In the world of personal finance, there is a common misconception that a high salary is synonymous with wealth. We often see the six-figure paycheck as the finish line, yet many high earners find themselves living “paycheck to paycheck” in gold-plated cages.

The real differentiator between the middle class and the truly wealthy isn’t the size of the gross income; it is the mastery of cash flow. While most people focus on the “how much,” millionaires focus on the “where to.”

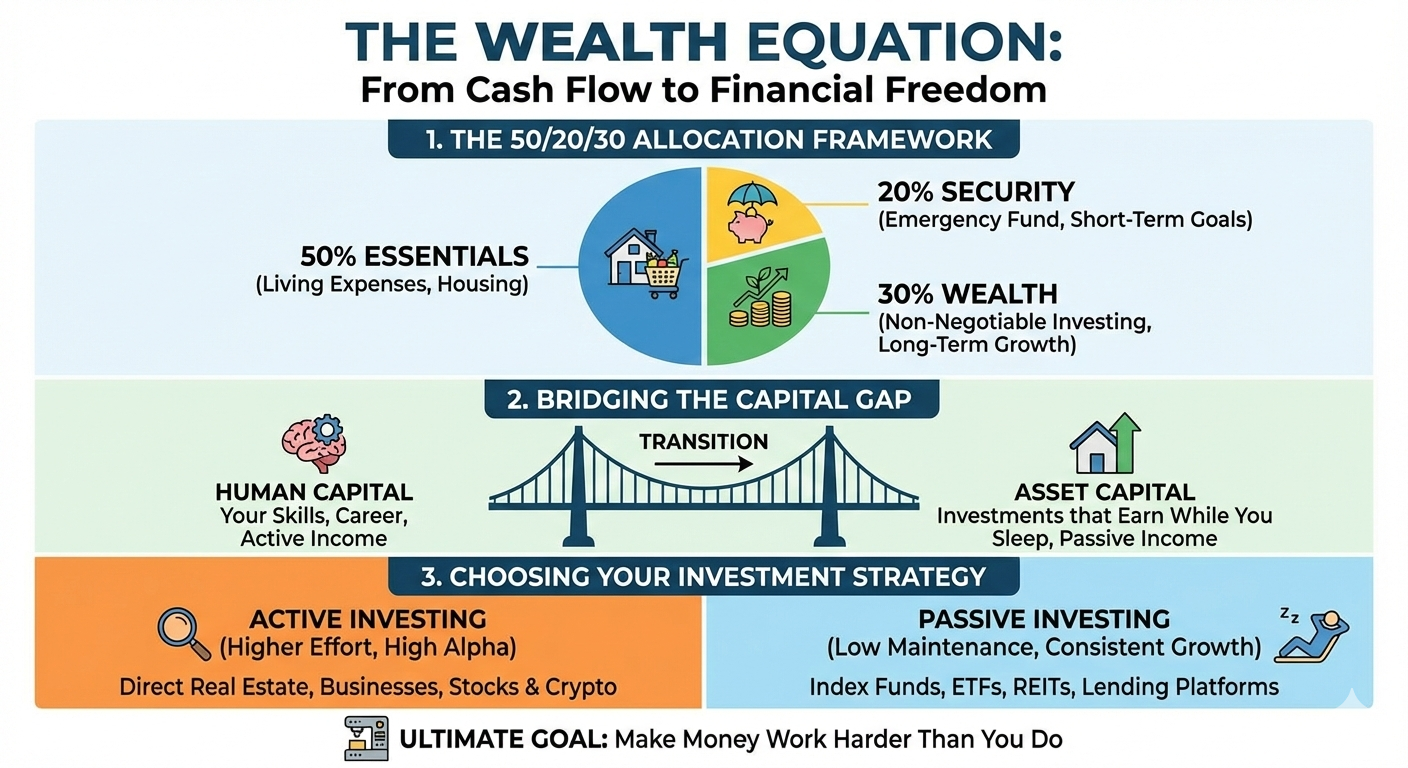

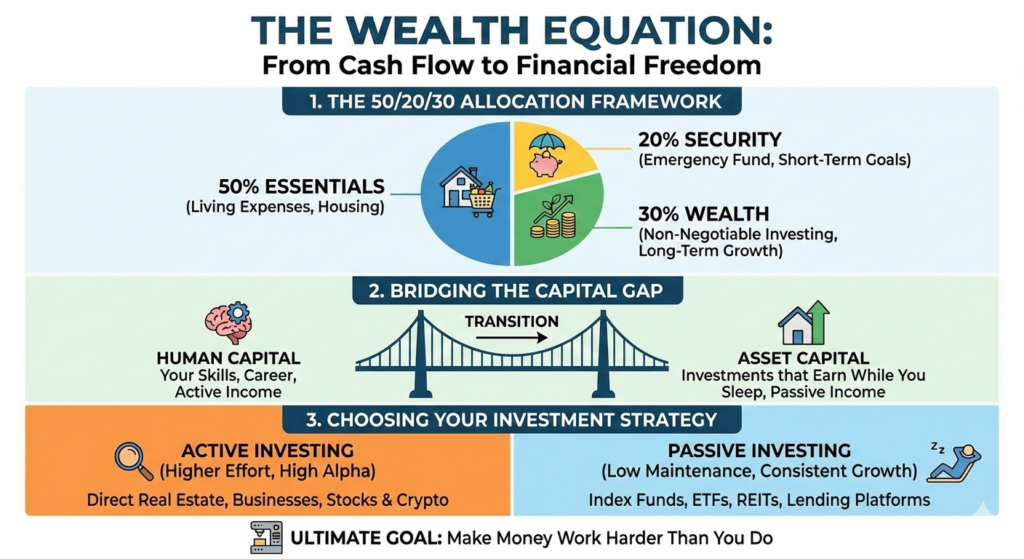

1. The 50/20/30 Framework: Disciplined Allocation

The first step in thinking like a millionaire is moving away from accidental spending and toward intentional allocation. Wealthy individuals typically view their capital through three distinct lenses:

- 50% for Essentials (The Foundation): This covers living expenses, housing, and utilities. By keeping overhead at half of their take-home pay, they ensure they are never “house poor” or over-leveraged.

- 20% for Security (The Safety Net): This is dedicated to emergency funds and short-term goals. It provides the “peace of mind” capital required to take calculated risks later.

- 30% for Wealth (The Engine): Here is the kicker: Investing is treated as a non-negotiable expense. For the wealthy, this 30% is a bill they pay to their future selves every single month, without fail.

2. Bridging the Gap: Human Capital vs. Asset Capital

To build lasting wealth, you must understand the transition from active labor to passive growth. This requires balancing two types of capital:

- Human Capital: This is your “active” power—your skills, your career, and your professional reputation. It is your primary engine for generating seed money.

- Asset Capital: This is your “passive” power—investments that generate returns while you sleep.

The goal of a wealth-builder is to use their Human Capital to purchase Asset Capital until the latter can eventually replace the former.

3. Choosing Your Strategy: Active vs. Passive

Once you have committed to the 30% investment rule, the next step is choosing a vehicle that matches your lifestyle and risk appetite. Wealthy portfolios are generally split into two categories:

Active Investing (Higher Effort, High Alpha)

This requires time, expertise, and “sweat equity.” It is for those who want to beat market averages through direct involvement.

- Direct Real Estate: Managing properties for rental income and appreciation.

- Business Ventures: Building or buying private companies.

- Individual Equities & Crypto: Strategic positioning in high-growth markets.

Passive Investing (Lower Maintenance, Consistent Growth)

This is the “set it and forget it” approach designed for long-term compounding.

- Index Funds & ETFs: Diversified exposure to the entire market.

- REITs (Real Estate Investment Trusts): Earning real estate dividends without being a landlord.

- Lending Platforms: Earning interest by acting as the bank.

The Bottom Line

The ultimate objective of financial management isn’t just to accumulate a large number in a bank account. It is to reach a point of leverage where your money works harder than you do.

By shifting your focus from “how much can I earn?” to “how can I allocate my cash flow?”, you stop chasing the next paycheck and start building a legacy.