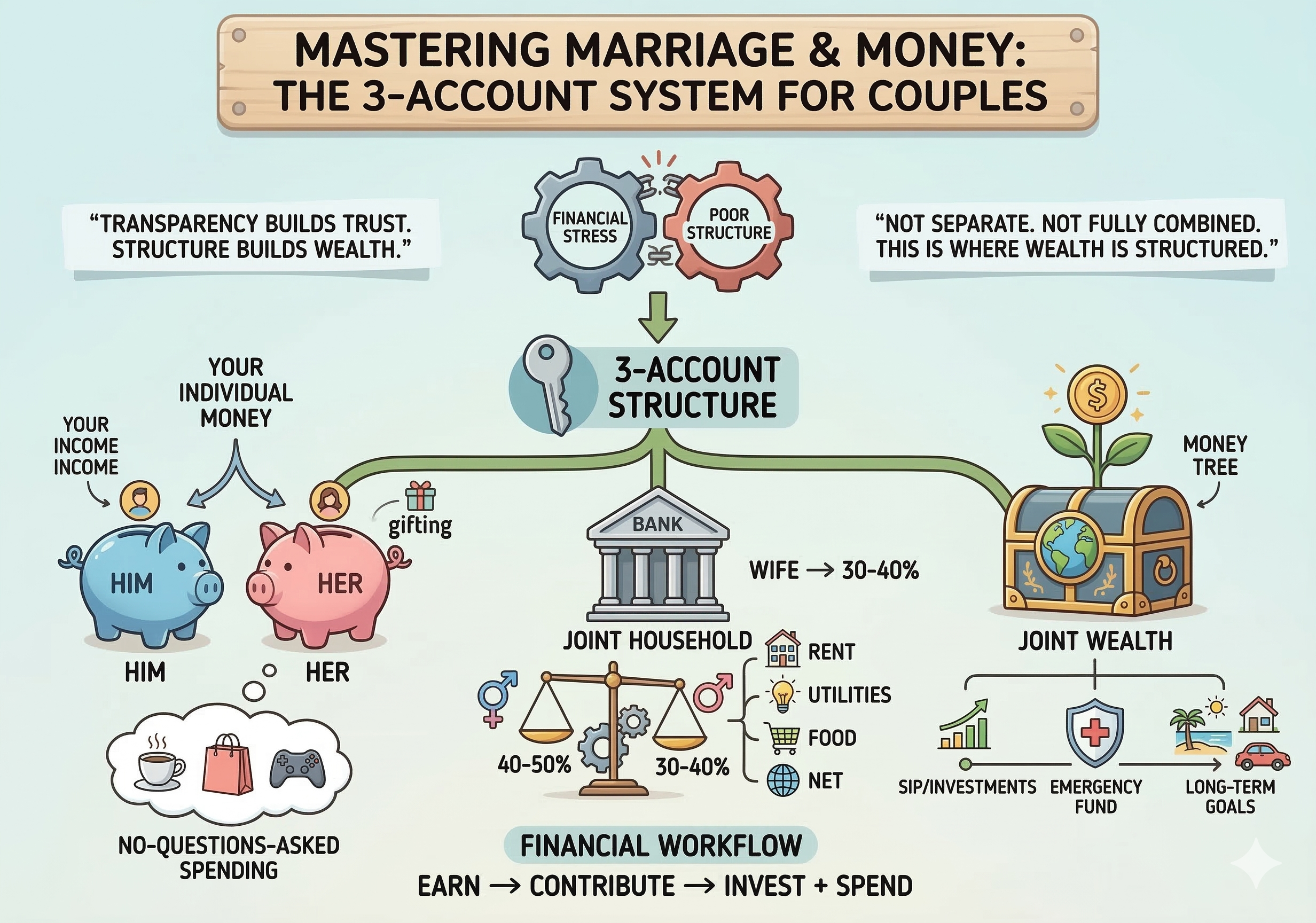

Money is often cited as the leading cause of friction in relationships. However, as the old saying goes, “It’s not about how much you make, but how you manage it.” Most couples fight about money not because they are broke, but because they lack a clear, transparent structure for who pays for what and who owns what.

When two lives merge, the “yours, mine, and ours” of finance can become a messy tug-of-war. To solve this, savvy couples are increasingly turning to the 3-Account System. This framework provides a roadmap for maintaining individual autonomy while aggressively pursuing shared financial dreams. Here is how to break it down.

1. The Personal Account: Protecting Your “No Questions Asked” Zone

The first pillar of a healthy financial marriage is, ironically, a bit of independence. Each partner should maintain their own Personal Account.

This is your “individual money.” In a healthy relationship, you shouldn’t have to justify every cup of coffee, video game purchase, or hobby expense to your partner. This account covers:

- Personal Expenses: Clothing, individual subscriptions, or nights out with friends.

- Gifting: It’s hard to surprise your spouse with a birthday gift if they can see the transaction on a joint statement immediately.

- Small Indulgences: Whether it’s a luxury skincare product or a niche collectible, this money is yours to spend.

The philosophy here is “No questions asked spending.” By having a set amount of “mad money” each month, you eliminate the resentment that comes from feeling like you’re being “monitored” or “controlled” by your partner.

2. The Joint Expense Account: The Engine Room of the Household

The second account is the Joint Expense Account. Think of this as the household’s “running account.” This is where the logistics of your life together happen. Rent or mortgage payments, utility bills, groceries, and internet costs all live here.

The graphic suggests a specific contribution ratio, though this should be adapted to your specific situation:

- Proportional Contribution: Often, one partner earns more than the other. A common rule is to contribute based on your income ratio. For example, the higher earner might contribute 40–50% of their take-home pay, while the other contributes 30–40%.

- The Goal: The goal isn’t necessarily a 50/50 split of the dollar amount, but a 50/50 split of the effort. Both partners should feel they are contributing a fair share relative to what they bring in.

Using this account ensures that the lights stay on and the fridge stays full without either person feeling like they are carrying the entire burden of the “boring bills.”

3. The Joint Wealth Account: Building Your Empire

While the Expense Account looks at today, the Joint Wealth Account looks at tomorrow. This is your “Future Building Account,” and it is where true wealth is created.

This account isn’t for spending; it’s for growing. It should be used for:

- SIPs and Investments: Systematically investing in stocks, mutual funds, or real estate.

- Emergency Fund: A safety net of 3–6 months of expenses to protect the family from job loss or medical emergencies.

- Insurance: Paying for life, health, and disability insurance to protect your shared assets.

- Long-term Goals: Saving for a house down payment, a child’s education, or that dream retirement.

As the image notes, “Transparency builds trust. Structure builds wealth.” This account represents your shared vision. It turns money from a source of stress into a tool for freedom.

The Golden Rule: Earn → Contribute → Invest + Spend

The workflow for this system is simple but effective:

- Earn: Both partners bring in their respective incomes.

- Contribute: A predetermined percentage of those incomes goes into the Joint Expense and Joint Wealth accounts.

- Invest + Spend: The “Wealth” portion is invested immediately, and whatever remains in the Personal Accounts is yours to spend guilt-free.

Why This Works

This system strikes a perfect balance. It is not separate money (where you live like roommates), and it is not fully combined money (where you lose your individual identity). Instead, it is structured money.

By implementing this 3-account system, you move away from reactive “money fights” and toward a proactive “wealth strategy.” You’ll find that when the structure is clear, the conversations about money become less about “why did you buy that?” and more about “how quickly can we reach our goals?”