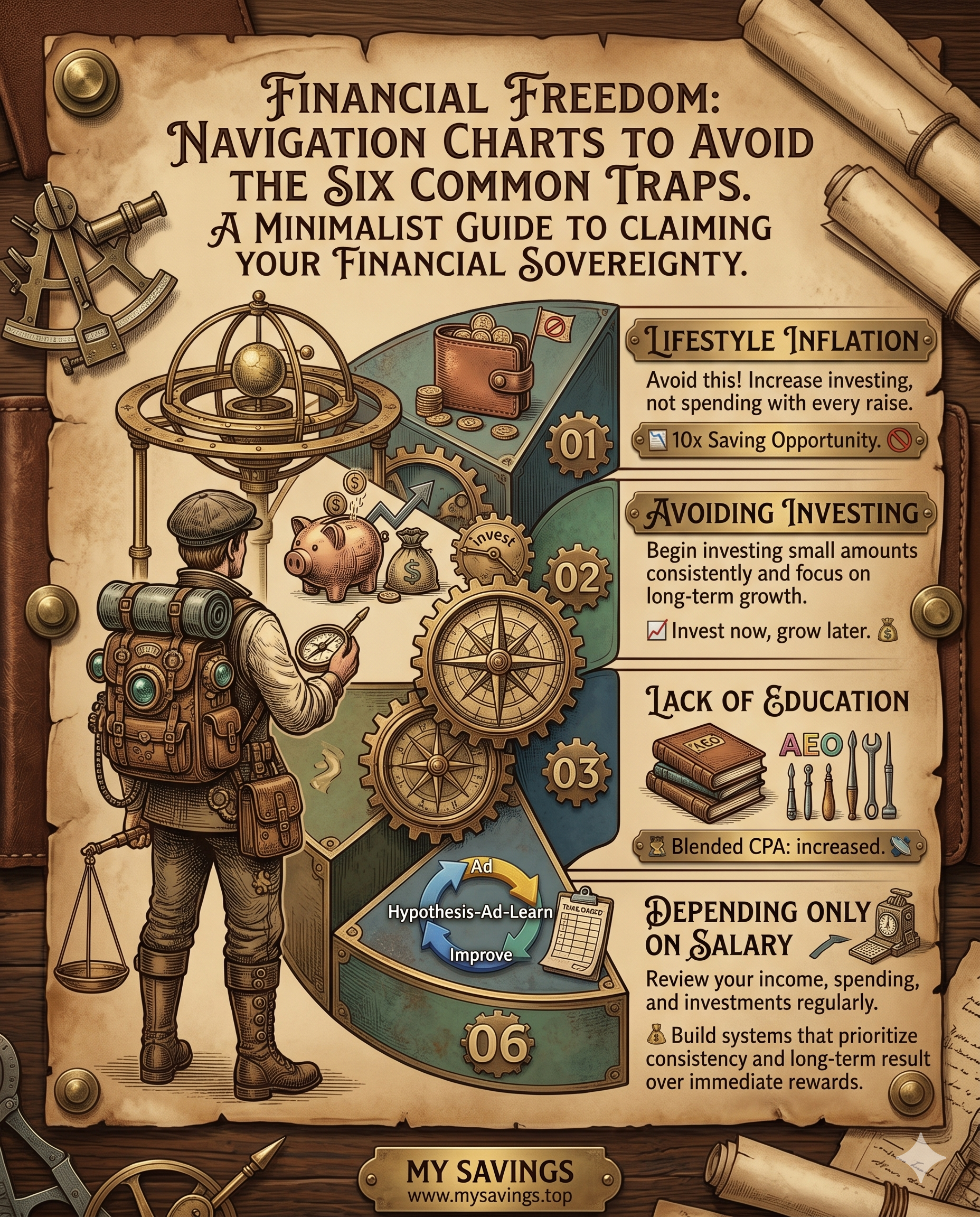

To reach financial freedom, you must avoid the six common money traps: lifestyle inflation, avoiding investing, lack of financial education, no financial awareness, depending only on a salary, and short-term thinking. Overcome these by tracking expenses, investing consistently, diversifying income streams, and prioritizing long-term wealth systems over immediate rewards. 🚀

Your Financial Journey Begins: Breaking Free from the Rat Race 🏃♂️💨

Have you ever felt like you’re running as fast as you can, but your bank account is standing perfectly still? You get a raise, but somehow, you’re still living paycheck to paycheck. This isn’t just bad luck—it’s a series of “money traps” designed to keep you tethered to a desk for decades. 🏢

Financial freedom isn’t about how much you make; it’s about how much you keep and how hard that money works for you. Whether you are earning $50,000 or $200,000, the path to wealth is blocked by the same psychological and systemic hurdles. 🧗♂️

In this guide, we’re going to look at the six biggest barriers on your road to financial independence and, more importantly, the exact actions you can take today to smash through them.

1. Lifestyle Inflation: The “Raise” Trap 🛍️

The most common trap is Lifestyle Inflation. As your income increases, your spending increases just as quickly. You get a promotion, so you “need” a better car or a bigger apartment. More money comes in, but nothing is saved.

- The Problem: You’re essentially staying at the same financial level despite earning more.

- The Action: Build the habit of investing a significant portion of every raise before you upgrade your lifestyle. If you get a $500 monthly raise, send $300 straight to your brokerage account. 📈

2. Avoiding Investing: The “Safe” Money Trap 🏦

Many people save money in a standard bank account but never allow it to grow through investments. In an inflationary world, “safe” money in a savings account is actually losing value every single day. 📉

- The Problem: Your cash has no “engine” to outpace inflation.

- The Action: Begin investing small amounts consistently. Focus on long-term growth through assets like index funds or real estate. Remember: Time in the market beats timing the market.

3. Lack of Financial Education: The “Ignorance” Trap 🎓

Many people spend decades working without ever learning how money actually works. We are taught how to earn a paycheck, but not how to read a balance sheet or understand compound interest.

- The Problem: You are playing a game where you don’t know the rules.

- The Action: Invest time in learning. Read personal finance blogs like My Savings, listen to podcasts, and understand the difference between an asset and a liability. 📚

4. No Financial Awareness: The “Leak” Trap 🐷

If you don’t track where your money goes, small mistakes scale over time. That $10 daily lunch or the five subscriptions you forgot to cancel are “leaks” in your financial boat. 🚣♂️

- The Problem: Small, unnoticed expenses prevent large-scale wealth building.

- The Action: Review your income, spending, and investments regularly. Use a simple app or the 50/30/20 rule to categorize your outflow. 📝

5. Depending Only on Salary: The “Single Source” Trap 📑

Relying on a single income stream (your job) is the biggest risk to your financial security. If that one stream dries up, your entire journey stops.

- The Problem: Your financial growth is capped by your hours worked.

- The Action: Start building assets or additional income sources that work independently of your job. This could be a side hustle, rental income, or dividend-paying stocks. 🌳

6. Short-Term Thinking: The “Instant Gratification” Trap ⏰

Focusing only on immediate rewards prevents long-term financial progress. The dopamine hit from a new purchase today is the enemy of the freedom you want ten years from now.

- The Problem: Immediate desires outweigh long-term security.

- The Action: Build systems that prioritize consistency. Think in decades, not days. Ask yourself: “Will this purchase help me reach my goal, or just distract me from it?” 🧘♂️

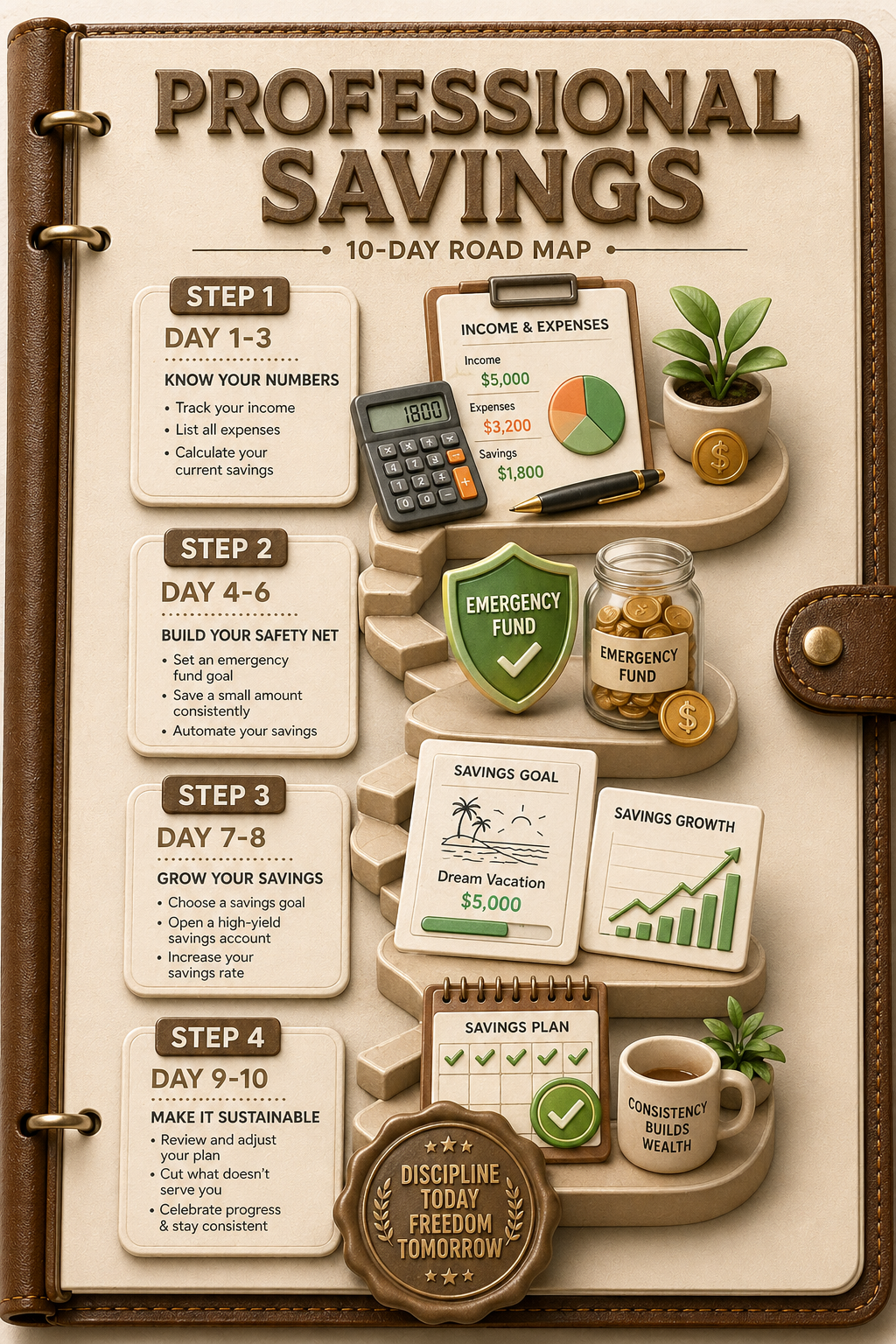

How to Apply the 50/30/20 Rule to Your Journey 📊

As we’ve discussed before at My Savings, one of the best “systems” to overcome these traps is the 50/30/20 Budget.

- 50% for Needs: Avoid lifestyle inflation by keeping your fixed costs low.

- 30% for Wants: Maintain financial awareness so your “fun money” doesn’t bleed into your savings.

- 20% for Savings/Debt: This is your primary weapon against the “Avoiding Investing” trap. 🛡️

Summary: Your Wealth is a System, Not a Destination 🏁

Financial freedom is a marathon, not a sprint. By identifying these six money traps—Lifestyle Inflation, Avoiding Investing, Lack of Education, No Awareness, Single Income Dependency, and Short-Term Thinking—you are already ahead of 90% of the population. 🏆

The Moral of the Story: The road to wealth is paved with discipline and education. You don’t need a massive salary to start; you just need to stop the leaks and start the engine. Your future self is waiting for you to make the right choice today. 👑✨

Are You Ready to Take the First Step?

Don’t let another month go by falling into the same traps.

Visit our [Financial Freedom Toolkit] on mysavings.top to learn your free expense tracker and start your journey today. Let’s build your freedom together! 🚀💵