Achieving millionaire status is rarely the result of luck; it is the outcome of a disciplined financial framework centered on capital conversion and strategic cash flow management. This comprehensive guide breaks down the “Millionaire Blueprint,” exploring the fundamental transition from human capital to asset capital. By implementing the 50/20/30 rule allocating 50% to essential living expenses, 20% to savings, and 30% to monthly investments individuals can create a sustainable path toward wealth. The article further distinguishes between active and passive investing strategies, providing an objective analysis of vehicles such as stocks, real estate, index funds, and ETFs. Whether you are looking to optimize your current paycheck or build a diversified portfolio from scratch, understanding these core pillars of money handling is essential for long-term fiscal stability and exponential growth. This exploration serves as a roadmap for anyone seeking to master the mechanics of wealth building through proven, structured methodologies.

The path to significant wealth is often shrouded in mystery, yet the underlying mechanics are remarkably consistent among high-net-worth individuals. Wealth creation is not merely about how much one earns, but rather how one allocates those earnings across different types of capital and investment vehicles. To build a lasting financial legacy, one must understand the flow of money from its inception as labor to its final form as a self-sustaining asset.

Understanding the Two Pillars of Capital

At the core of the millionaire mindset is the distinction between Human Capital and Assets Capital. These represent the two primary phases of a wealth-building journey.

1. Human Capital: The Starting Point

Human capital refers to the intangible assets an individual possesses: education, skills, experience, and the ability to perform labor. For most people, human capital is their first and most significant asset. It is the engine that generates initial cash flow. To maximize human capital, individuals must focus on “upskilling” and increasing their market value. However, human capital is finite; it is limited by time, health, and age.

2. Assets Capital: The Wealth Accelerator

The ultimate goal of financial planning is to convert human capital into assets capital. Assets capital consists of tangible and intangible investments that generate value or income without requiring active labor. This includes equities, properties, and business interests. Transitioning from “working for money” to “money working for you” is the definitive shift that separates earners from wealth builders.

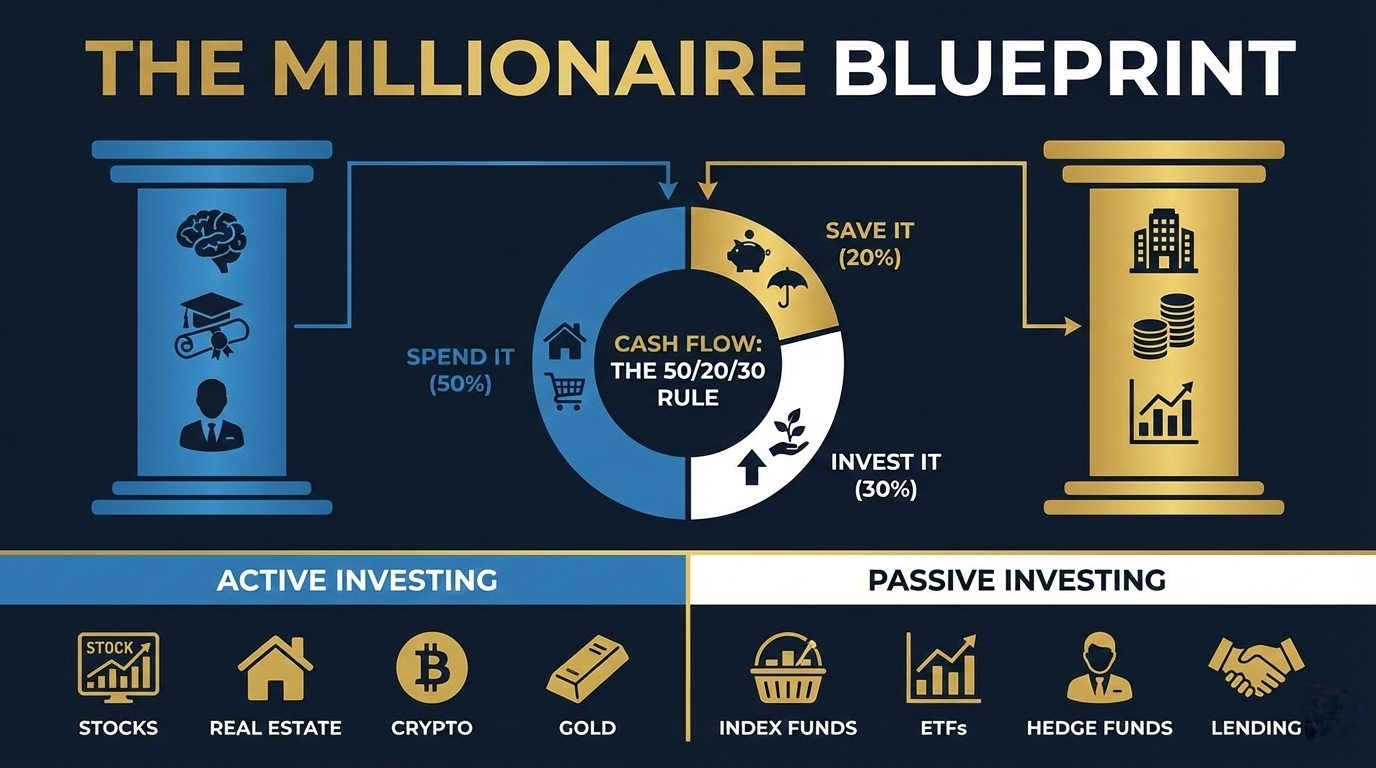

The 50/20/30 Framework for Cash Flow Management

Once income is generated via human capital, the methodology of its distribution determines the speed of wealth accumulation. A highly effective and professional standard used for managing cash flow is the 50/20/30 Rule.

- Spend It (50%): Daily Living Expenses To maintain financial health, essential costs—such as housing, utilities, groceries, and transportation—should ideally not exceed 50% of take-home pay. Keeping fixed costs low provides the “breathing room” necessary to fund the other two categories.

- Save It (20%): The Safety Net One-fifth of every paycheck should be directed toward liquid savings. This serves as an emergency fund and a buffer against market volatility. In the millionaire framework, this 20% provides the psychological and financial security to take calculated risks elsewhere.

- Invest It (30%): The Growth Engine The most critical component for long-term wealth is the 30% allocated to investments every single month. This is not a “leftover” amount; it is a priority. Consistent, monthly contributions to investment vehicles allow for the power of compounding to take effect over time.

Active vs. Passive Investing: Choosing Your Path

When it comes to the 30% investment allocation, investors generally choose between two primary paths: Active Investing and Passive Investing.

Active Investing: Seeking Higher Returns Through Involvement

Active investing requires significant time, research, and ongoing management. It is often higher risk but offers the potential for market-beating returns.

- Stocks: Directly purchasing shares of individual companies based on fundamental analysis.

- Real Estate: Investing in physical property to generate rental income or capital appreciation. This requires property management and market timing.

- Businesses: Owning or operating a private enterprise. This is perhaps the most direct way to leverage human capital into assets capital.

- Crypto: High-volatility digital assets that require a deep understanding of blockchain technology and market sentiment.

- Gold: A traditional hedge against inflation and currency devaluation, often used to preserve wealth during economic downturns.

Passive Investing: Efficiency and Diversification

Passive investing is designed for those who prefer a “set it and forget it” approach, focusing on long-term market growth rather than short-term fluctuations.

- Index Funds & ETFs: These provide instant diversification by tracking a specific market index (like the S&P 500). They are cost-effective and historically reliable.

- Hedge Funds: Managed investment funds that employ different strategies to earn active returns for their investors, typically available to accredited investors.

- Lending: Peer-to-peer lending or private debt where you earn interest on capital provided to others.

- EBITS (Earnings-Based Investments): Focusing on assets that provide consistent earnings before interest and taxes, often through structured business debt or preferred equity.

Conclusion: The Compound Effect

The journey to becoming a millionaire is a marathon, not a sprint. By prioritizing the conversion of human capital into asset capital and adhering to a strict 50/20/30 cash flow split, anyone can build a robust financial foundation. The choice between active and passive investing depends on one’s risk tolerance and available time, but the most important factor is consistency. Monthly investments, coupled with a disciplined lifestyle, create a snowball effect that eventually leads to total financial independence.