Save Smarter from Early

Save a starter emergency fund, Get out of debt, Pay cash for your car, Pay cash for college, and Build wealth and give, forming a sequential path from stability to abundance by first tackling crises, then debt, big purchases, education, and finally growing significant wealth

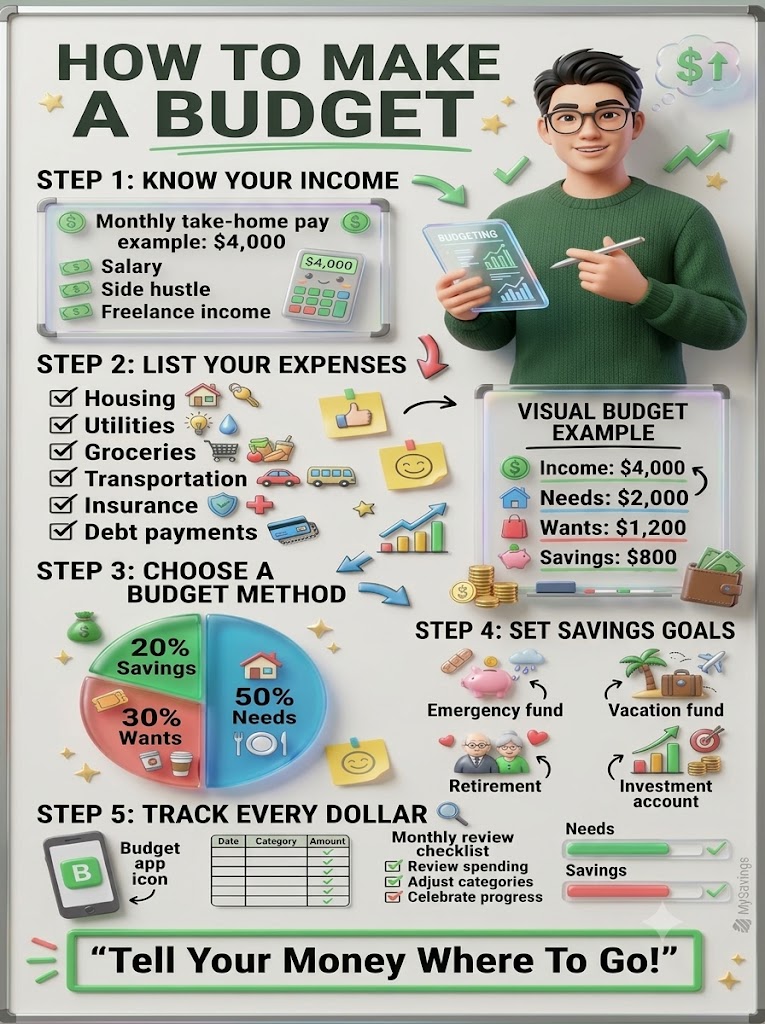

Create a Budget and Track Your Spending: A budget is a plan for your money, ensuring you know exactly where it goes each month. Track your expenses to understand your spending habits and identify areas where you can cut back. A zero-based budget (income minus expenses equals zero, with every dollar assigned a job like saving or spending) is a popular method.

Live on Less Than You Make: The fundamental rule of personal finance is to spend less than your income. This creates a margin in your budget that allows for saving, investing, and paying off debt, rather than living paycheck to paycheck.

Build an Emergency Fund: Life is unpredictable, and unexpected expenses (car repairs, medical bills, job loss) can arise. Aim to save three to six months’ worth of living expenses in a separate, easily accessible savings account to act as a financial safety net.

Pay Off High-Interest Debt: Manage your debt wisely by prioritizing the repayment of high-interest debt, such as credit cards. High interest rates make it difficult to get ahead financially, so paying these off first saves you money in the long run.

Set Clear Financial Goals: Define what you want to achieve with your money, whether it’s saving for a down payment on a house, paying off student loans, or building a retirement fund. Setting specific, achievable goals helps you stay motivated and focused on your financial journey.

Start Saving and Investing Early: Take advantage of the power of compound interest by starting to save and invest as soon as possible. Even small, consistent contributions over time can grow significantly. Consider utilizing tax-advantaged accounts like a 401(k) or IRA.

Use Credit Wisely: Credit can be a powerful tool, but it’s important to understand the terms before you borrow. Avoid accumulating unnecessary debt and make more than the minimum payments on any credit cards you have.

Invest in Yourself: Your education and skills are some of your best investments. Studies show that more education often leads to higher lifetime earnings, so investing time and resources into personal and professional development can pay significant dividends.

Automate Your Finances: Make saving a habit by setting up automatic transfers from your checking account to your savings and investment accounts. “Pay yourself first” before you have a chance to spend the money; what you don’t see, you don’t miss.

Review and Adjust Your Plan Regularly: Your financial situation and goals will change over time, so it’s vital to review and update your financial plans periodically. Check your progress, assess your investments, and make adjustments as needed, especially after major life events like a new job, marriage, or childbirth

General Foundational Pillars

Protection/Risk Management: Using insurance and legal tools to safeguard assets.

Income/Earning: Maximizing your money coming in.

Spending/Budgeting: Knowing where your money goes and controlling it.

Saving: Setting aside money for short-term needs (emergency fund, goals).

Investing: Growing your money over the long term (retirement, wealth).