📈 Managing personal finances effectively requires a structured approach to tracking income and managing expenditures. 📊 This comprehensive guide breaks down the essential steps of creating a sustainable budget, from identifying net income sources like salaries and freelance earnings to categorizing fixed and variable expenses. 🏦 Readers will explore proven budgeting frameworks, such as the widely acclaimed 50/30/20 rule, which systematically allocates resources toward necessary living costs, personal desires, and long-term financial milestones. 💸 Additionally, the article highlights the importance of establishing dedicated savings targets for emergencies, retirement, and investments while tracking every dollar to ensure long-term alignment with personal wealth goals. 💎 By implementing these structured financial strategies, individuals can eliminate wasteful spending habits, optimize their cash flow, and build a secure financial foundation. 🎯 Read on to discover actionable budgeting methods designed to transform your financial habits and secure your future. ✨

🔍 How to Create a Personal Budget Successfully?

Effective financial management serves as the cornerstone of long-term economic stability and wealth accumulation. Without a structured framework to regulate cash flow, individuals frequently find themselves navigating financial uncertainty, regardless of their income level. Budgeting is not an exercise in financial restriction; rather, it is a strategic roadmap that empowers individuals to assign purpose to every dollar earned. By establishing a clear overview of financial inputs and outputs, you can mitigate economic anxiety, eliminate unnecessary debt, and systematically fund long-term objectives.

This comprehensive guide provides an objective, step-by-step breakdown of how to design, execute, and maintain an efficient personal budget tailored to modern financial demands.

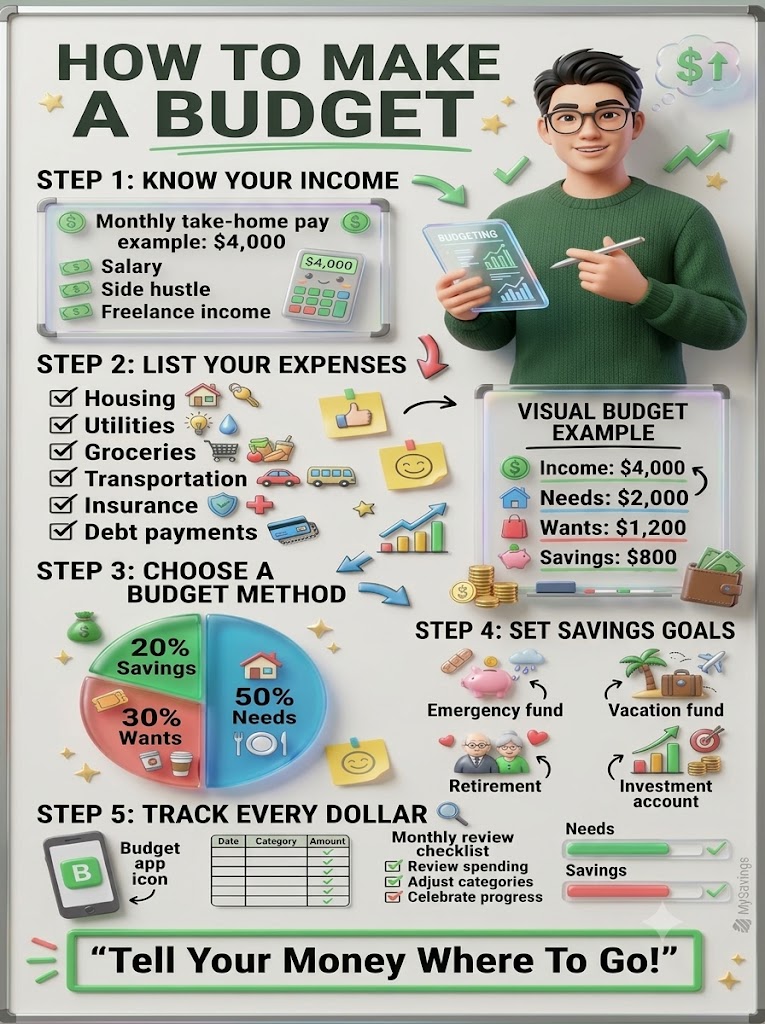

💵 Step 1: Establish a Comprehensive Overview of Total Income

The foundation of any functional budget rests upon an accurate calculation of total net income. Relying on gross income figures can lead to structural deficits, as taxes, insurance deductions, and retirement contributions significantly alter the actual liquidity available for monthly expenditures.

To establish an accurate baseline, all regular and irregular revenue streams must be aggregated monthly:

🟢 Base Salary: This constitutes the primary source of predictable cash inflow for salaried employees, representing the net take-home pay deposited directly into a banking account after all legal and corporate deductions.

🔵 Side Hustle Earnings: Income generated from secondary commercial ventures, e-commerce activities, or contractual consulting arrangements must be factored in using a conservative monthly average to account for potential market fluctuations.

🟣 Freelance and Contractual Income: Independent contractors and gig economy professionals must track irregular payments meticulously, utilizing historic data to estimate a safe, baseline monthly minimum for budgeting purposes.

Once the total net income is calculated—for example, a baseline of $4,000 per month individuals possess the necessary foundation to execute the subsequent phases of financial planning.

📉 Step 2: Conduct a Detailed Categorization of Monthly Expenses

An accurate understanding of cash outflow is crucial to identifying systemic inefficiencies in personal spending. Expenses are generally divided into fixed requirements and variable expenditures, both of which must be thoroughly documented to prevent capital leakage.

Tracking historical spending through bank statements and credit card ledgers reveals the precise distribution of capital across critical sectors:

🟤 Housing: Monthly mortgage payments, rental fees, property taxes, and mandatory community association dues form the largest fixed structural cost for most households.

🟡 Utilities: Essential operational costs, including electricity, water, gas, high-speed internet, and cellular communication services, require consistent allocation.

🟠 Groceries: Nutritional sustenance represents a variable yet non-negotiable expense category that must be monitored to distinguish essential sustenance from premium dining upgrades.

🔴 Transportation: Commuting expenses encompassing automotive loan payments, fuel, public transit passes, vehicle maintenance, and parking fees must be factored into the operational budget.

🟪 Insurance Coverages: Premium payments dedicated to maintaining health, life, auto, and property insurance policies protect against catastrophic financial losses.

🔲 Debt Service Obligation: Minimum monthly obligations toward student loans, outstanding credit card balances, personal loans, and retail financing agreements require strict prioritization to safeguard credit health.

📐 Step 3: Select and Implement a Proven Budgeting Framework

A structured allocation methodology prevents emotional spending and provides clear, mathematical boundaries for resource distribution. One of the most resilient and universally applicable frameworks is the 50/30/20 budgeting rule, which categorizes expenditures into three distinct operational pools.

This systemic division ensures that essential obligations are met while simultaneously securing future financial health and maintaining a reasonable quality of life:

🧩 50% Dedicated to Essential Needs: Exactly half of the net income is reserved exclusively for non-negotiable living expenses, such as housing, healthcare, basic utilities, transportation, and core groceries.

🎨 30% Allocated for Discretionary Wants: This portion accommodates lifestyle choices that enhance personal well-being but are non-essential for survival, including dining out, entertainment, subscription services, and recreational travel.

🏆 20% Conserved for Financial Goals: The remaining fifth of total revenue is directed intentionally toward capital accumulation, debt acceleration programs, and long-term asset investments.

For an individual earning a net income of $4,000 per month, this structural breakdown translates precisely into $2,000 for essential needs, $1,200 for discretionary lifestyle choices, and $800 allocated directly toward long-term financial security.

🎯 Step 4: Define and Fund Distinct Strategic Savings Goals

Capital accumulation without a defined purpose frequently results in low retention rates. To maximize the efficiency of the 20% savings allocation, capital should be systematically partitioned into specialized accounts designed to counter specific risks or capture future opportunities.

Prioritizing savings distributions ensures long-term fiscal resilience against market volatility:

💎 Emergency Fund Establishments: Financial planners universally recommend maintaining an accessible liquidity reserve equivalent to three to six months of core living expenses to mitigate unexpected medical emergencies or sudden employment termination.

✈️ Sinking Funds for Lifestyle Milestones: Dedicated capital reserves should be incrementally funded to cover anticipated, non-recurring expenses such as annual vacations, vehicle replacements, or holiday distributions without disrupting the primary budget.

⚓ Long-Term Retirement Capital: Consistent contributions to employer-sponsored retirement plans, individual retirement accounts, or sovereign pension funds leverage the compounding effects of time to build future wealth.

📈 Strategic Investment Portfolios: Capital directed toward equities, fixed-income instruments, real estate index funds, or diversified exchange-traded funds (ETFs) serves to counteract monetary inflation and expand net worth over time.

🔍 Step 5: Leverage Technology to Track and Review Every Dollar

A budget is a dynamic instrument that requires constant verification against real-world execution. Failing to track daily expenditures compromises the integrity of the financial plan, leading to accidental deficits.

Modern financial tools and periodic reviews provide the necessary visibility to maintain operational compliance:

📱 Automated Budgeting Applications: Utilizing digital software platforms enables real-time synchronization with banking institutions, automating the categorization of transactions and generating instantaneous visual alerts when category limits are approached.

📊 Manual Ledger Maintenance: For individuals seeking tactile awareness of their financial habits, utilizing specialized spreadsheets or physical accounting ledgers provides an intimate, deliberate tracking experience.

🔋 Monthly Review Checklists: At the conclusion of each billing cycle, an objective comparison between projected spending and actual expenditures must be executed to identify anomalies, adjust underfunded categories, and record financial progress.

By actively directing resources rather than passively observing spending patterns, individuals transition from financial reactivity to proactive wealth management. Consistent execution of these steps transforms abstract financial goals into structured, inevitable milestones.