💡 Personal finance is not just about earning more—it is about mastering habits that protect, grow, and sustain your money over time. This article breaks down 9 essential laws of personal finance that shape financial stability, wealth creation, and long-term security.

💰 From saving first and avoiding lifestyle inflation to understanding the risks of debt and the importance of financial discipline, each principle offers practical guidance for better money management. You will also learn why tracking every dollar matters, how diversification reduces risk, and why ignoring fast-money schemes protects your future.

📊 Whether you are building savings, managing debt, or improving financial awareness, these principles provide a clear roadmap to smarter decisions.

🌍 Designed for readers seeking practical financial education, this guide helps strengthen money habits and supports better financial planning for a more secure future.

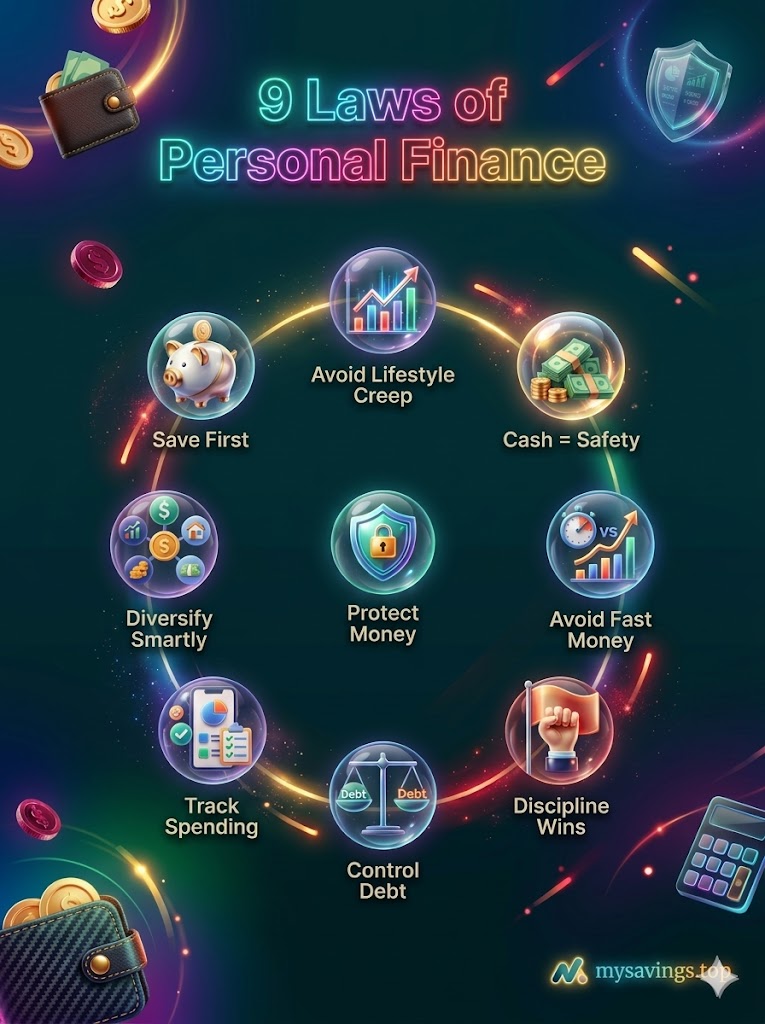

Why Personal Finance Laws Matter

Personal finance is built on behavior, not complexity. While income plays a role in financial stability, long-term success depends on disciplined habits and consistent decision-making. Understanding fundamental financial principles helps individuals avoid common money mistakes, build savings, and create sustainable wealth systems.

These 9 laws of personal finance serve as guiding principles that simplify money management and encourage smarter financial choices in everyday life.

🏦 Law 1: Save First, Spend Later

One of the most effective financial habits is prioritizing savings before expenses. Instead of saving what remains after spending, reversing the order ensures consistent wealth building.

Automating savings helps enforce discipline and creates a stable financial foundation. Over time, this approach builds emergency funds and investment capital without relying on leftover income.

📈 Law 2: Avoid Lifestyle Creep

Lifestyle inflation occurs when expenses increase in proportion to income. While income growth is positive, increasing spending at the same rate prevents wealth accumulation.

Maintaining stable living costs even after income raises allows surplus funds to flow into savings, investments, or debt reduction. Financial growth comes from what is saved, not what is spent.

💵 Law 3: Cash Provides Financial Breathing Room

Cash reserves act as a buffer during unexpected financial challenges. Emergencies such as medical expenses, job changes, or urgent repairs become manageable when savings are available.

Liquidity ensures flexibility and reduces reliance on debt. A strong cash reserve creates financial confidence and stability during uncertain periods.

📊 Law 4: Diversify, Do Not Gamble

Financial security depends on spreading risk across different assets. Relying on a single investment or income source increases vulnerability.

Diversification reduces the impact of market fluctuations and financial losses. A balanced financial portfolio supports long-term growth while minimizing risk exposure.

🔐 Law 5: Protect What You Build

Earning and saving money is only part of financial success—protecting it is equally important. Financial security includes safeguarding accounts, using strong passwords, and avoiding scams.

Cybersecurity awareness and financial vigilance help prevent loss from fraud or identity theft. Protection ensures that accumulated wealth remains secure.

⚠️ Law 6: Ignore Fast-Money Promises

Quick-profit schemes often carry hidden risks. Financial decisions should be based on verified information rather than emotional persuasion or unrealistic promises.

Evaluating financial advice sources is essential before committing money. Sustainable wealth is built slowly, not through shortcuts.

📒 Law 7: Track Every Dollar

Money management requires awareness of income and expenses. Without tracking, financial control becomes impossible.

Budgeting tools or simple expense logs help identify spending patterns and unnecessary costs. Awareness leads to better decisions and improved savings behavior.

💳 Law 8: Debt Slows Financial Progress

Debt reduces future financial flexibility by committing income to past spending decisions. High-interest obligations further limit wealth-building potential.

Managing debt responsibly or reducing it over time improves financial freedom. Avoiding unnecessary borrowing supports long-term financial health.

🧠 Law 9: Discipline Beats Emotion

Financial decisions driven by emotions often lead to mistakes. Impulse spending, panic selling, or fear-based choices can harm long-term goals.

Discipline ensures consistency in saving, investing, and budgeting. Successful financial outcomes depend more on behavior than mathematical knowledge.

🌍 Final Thoughts

These 9 personal finance laws provide a foundation for building financial stability and long-term wealth. When applied consistently, they help improve decision-making, reduce risk, and strengthen financial confidence.

Mastering these principles allows individuals to move toward financial independence through structured habits rather than unpredictable outcomes.

For more financial insights and saving strategies, explore resources from My Savings.