invest in knowledge. Understanding the difference between assets (things that put money in your pocket) and liabilities (things that take money out) is the cornerstone of financial literacy.

Section 2: The Intermediate Phase – Capital Growth

Once the foundation is secure, the focus shifts to capital growth. In this phase, your money starts working for you, and the goal is to build consistency.

1. Index Investing Index investing provides broad market exposure, allowing investors to capture the growth of the entire economy rather than betting on individual stocks. This strategy focuses on protecting and growing capital with lower volatility.

2. Dollar-Cost Averaging (DCA) Consistency is the engine of wealth. Dollar-cost averaging involves investing a fixed amount of money at regular intervals, regardless of market price. This removes emotional decision-making and lowers the average cost per share over time.

3. Retirement Accounts Utilizing tax-advantaged accounts (such as 401ks or IRAs) allows for compounding growth without the immediate drag of taxation. Contributing every single month to these accounts is a non-negotiable step for long-term security.

4. Skill-Based Income Growth Investing is not just about the stock market; it is about increasing your earning power. Career leverage, certifications, and negotiation skills increase the amount of capital you have available to invest, accelerating the journey to the professional phase.

Section 3: The Professional Phase – Advanced Allocation & Retention

In the professional phase, growth becomes strategic. The focus shifts from merely accumulating wealth to building longevity and protecting what has been earned.

1. Strategic Asset Allocation This involves the deliberate distribution of capital across various asset classes, including stocks, real estate, private business, and alternatives. The goal is to optimize the risk-to-reward ratio based on specific long-term objectives.

2. Active Trading (With Education) For those with the requisite education, active trading can be used to generate alpha. However, this is structured, rule-based execution. Professionals manage risk on every single trade to ensure that no single loss can compromise their overall portfolio.

3. Asset Protection As wealth grows, so does the need to protect it from downside risk. This involves diversification, comprehensive insurance, and legal structures (like trusts or LLCs) to shield assets from liability and economic downturns.

4. Advanced Budgeting & Planning At the professional level, budgeting evolves into advanced cash flow management. It is no longer just about “saving” but about planning spending in advance to ensure maximum capital efficiency. The objective is to keep more of what you earn through tax efficiency and strategic planning.

Mastering the Phases

Financial success is a marathon, not a sprint. By mastering the beginner phase of stability, the intermediate phase of growth, and the professional phase of retention, investors can build a legacy of wealth. The key is to never move to the next step until the current one is firmly established.