💸 Most financial struggles are not caused by low income alone — they often come from poor structure, emotional spending, and weak money habits. Building long-term wealth requires discipline, smart planning, and the ability to make intentional financial decisions every day.

📈 This article explores six powerful money principles that can transform personal finances over time. From avoiding unnecessary purchases and limiting peer-pressure spending to understanding the importance of emergency funds, multiple income streams, and tax awareness, these lessons reveal what truly separates financially stable people from those constantly struggling with money.

💡 Readers will also discover why the people around them strongly influence financial behavior and how creating better systems can improve saving consistency and long-term security. Whether the goal is financial freedom, smarter budgeting, or wealth-building, these practical strategies provide a strong foundation for better money management in today’s economy.

Money Truths Most People Learn Too Late

Money problems are often misunderstood. Many people believe financial success comes only from earning a high salary, landing a better job, or getting lucky with investments. In reality, long-term financial stability usually depends on structure, habits, discipline, and decision-making.

Wealth is rarely built through one dramatic action. Instead, it grows through consistent financial behaviors repeated over time. Small daily decisions — spending, saving, investing, and managing risk — eventually shape financial outcomes.

These six money truths reveal some of the most important financial lessons for building stability, protecting wealth, and improving long-term financial health.

💡 Most People Do Not Have Money Problems — They Have Structure Problems

Many financial struggles are not caused by a lack of income. They are caused by the absence of a financial system.

Without structure, even high earners can struggle financially. A person may earn a strong monthly income yet still experience stress, debt, and financial instability because spending habits are uncontrolled and savings are inconsistent.

Financial structure creates clarity. It helps people understand:

- Where money is going

- How much should be saved

- Which expenses are unnecessary

- How to prepare for emergencies

- How to build wealth gradually

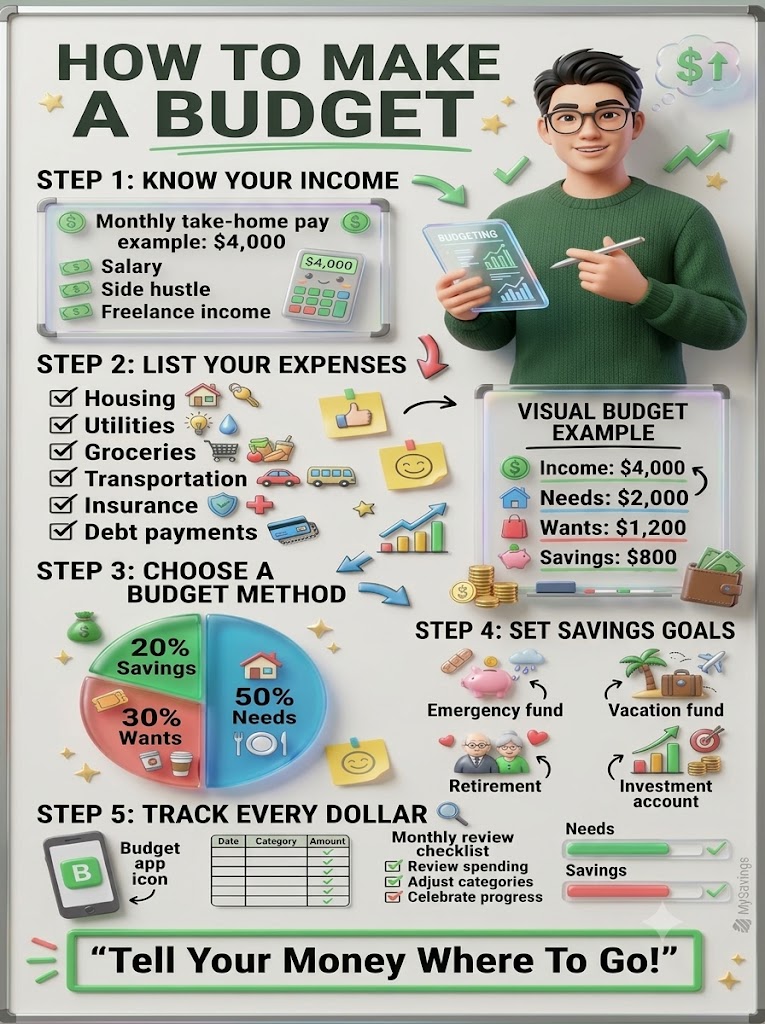

📊 Why Financial Systems Matter

A strong money system removes emotional decision-making from personal finances. Instead of reacting impulsively, structured budgeting creates intentional spending patterns.

Important elements of a healthy financial structure include:

💵 Monthly Budget Planning

Tracking income and expenses helps identify financial leaks and overspending habits.

🏦 Automatic Savings

Automating savings ensures consistent financial growth without relying on motivation.

📅 Expense Categories

Organizing spending into categories improves awareness and control.

🎯 Financial Goals

Clear goals increase discipline and long-term focus.

People who create systems around money often experience lower stress levels and better financial outcomes over time.

🚫 Wealth Requires Saying “No” More Than “Yes”

One of the biggest differences between wealthy people and constant spenders is the ability to delay gratification.

Modern consumer culture encourages endless spending. Social media trends, online shopping, luxury branding, and peer influence constantly push unnecessary purchases.

Building wealth often requires rejecting short-term pleasure in favor of long-term financial security.

🛑 The Hidden Cost of Impulse Spending

Small unnecessary purchases may seem harmless individually, but repeated impulsive spending can destroy savings potential.

Examples include:

- Trend-based purchases

- Unnecessary subscriptions

- Frequent luxury spending

- Emotional shopping

- Lifestyle inflation

Financial discipline is not about avoiding enjoyment entirely. It is about spending intentionally instead of emotionally.

💰 Every “No” Becomes a Future Investment

Every avoided unnecessary expense creates an opportunity for:

- Emergency savings

- Debt reduction

- Investment growth

- Retirement preparation

- Financial independence

Wealth often grows quietly through consistent restraint rather than visible luxury.

👥 The People Around You Influence Your Finances More Than You Think

Financial habits are highly contagious.

People naturally adopt behaviors, priorities, and lifestyles from their environment. Spending habits are often shaped by friends, family members, coworkers, and social circles.

Someone surrounded by impulsive spenders may begin overspending without realizing it. On the other hand, people surrounded by disciplined savers and ambitious builders often develop stronger financial habits.

🧠 Financial Behavior Is Social

Human behavior is deeply influenced by social normalization. When expensive lifestyles become common in a social circle, overspending begins to feel normal.

Common financial influences include:

🛍️ Peer Pressure Spending

Trying to match others financially can create unnecessary debt and stress.

📱 Social Media Comparison

Constant exposure to luxury lifestyles encourages unrealistic expectations.

🏗️ Growth-Oriented Environments

Being around financially disciplined people can improve motivation and financial awareness.

🌱 Choose Financially Healthy Environments

Healthy financial environments encourage:

- Saving consistency

- Long-term thinking

- Investment education

- Business and career growth

- Responsible spending

Financial success is often connected to the habits and mindset of the people nearby.

💼 One Income Stream Is One Point of Failure

Relying entirely on a single income source creates financial vulnerability.

Economic downturns, layoffs, industry changes, inflation, and emergencies can suddenly reduce income stability. Depending on only one paycheck increases financial risk.

Diversifying income improves financial security and resilience.

📈 Why Multiple Income Streams Matter

Additional income sources can:

- Increase savings speed

- Reduce financial stress

- Provide backup during emergencies

- Accelerate debt repayment

- Improve investment opportunities

Modern technology and digital platforms have created many ways to build extra income.

💡 Popular Additional Income Ideas

🌐 Freelancing

Skills like writing, graphic design, coding, and marketing can generate online income.

🛒 Digital Businesses

Blogs, online stores, and digital products create scalable opportunities.

📊 Investments

Dividend stocks, mutual funds, and long-term investing can produce passive income.

🎥 Content Creation

Educational or entertainment content can become monetized over time.

A second income stream does not need to replace a full-time job immediately. Even small additional income sources can improve long-term financial flexibility.

🛡️ A Safety Fund Is Emotional Protection, Not Just Financial Protection

Emergency savings do more than cover unexpected expenses. They reduce fear, anxiety, and financial pressure.

People without emergency savings often feel trapped during crises because every problem becomes financially dangerous.

A safety fund creates breathing room and decision-making freedom.

🚨 Why Emergency Funds Matter

Unexpected expenses can appear at any time:

- Medical emergencies

- Vehicle repairs

- Job loss

- Family emergencies

- Economic instability

Without savings, people may rely on debt, loans, or high-interest credit options.

💰 How Much Should Be Saved?

Many financial experts recommend building emergency savings equal to:

- 3 to 6 months of living expenses

- More for unstable income situations

- Additional reserves for families or businesses

🧠 Emotional Benefits of Emergency Savings

Financial safety funds can reduce:

- Stress

- Panic decision-making

- Dependence on debt

- Fear of uncertainty

Savings are not just money. They are flexibility, security, and freedom.

🧾 Understanding Taxes Is One of the Most Financially Powerful Skills You Can Learn

Many people spend years earning money without learning how taxes work.

Tax knowledge can significantly affect:

- Savings potential

- Investment growth

- Business profitability

- Financial planning

- Wealth preservation

Understanding legal tax advantages helps people make smarter financial decisions.

📊 Why Tax Education Matters

Tax systems affect nearly every area of personal finance, including:

- Salaries

- Investments

- Businesses

- Property ownership

- Retirement planning

Learning basic tax principles can help reduce unnecessary financial losses.

✅ Smart Financial Tax Habits

📂 Keep Financial Records Organized

Accurate tracking improves budgeting and financial awareness.

📈 Learn Investment Tax Rules

Different investment types may have different tax treatments.

🏢 Understand Business Expenses

Business-related deductions can reduce taxable income legally.

📚 Continue Financial Education

Tax laws and financial systems evolve regularly.

Tax awareness is not only for business owners or accountants. It is an essential life skill for long-term financial growth.

🚀 Final Thoughts

Financial success is usually less about luck and more about systems, discipline, and long-term behavior.

These six money truths highlight an important reality:

- Better structure creates better financial control

- Saying “no” protects future wealth

- Financial environments influence behavior

- Multiple income streams reduce risk

- Emergency savings create freedom

- Tax knowledge strengthens financial power

Building wealth rarely happens overnight. It is often the result of consistent habits repeated for years.

Small financial improvements made today can create major long-term changes tomorrow.