Starting your first full-time job in 2026 is exciting and financially important. Between rising living costs, subscription-heavy lifestyles, new investing tools, and evolving job benefits, the money decisions you make in your first year can set you up for years (or decades) of stability.

This guide covers practical, modern personal finance advice for young professionals beginning their careers in 2026 step by step, with clear priorities you can act on immediately.

Table of Contents

1. [Why 2026 Is a Unique Time to Start Managing Money](why-2026-is-a-unique-time-to-start-managing-money)

2. [The First Month: Set Up Your Financial Foundation](the-first-month-set-up-your-financial-foundation)

3. [Build a Budget That Actually Works in 2026](build-a-budget-that-actually-works-in-2026)

4. [Emergency Fund: Your 1 Wealth-Building Tool](emergency-fund-your-1-wealth-building-tool)

5. [Credit Scores and Credit Cards: Use Them, Don’t Let Them Use You](credit-scores-and-credit-cards-use-them-dont-let-them-use-you)

6. [Pay Off Debt Strategically (Student Loans, BNPL, and More)](pay-off-debt-strategically-student-loans-bnpl-and-more)

7. [Start Investing Early even if It’s Small](start-investing-earlyeven-if-its-small)

8. [Retirement Accounts and Workplace Benefits to Max Out](retirement-accounts-and-workplace-benefits-to-max-out)

9. [Insurance Basics for First-Time Employees](insurance-basics-for-first-time-employees)

10. [Avoid Lifestyle Inflation (Without Feeling Deprived)](avoid-lifestyle-inflation-without-feeling-deprived)

11. [Money Habits to Automate in 2026](money-habits-to-automate-in-2026)

12. [Common Financial Mistakes Young Professionals Make](common-financial-mistakes-young-professionals-make)

13. [A Simple 2026 Financial Checklist](a-simple-2026-financial-checklist)

14. [FAQs](faqs)

15. [Final Thoughts](final-thoughts)

—

Why 2026 Is a Unique Time to Start Managing Money

Personal finance for young adults in 2026 looks different than it did a decade ago. You’re likely dealing with:

– Higher rent and cost-of-living pressure in many cities

– Subscription creep (apps, streaming, AI tools, delivery memberships)

– Buy Now Pay Later (BNPL) offers everywhere

– Easier access to investing (and more temptation to “trade”)

– A job market where switching roles is common and benefits vary widely

The good news: you can build a strong financial life faster than ever if you focus on the right fundamentals.

—

The First Month: Set Up Your Financial Foundation

Before you worry about investing strategies or side hustles, lock in the basics.

1) Know your real take-home pay

Your offer letter salary is not what hits your bank account. In 2026, your paycheck may include:

– Taxes (federal, state, local)

– Health insurance premiums

– Retirement contributions

– Benefits like commuter plans or HSA/FSA

Action step: Use your first paycheck to calculate your “net monthly income” (what you actually can spend/save).

2) Open the right accounts

At minimum, you’ll want:

– Checking account for bills and daily spending

– High-yield savings account (HYSA) for emergency fund and short-term goals

– Retirement account through work (if offered)

3) Set up autopay for essentials

Autopay reduces late fees and protects your credit score. Prioritize:

– Rent

– Utilities

– Minimum debt payments

– Credit card statement balance

—

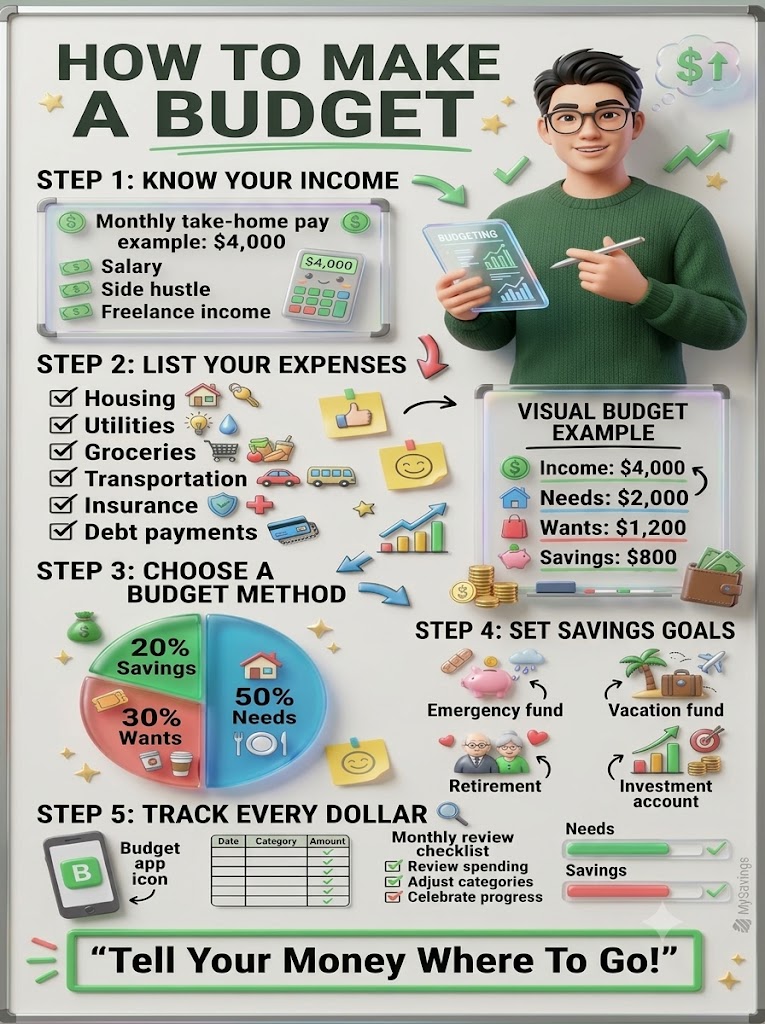

Build a Budget That Actually Works in 2026

Budgeting isn’t about restriction; it’s about directing your money toward what matters.

Try the “50/30/20” rule then personalize it

A common starting point:

– 50% Needs: rent, groceries, utilities, transportation

– 30% Wants: dining out, entertainment, travel

– 20% Savings/Debt: emergency fund, investing, loan payoff

In many cities, rent alone can exceed 30–40%. If that’s you, adjust the percentages and focus on keeping your savings rate consistent, even if small.

Use a “two-account” system

A simple method that works well for first jobs:

– Paycheck lands in Checking A (Bills)

– Automatically transfer a “spending allowance” to Checking B (Fun/Variable spending)

This prevents accidental overspending and makes your budget feel effortless.

—

Emergency Fund: Your 1 Wealth-Building Tool

An emergency fund keeps you from going into debt when life happens (car repairs, job changes, medical costs).

How much should you save in 2026?

Start with:

– $1,000 mini emergency fund (fast win)

Then build toward:

– 3–6 months of essential expenses

Where to keep it: a high-yield savings account so it’s safe and accessible.

—

Credit Scores and Credit Cards: Use Them, Don’t Let Them Use You

Your credit score affects:

– Apartment approvals

– Car loan rates

– Some job background checks (industry dependent)

– Insurance pricing in some regions

Rules for credit success

– Pay on time, every time

– Keep utilization low (ideally under 30%, better under 10%)

– Don’t open too many accounts at once

– Avoid carrying a balance

Best practice: Treat your credit card like a debit card and pay it off in full monthly.

—

Pay Off Debt Strategically (Student Loans, BNPL, and More)

Debt is not always “bad,” but unmanaged debt is expensive.

Student loans (common for new grads)

– Confirm your repayment plan and interest rates

– If you have multiple loans, consider:

– Avalanche method: pay highest interest first (saves most money)

– Snowball method: pay smallest balance first (motivating)

Watch out for BNPL in 2026

BNPL can feel harmless, but multiple small payments can quietly wreck your cash flow.

Rule: If you wouldn’t buy it outright today, don’t finance it.

—

Start Investing Early even if It’s Small

Time is your biggest investing advantage. Starting in your early 20s can make a huge difference due to compound growth.

A simple investing approach for beginners

If you’re not sure where to start, consider:

– Low-cost index funds

– Broad market ETFs

– Target-date retirement funds (simple “set it and forget it” option)

Avoid: day trading or chasing hype. In 2026, investing apps make trading easy but not necessarily profitable.

—

Retirement Accounts and Workplace Benefits to Max Out

Your first job often includes benefits that are basically “free money” if you use them.

1) 401(k) / workplace retirement plan

If your employer offers a match, aim to contribute at least enough to get the full match.

Example: If they match up to 4%, contribute 4% that’s an instant return.

2) HSA (Health Savings Account), if eligible

An HSA can be one of the most tax-efficient accounts:

– Contributions may be pre-tax

– Growth can be tax-free

– Qualified medical withdrawals can be tax-free

3) ESPP and stock benefits (if offered)

Employee Stock Purchase Plans can be valuable, but don’t overconcentrate your wealth in your employer’s stock.

—

Insurance Basics for First-Time Employees

Insurance isn’t fun, but it protects your progress.

Key coverage to consider

– Health insurance: understand deductible, copays, out-of-pocket max

– Renter’s insurance: often inexpensive and worth it

– Auto insurance: shop rates annually

– Disability insurance: important if you rely on your income (most people do)

—

Avoid Lifestyle Inflation (Without Feeling Deprived)

Lifestyle inflation happens when your spending rises as fast as your income so you never feel ahead.

A better approach: “Raise your savings rate first”

When you get a raise:

1. Increase retirement contribution

2. Increase emergency fund or investing

3. Then upgrade lifestyle (if you want)

This keeps you moving forward while still enjoying your money.

—

Money Habits to Automate in 2026

Automation is the cheat code for consistent financial progress.

Automate:

– Payday transfer to HYSA (emergency + goals)

– 401(k) contributions

– Roth IRA contributions (if applicable)

– Bill payments

– Credit card full balance payment

If you never see the money, you’re less likely to spend it.

—

Common Financial Mistakes Young Professionals Make

Avoid these early-career traps:

– Not tracking subscriptions and recurring charges

– Carrying credit card balances “just this month”

– Ignoring employer match (leaving money on the table)

– Buying a car that stretches your budget

– Investing without an emergency fund

– Trying to get rich quick with risky trades

—

A Simple 2026 Financial Checklist

Use this as your first-year roadmap:

Month 1–2

– Calculate take-home pay

– Build a starter budget

– Set up checking + HYSA

– Start $1,000 emergency fund

– Enroll in benefits

Month 3–6

– Contribute enough to get full 401(k) match

– Pay down high-interest debt

– Build emergency fund to one month of expenses

– Track subscriptions and cut waste

Month 6–12

– Grow emergency fund to 3 months (or more)

– Start/expand investing (index funds/ETFs)

– Increase savings rate after any raise

– Set goals: travel, car, moving, education, business

—

FAQs

What’s the best personal finance advice for young adults in 2026?

Start with an emergency fund, avoid high-interest debt, get your employer retirement match, and automate saving/investing.

How much should a new graduate save from their first job?

Aim for 10–20% of take-home pay if possible. If that’s too high, start with 1–5% and increase every few months.

Should I invest or pay off debt first?

If the debt is high-interest (like credit cards), pay that off first. If it’s low-interest, you may be able to invest while paying it down consistently especially if you’re also building an emergency fund.

Is budgeting still necessary with good income?

Yes higher income without a plan often leads to higher spending. Budgeting ensures your money supports your goals.

—

Final Thoughts

If you’re starting your career in 2026, you don’t need a perfect plan you need a simple one you can stick to. Focus on the fundamentals: spend intentionally, save automatically, protect yourself with an emergency fund, and invest consistently. Those habits will outperform almost any “hack” over time.

If you want, tell me your country, expected monthly take-home pay, and whether you’ll have student loans and I’ll create a personalized first-year money plan and budget template for 2026.