Achieving financial independence requires a strategic shift from traditional saving habits to proactive wealth-building systems. This comprehensive guide outlines five foundational financial rules that individuals should master by age 30 to secure their economic future. By prioritizing income growth over extreme frugality and focusing on high-impact investments, one can build a robust financial foundation. The article explores the importance of “going all-in” on specialized asset classes, the necessity of continuous skill acquisition, and the strategic protection of credit scores. Furthermore, it emphasizes the power of consistent, incremental investing and the philosophy of expanding one’s earning power. Designed for those seeking to build real wealth in their 30s, 40s, and beyond, these principles serve as a blueprint for navigating modern economic landscapes with precision and objective financial logic. Learn how to transition from a mindset of scarcity to one of scalable asset management and sustainable fiscal growth.

The journey to financial freedom is often paved with outdated advice that focuses solely on penny-pinching and risk aversion. However, modern wealth creation demands a more sophisticated approach. To build real wealth in your 30s, 40s, and beyond, it is essential to implement specific financial frameworks that prioritize growth, leverage, and consistency.

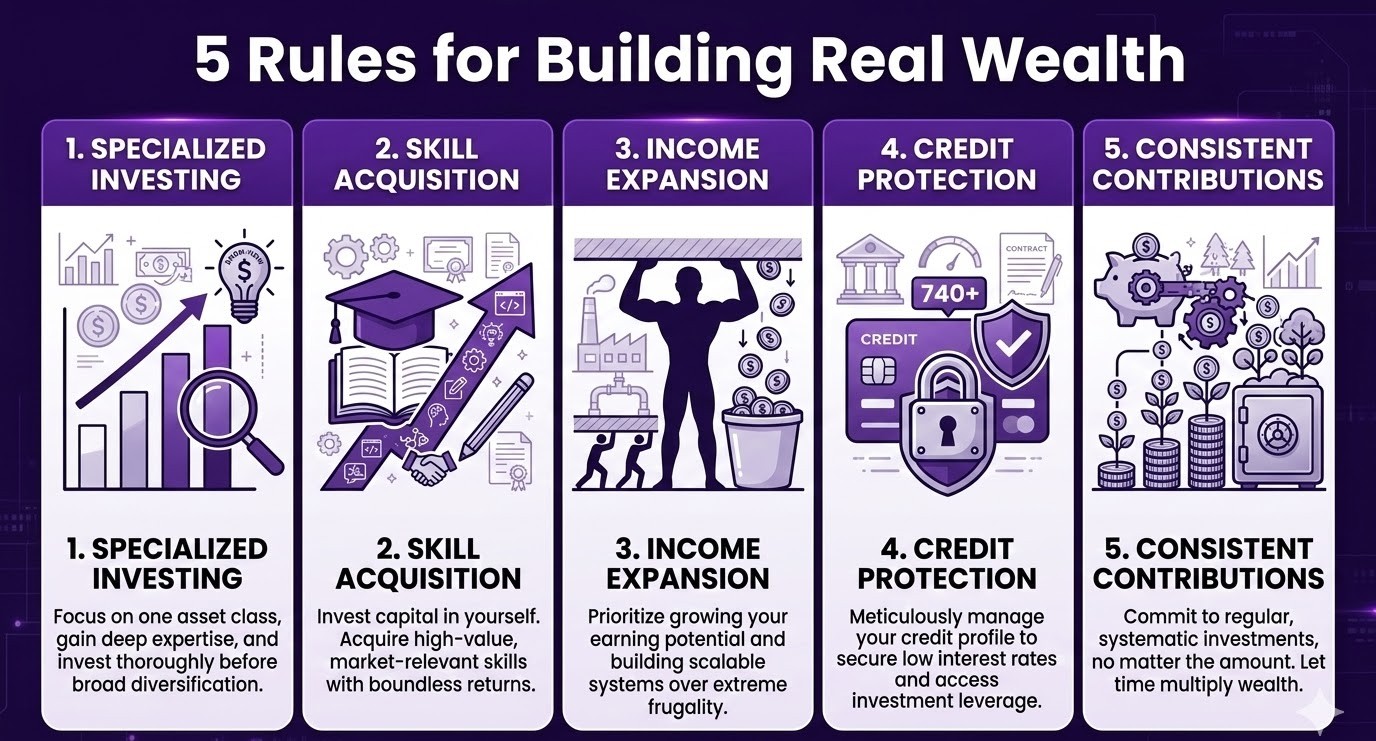

1. The Power of Specialized Investment: Go All-In on One Asset Class

Traditional financial advice often emphasizes immediate diversification. While diversification is a vital tool for wealth preservation, it can often dilute the potential for wealth creation in the early stages. The first rule for building significant capital is to research and invest deeply in a single asset class that you understand thoroughly.

By focusing on one area—whether it be equities, real estate, or a specific industry—you develop an informational advantage. This “all-in” approach allows you to master the nuances of market cycles, valuation metrics, and risk factors within that niche. Once a substantial return has been realized and a solid capital base is established, the strategy should then shift toward diversifying the portfolio to mitigate systemic risk.

2. Strategic Capital Allocation: Spending to Improve Skills

Wealth is not merely a reflection of what you keep, but what you are capable of generating. One of the most effective uses of capital is reinvesting it into your own human capital. Spending money to improve your skills is an investment with a potentially infinite ROI.

In a fluctuating economy, specialized knowledge acts as a hedge against business dips and market volatility. Whether it involves obtaining advanced certifications, mastering new technologies, or developing leadership competencies, the objective is to increase your value in the marketplace. This shift in perspective moves money from being a “spent” resource to a “leveraged” tool for professional advancement.

3. Shifting the Focus: Increase Income Over Reducing Expenses

A common financial pitfall is the attempt to “shrink” one’s way to wealth. While fiscal responsibility is necessary, there is a hard floor on how much a person can cut from their expenses. Conversely, there is no theoretical ceiling on how much one can increase their income.

The wealthy focus on expanding their earning power rather than merely minimizing their lifestyle. This involves building scalable systems, developing side businesses, or negotiating higher-value contracts. By focusing on income expansion, you create the surplus necessary to fund aggressive investment strategies. Building systems that generate income independently of your time is the ultimate goal of this rule.

4. Credit as Leverage: Build and Protect Your Score

In the modern financial system, credit is more than just a number; it is a tool for leverage. Aiming for a credit score of 740 or higher is essential for accessing the best financial products. High credit scores lead to lower interest rates and reduced borrowing costs, which are critical when seeking funding for business ventures or real estate acquisitions.

Protecting your credit involves meticulous management of debt-to-income ratios and timely repayments. When you maintain excellent credit, you position yourself to use “other people’s money” (OPM) to acquire appreciating assets. This leverage is a cornerstone of professional wealth building, allowing for faster scaling than would be possible through cash savings alone.

5. The Consistency Principle: Invest Regardless of the Amount

The final rule is the commitment to consistent investing, regardless of the size of the contribution. The mathematical power of compound interest is most effective over long durations. Starting early—even with small amounts—allows time to do the heavy lifting.

Whether the vehicle is an index fund, real estate, or business ownership, the key is the habit of monthly or quarterly contributions. This approach, often referred to as dollar-cost averaging in the context of stocks, removes the emotional volatility of trying to “time the market.” Small, consistent contributions create a foundation of long-term financial strength that eventually evolves into a self-sustaining portfolio.

Implementing the Wealth Framework

Mastering these five rules by age 30 sets a trajectory for lifelong financial success. By focusing on specialized expertise, continuous self-improvement, income expansion, credit leverage, and disciplined consistency, individuals can move beyond basic survival into the realm of true wealth accumulation. These principles are not shortcuts; they are the structural components of a professional financial strategy designed for the long term.