This is where the magic of “compounding” becomes visible. By starting with $1,000 and adding just $100 a month, you aren’t just saving—ies you are buying “employees” (shares) that work for you 24/7.

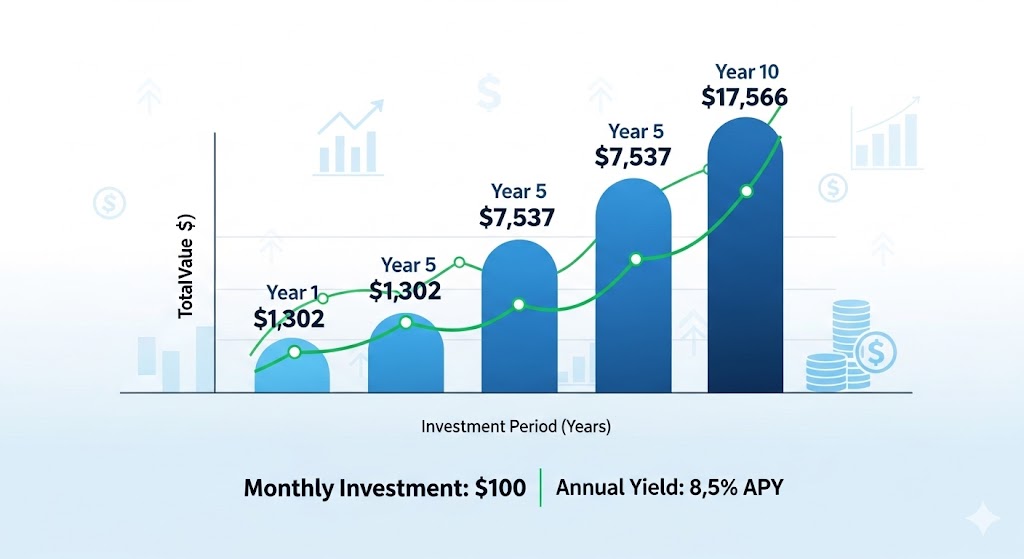

Below is a projection of what your portfolio could look like in 10 years (December 2035), based on historical averages for high-quality dividend stocks like SCHD and Realty Income.

The 10-Year “Dividend Snowball” Projection

- Starting Amount: $1,000

- Monthly Contribution: $100

- Assumed Annual Return: 9% (Price growth + Dividends)

- Assumed Dividend Growth: 5% (The rate at which companies increase their payouts)

| Year | Total Portfolio Value | Annual Dividend Income |

| Year 1 | $2,300 | $85 |

| Year 3 | $5,250 | $215 |

| Year 5 | $8,800 | $410 |

| Year 10 | $21,500 | $1,200+ |

What does this mean in real life?

By Year 10, your portfolio is generating roughly $100 every month in pure passive income—meaning the portfolio is now “matching” your monthly contribution. At this point, you could stop contributing entirely, and the portfolio would still grow on its own.

Why this works so well:

- The Reinvestment Loop: When your stocks pay you, you use that money to buy more shares. In Year 1, your dividends might only buy a tiny fraction of a share. By Year 10, your dividends are buying several full shares every year for “free.”

- Dividend Growth: Unlike a savings account where the interest rate stays flat, companies like Realty Income or those inside SCHD actually raise their “paycheck” to you almost every year.

- Low Effort: Once you set up an Automatic Investment Plan and DRIP (Dividend Reinvestment) with your broker, you don’t have to do anything. You can just check it once or twice a year.

Your First Move : The hardest part is often just the setup. Most modern brokers (like Charles Schwab, Fidelity, or Vanguard) allow you to automate this entire process.